2014.05.20_oecd-eclac-pse forum_mojon

TRANSCRIPT

Euro area 2014 monetary policy challenges

Benoit MojonBanque de France

Europe and Latin America in an ever-changing global economy

OECD Headquarters ,20 Mai 2014

2

European challenges & global interactions

I’ll focus on the Euro Zone :

1. Where we come from: main stress is behind

2. Where we are: slow and fragile recovery with too low inflation

3. Where we are headed: resolute monetary policy =>

neither deflation

nor too low inflation for too long

0

1

2

3

4

5

6

7

2007m1 2009m1 2011m1 2013m1

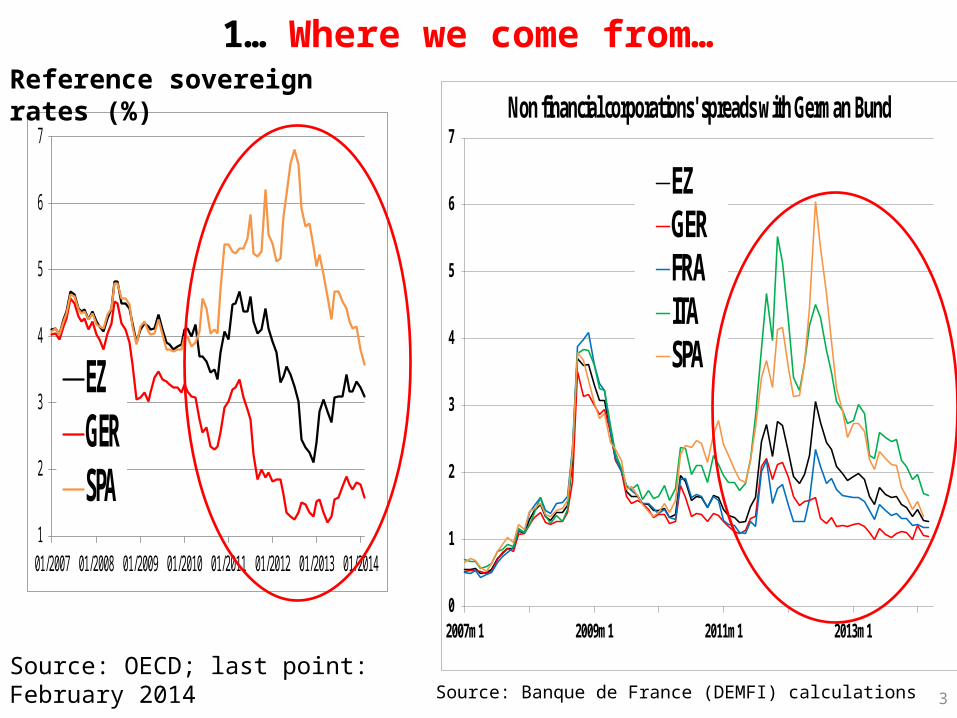

Non financial corporations' spreads with German Bund

EZGERFRAITASPA

Source: Banque de France (DEMFI) calculations

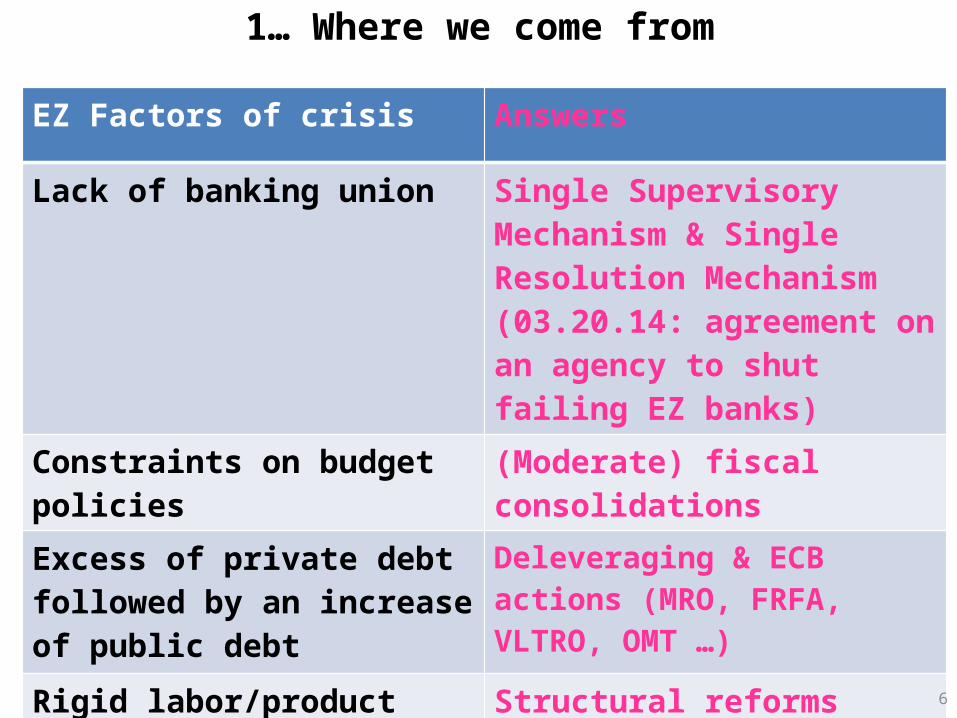

1… Where we come from…

3

Source: OECD; last point: February 2014

1

2

3

4

5

6

7

01/2007 01/2008 01/2009 01/2010 01/2011 01/2012 01/2013 01/2014

