18 kgi-toronto marketing-m_partners-26may15

TRANSCRIPT

A PROFITABLE FUTURE

TORONTO MARKETING May 26/28, 2015

A RICH HISTORY

TSX/AIM:KGI

Forward Looking Statements Cautionary Note Regarding Forward Looking Statements.

This presentation contains statements which constitute ”forward-looking statements”, including statements regarding

the plans, intentions, beliefs and current expectations of the Company with respect to the future business activities

and operating performance of the Company. The words “may”, “would”, “could”, “should”, “will”, “intend”, “plan”,

“anticipate”, “believe”, “estimate”, “expect” and similar expressions, as they relate to the Company, are intended to

identify such forward-looking statements. Forward-looking statements used in this Presentation include, but

may not be limited to; statements regarding the Company’s guidance for fiscal 2015 including ounces

produced and grade assumptions, cash operating cost per ounce and AICC, sustaining capital, revenue,

operating cash flow and free cash flow generation; the ability to bring more higher grade stopes online from

the 5400 level and access to the 5600 level and the timing thereof; the exploration programs and the results

and timing thereof. Investors are cautioned that forward-looking statements are based on the opinions, assumptions

and estimates of management considered reasonable at the date the statements are made such as, without

limitation, opinion, assumptions and estimates of management regarding the Company’s business, its ability to

increase its production capacity and decrease its production cost. Such opinions, assumptions and estimates, are

inherently subject to a variety of risks and uncertainties and other known and unknown factors that could cause

actual events or results to differ materially from those projected in the forward-looking statements. These factors are

discussed in length in the Company's annual Management's Discussion and Analysis and Annual Information Form

for the year ended April 30, 2014. and the Company’s Management's Discussion and Analysis for the interim period

ended January 31, 2015 filed with the securities regulatory authorities in certain provinces of Canada and available at

www.sedar.com.

Should one or more of these risks or uncertainties materialize, or should assumptions underlying the forward-looking

statements prove incorrect, actual results may vary materially from those described herein as intended, planned,

anticipated, believed, estimated or expected. Although the Company has attempted to identify important risks, uncertainties

and factors which could cause actual results to differ materially, there may be others that cause results not to be as

anticipated, estimated or intended. The Company does not intend, and does not assume any obligation, to update these

forward-looking statements except as otherwise required by applicable law.

TSX/AIM:KGI www.klgold.com 2

Investment Highlights

Located in Ontario, one of the safest and lowest risk mining jurisdictions globally

Attractive NI43-101 high grade reserve and resource profile with a long mine life

Growing annual production, declining cost base and improving unit costs

Company returning to profitability and free cash flow

Significant exploration potential with organic growth

Potential upside with a higher gold price and a weaker Canadian dollar

www.klgold.com 3 TSX/AIM:KGI

Experienced and Diverse Board of Directors and Management Team

Experienced Team

Eric Sprott, Chairman of the Board (Non-executive Director)

Barry Cooper, B.Sc., MBA (Non-executive Director)

Pamela Klessig, P.Geo (Non-executive Director)

Barry Olson, M.Sc. (Non-executive Director)

Jeffrey Parr, CA, BA, MBA (Non-executive Director)

Dawn Whittaker, LLB (Non-executive Director)

www.klgold.com 4 TSX/AIM:KGI

George Ogilvie, P.Eng. (Director, President & CEO)

John Thomson, CA (Director, Executive VP & CFO)

Chris Stewart, P.Eng. – VP Operations

Suzette N Ramcharan, CPIR – Director, Investor Relations

Board of Directors

Senior Management

Financial Position

CASH C$80.3 million 1

DEBT C$115 million convertible debentures

KGI.DB: 6% coupon/ $15.00 strike

C$54.5MM mature Jun/2017

KGI.DB.A: 7.5% coupon/ $13.70 strike

C$60.5MM* mature Dec/2017

*In F2015, KGI purchased C$5MM of the 7.5%

3

ROYALTY 2.5% NSR Franco Nevada Corporation

option to buyback 1% by October 31, 2016, at a cost

of US$36MM less any money paid against the 1%

52 Week Performance 2

HIGH C$6.88

LOW C$2.51

www.klgold.com 5 TSX/AIM:KGI

1As at April 30, 2015; 2 As at May 12, 2015 3 See press release dated April 1, 2015, for details on the NCIB

CAPITAL STRUCTURE 1

ISSUED SHARES 80,306,617

Stock Options 4,107,300

Convertible Debentures 8,536,495 3

FULLY DILUTED 92,950,412

MARKET CAP ~488 Million 2

Major Shareholders (~50%) 1

Resolute Funds (10%)

Eric Sprott (10%)

Columbia Wanger Asset Management LLC (8%)

Equinox Partners (7%)

Van Eck Associates Corporation (5%)

Harry Dobson (4%)

ABC Funds (4%)

KGI Share Price Performance

KGI Share Price Vs Gold Price (C$)

Over a 12 month Period

(May 2014 – May 2015)

• KGI share price has outperformed

the POG by 80%

• Steady increase in KGI share price

since January 2015

KGI Share Price Vs Select

Group of Peers (2015 YTD,

as of May 6, 2015)

• KGI share price has

increase by 73% relative

to its peers

• Share price has also

remained above issue

price of bought deal*

www.klgold.com 6 TSX/AIM:KGI

* See press release dated February 18, 2015

Source: Bloomberg as at May 5, 2015

Kirkland Lake Camp

www.klgold.com 7 TSX/AIM:KGI

KGI owns five former

producing high grade mines

Historical production of

~22 Moz’s of gold

Average head grade of

0.44 opt or 15.1 g/t

The Kirkland Lake gold camp

has been producing gold for

over 100 years.

Almost 25 Moz’s has been

produced to date, from

seven mines.

Based on grade, it is one of

the richest gold camps in

the world.

One of