EZGERSPA

Reference sovereign rates (%)

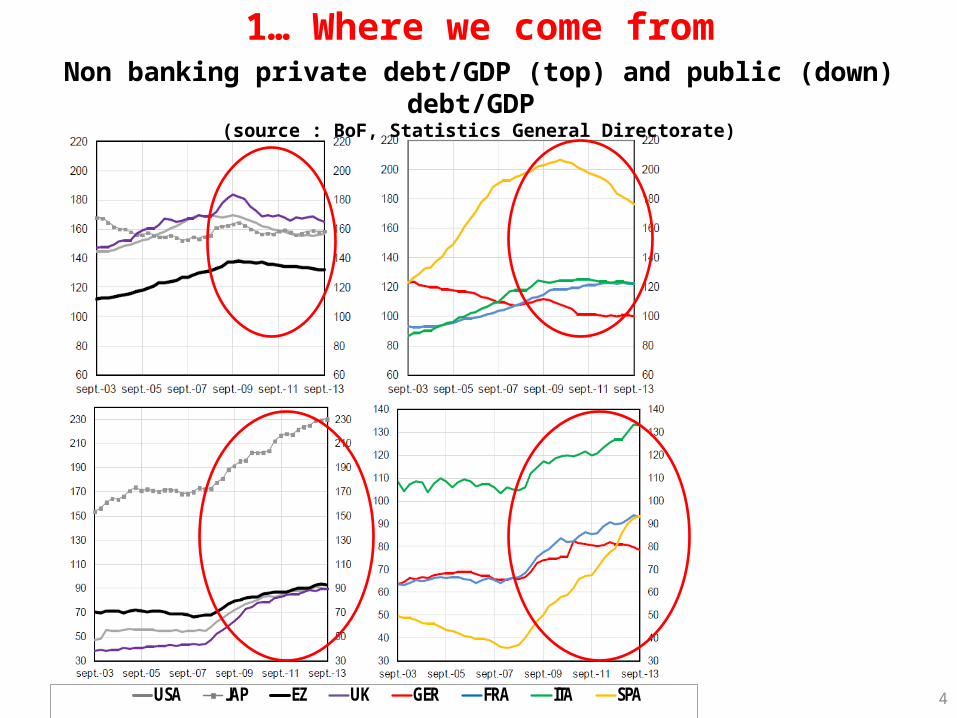

1… Where we come from

4

Non banking private debt/GDP (top) and public (down) debt/GDP (source : BoF, Statistics General Directorate)

0123456789

janv.-00 janv.-00 janv.-00

USA JAP EZ UK GER FRA ITA SPA

5

1… Crisis factors and answers: the role of debt

1… Where we come from

EZ Factors of crisis Answers

Lack of banking union Single Supervisory Mechanism & Single Resolution Mechanism (03.20.14: agreement on an agency to shut failing EZ banks)

Constraints on budget policies (Moderate) fiscal consolidations

Excess of private debt followed by an increase of public debt

Deleveraging & ECB actions (MRO, FRFA, VLTRO, OMT …)

Rigid labor/product markets Structural reforms (increase of flexisecurity: Spain, France …)

6

7

2... Where we are: slow and fragile recoveryGDP growth projections (source: IMF WEO, April 2014)

-5

-4

-3

-2

-1

0

1

2

3

4

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

United States

Eurozone

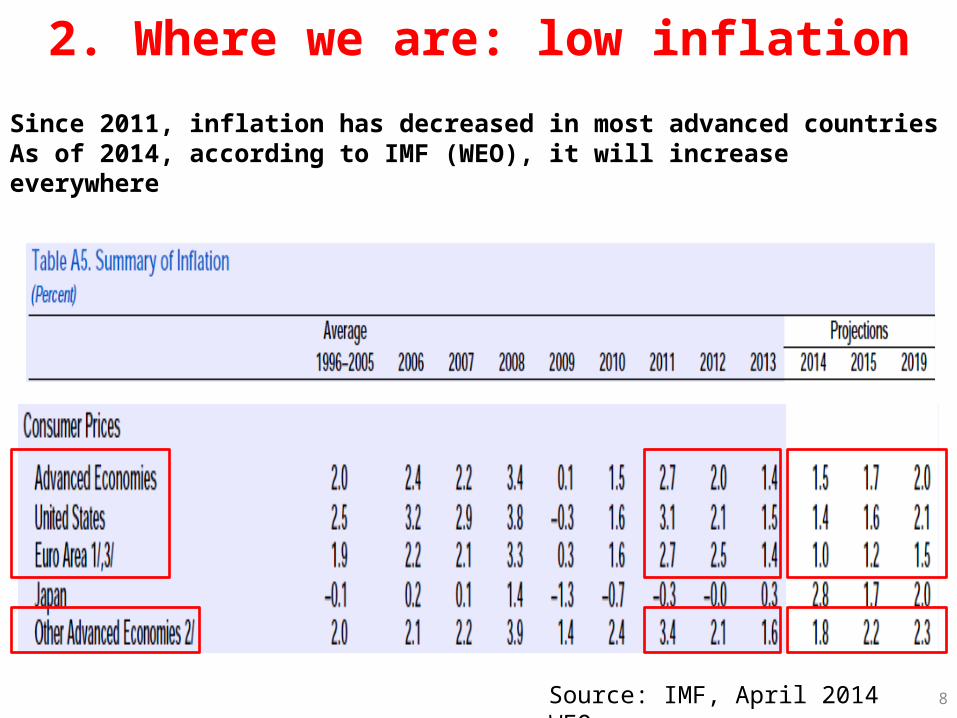

2. Where we are: low inflation

Since 2011, inflation has decreased in most advanced countriesAs of 2014, according to IMF (WEO), it will increase everywhere

8Source: IMF, April 2014 WEO

-4

-2

0

2

4

6

8

-4

-2

0

2

4

6

8

2007 2008 2009 2010 2011 2012 2013 2014

ZEDEFRITESMINMAX

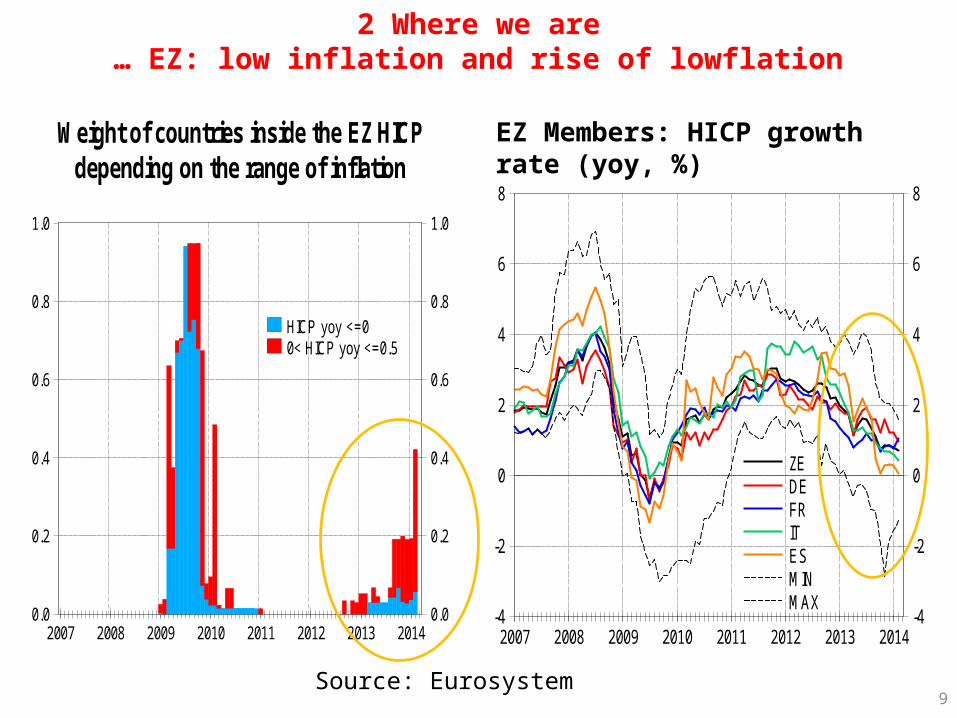

2 Where we are… EZ: low inflation and rise of lowflation

9

0.0

0.2

0.4

0.6

0.8

1.0

0.0

0.2

0.4

0.6

0.8

1.0

2007 2008 2009 2010 2011 2012 2013 2014

HICP yoy <=00< HICP yoy <=0.5

Weight of countries inside the EZ HICPdepending on the range of inflation

Source: Eurosystem

EZ Members: HICP growth rate (yoy, %)

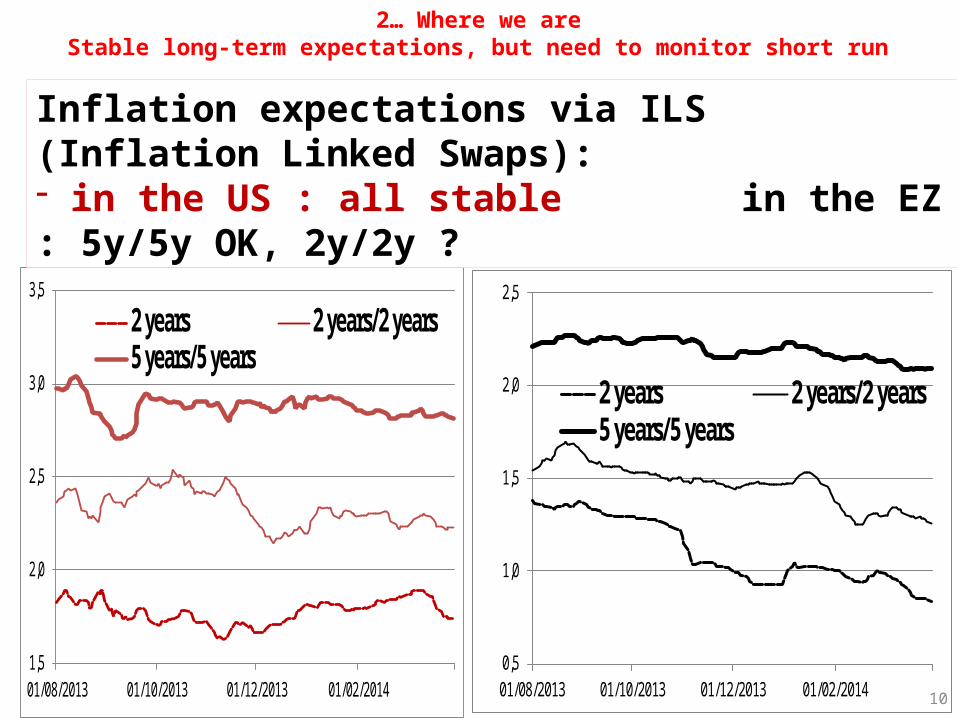

2… Where we areStable long-term expectations, but need to monitor short run

0,5

1,0

1,5

2,0

2,5

01/08/2013 01/10/2013 01/12/2013 01/02/2014

2 years 2 years/2 years5 years/5 years

1,5

2,0

2,5

3,0

3,5

01/08/2013 01/10/2013 01/12/2013 01/02/2014

2 years 2 years/2 years5 years/5 years

10

Inflation expectations via ILS (Inflation Linked Swaps):- in the US : all stable in the EZ : 5y/5y OK, 2y/2y ?

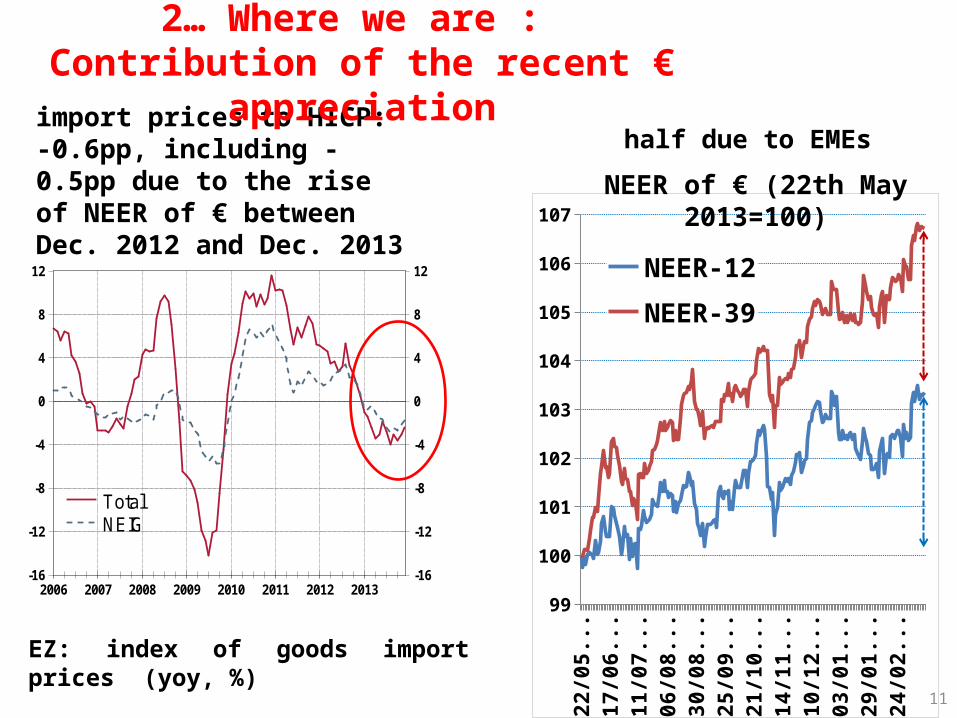

half due to EMEs

11

May

-13

Jun-

13Ju

n-13

Jul-1

3Au

g-13

Aug-

13Se

p-13

Oct

-13

Oct

-13

Nov

-13

Nov

-13

Dec-

13Ja

n-14

Jan-

14Fe

b-14

Mar

-14

99

100

101

102

103

104

105

106

107

NEER-12

NEER-39

NEER of € (22th May 2013=100)

EZ: index of goods import prices (yoy, %)

-16

-12

-8

-4

0

4

8

12

-16

-12

-8

-4

0

4

8

12

2006 2007 2008 2009 2010 2011 2012 2013

TotalNEIG

import prices to HICP:-0.6pp, including -0.5pp due to the rise of NEER of € between Dec. 2012 and Dec. 2013

2… Where we are : Contribution of the recent € appreciation

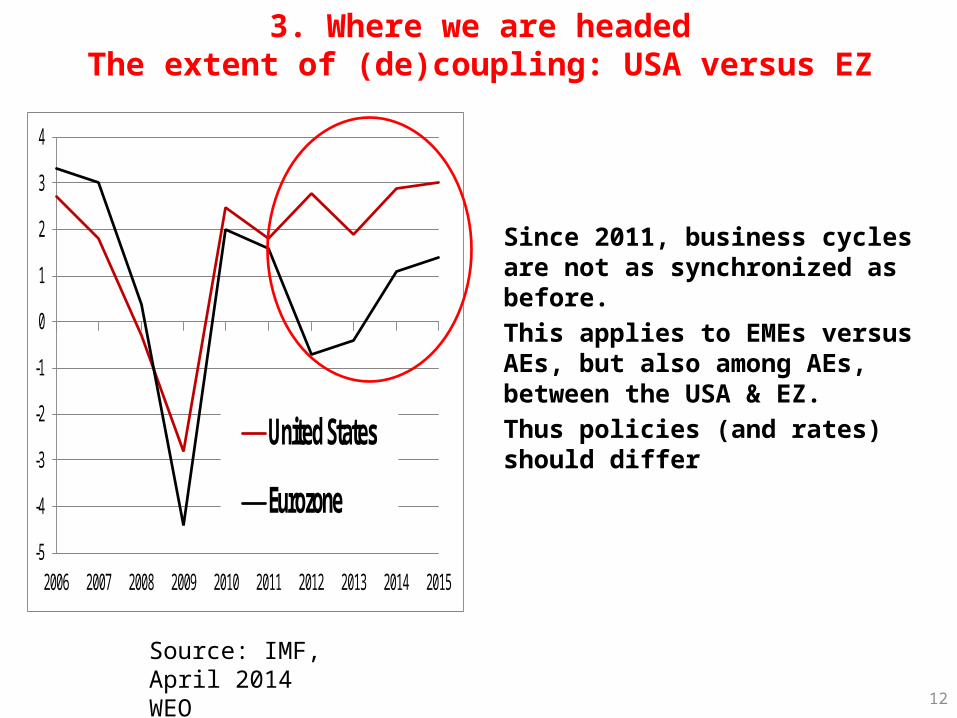

3. Where we are headedThe extent of (de)coupling: USA versus EZ

Since 2011, business cycles are not as synchronized as before.This applies to EMEs versus AEs, but also among AEs, between the USA & EZ. Thus policies (and rates) should differ

12

Source: IMF, April 2014 WEO

-5

-4

-3

-2

-1

0

1

2

3

4

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

United States

Eurozone

Banque de France Direction générale des Études et des Relations internationales

3. Global (de)coupling versus spillovers

14

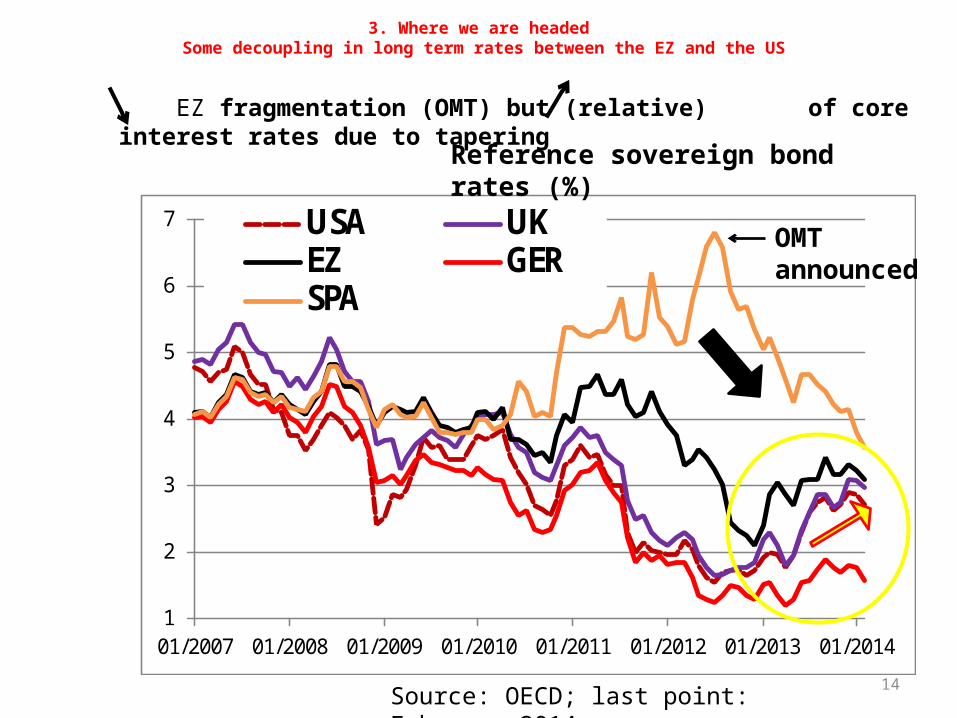

3. Where we are headed Some decoupling in long term rates between the EZ and the US

1

2

3

4

5

6

7

01/2007 01/2008 01/2009 01/2010 01/2011 01/2012 01/2013 01/2014

USA UKEZ GERSPA

EZ fragmentation (OMT) but (relative) of core interest rates due to tapering

Source: OECD; last point: February 2014

OMT announced

Reference sovereign bond rates (%)

3M 6M 1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y-1

0

1

2

3

4

June '13Jul'13 - Feb'14

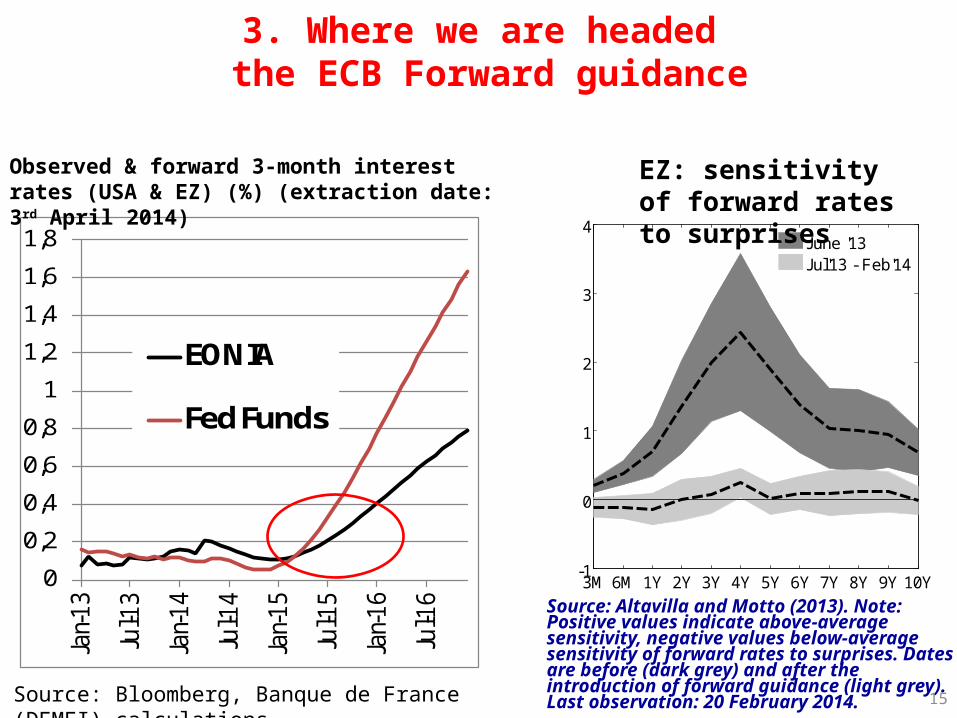

Source: Altavilla and Motto (2013). Note: Positive values indicate above-average sensitivity, negative values below-average sensitivity of forward rates to surprises. Dates are before (dark grey) and after the introduction of forward guidance (light grey). Last observation: 20 February 2014.

15

3. Where we are headed the ECB Forward guidance

0

0,2

0,4

0,6

0,8

1

1,2

1,4

1,6

1,8

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

EONIA

Fed Funds

Source: Bloomberg, Banque de France (DEMFI) calculations

Observed & forward 3-month interest rates (USA & EZ) (%) (extraction date: 3rd April 2014)

EZ: sensitivity of forward rates to surprises

16

Conclusion

The European recovery is under way

Current low inflation should be transitory and does not mean deflation

ECB policy is focused on delivering price stability and it will, whatever happens to US interest rates

17

RESERVE SLIDES

18

Fiscal consolidation but keeping in mind growth

Source: IMF, April 2014 WEO

19

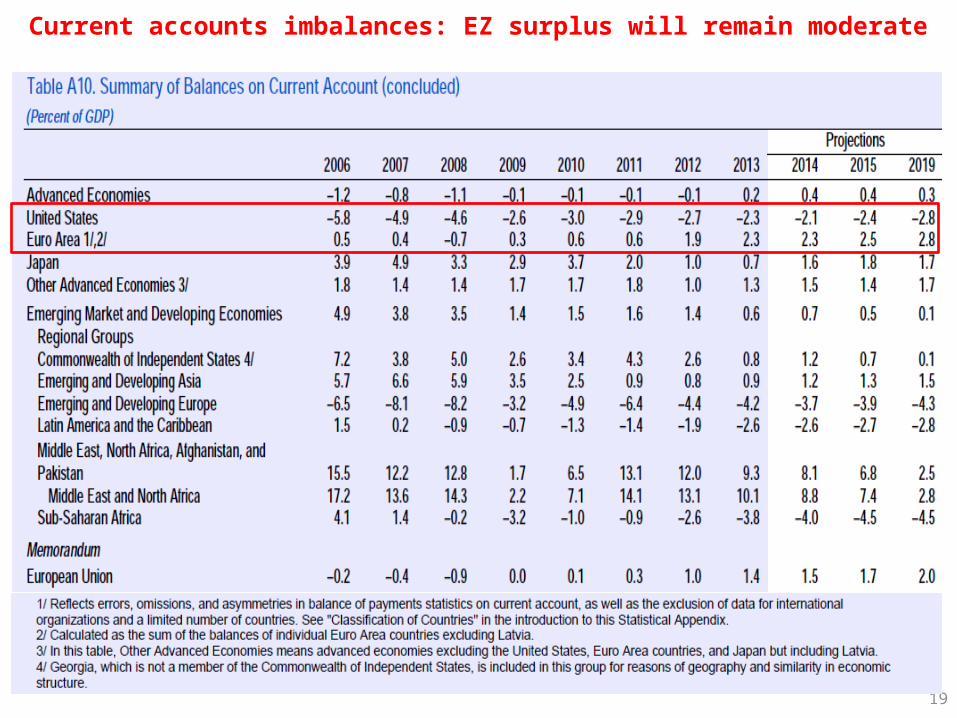

Current accounts imbalances: EZ surplus will remain moderate

20

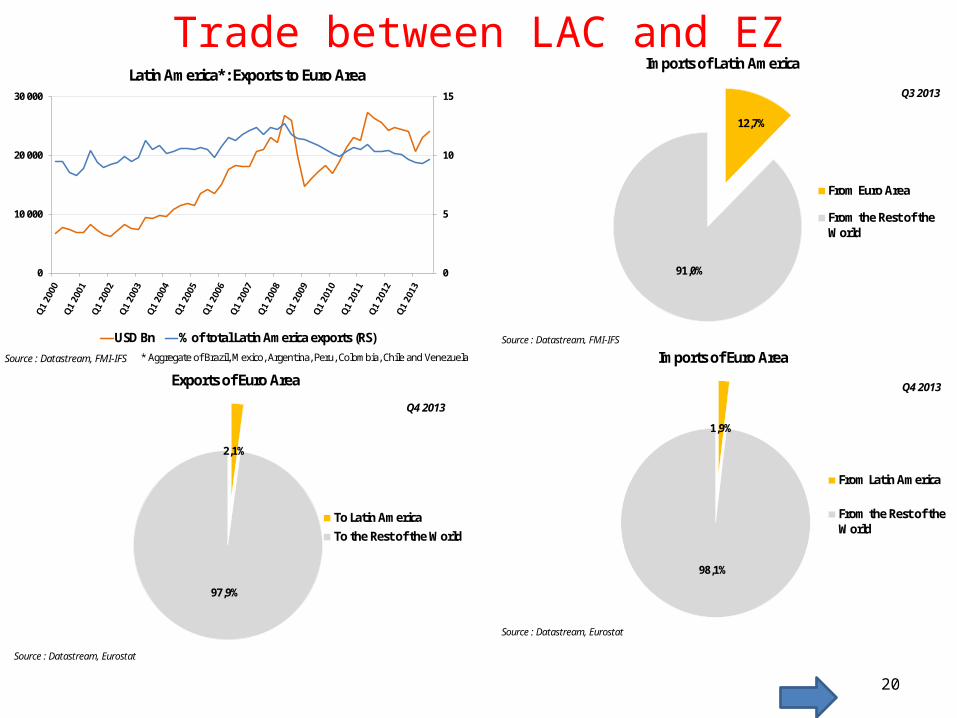

12,7%

91,0%

Imports of Latin America

From Euro Area

From the Rest of theWorld

Source : Datastream, FMI-IFS

Q3 2013

2,1%

97,9%

Exports of Euro Area

To Latin AmericaTo the Rest of the World

Source : Datastream, Eurostat

Q4 2013

1,9%

98,1%

Imports of Euro Area

From Latin America

From the Rest of theWorld

Source : Datastream, Eurostat

Q4 2013

Trade between LAC and EZ

0

5

10

15

0

10 000

20 000

30 000

Latin America*: Exports to Euro Area

USD Bn % of total Latin America exports (RS)

Source : Datastream, FMI-IFS * Aggregate of Brazil, Mexico, Argentina, Peru, Colombia, Chile and Venezuela

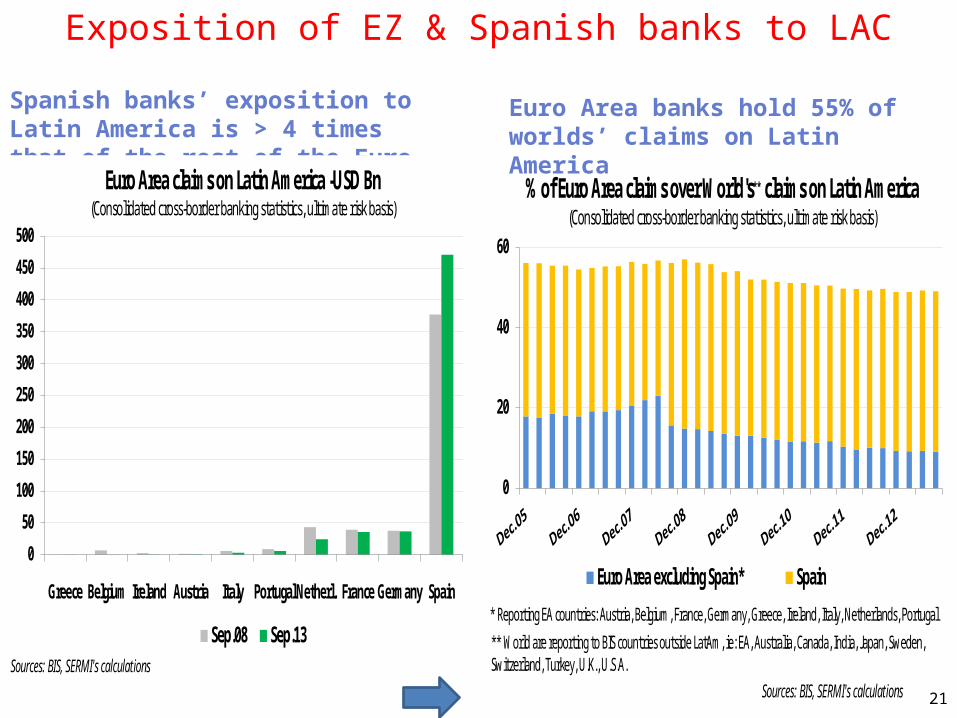

Spanish banks’ exposition to Latin America is > 4 times that of the rest of the Euro Area

0

50

100

150

200

250

300

350

400

450

500

Greece Belgium Ireland Austria Italy Portugal Netherl. France Germany Spain

Sep.08 Sep.13

Euro Area claims on Latin America -USD Bn(Consolidated cross-border banking statistics, ultimate risk basis)

Sources: BIS, SERMI's calculations

0

20

40

60

Euro Area excluding Spain* Spain

% of Euro Area claims over World's** claims on Latin America (Consolidated cross-border banking statistics, ultimate risk basis)

Sources: BIS, SERMI's calculations

* Reporting EA countries: Austria, Belgium, France, Germany, Greece, Ireland, Italy, Netherlands, Portugal

** World are reporting to BIS countries outside LatAm, ie: EA, Australia, Canada, India, Japan, Sweden, Switzerland, Turkey, U.K., U.S.A.

Euro Area banks hold 55% of worlds’ claims on Latin America

21

Exposition of EZ & Spanish banks to LAC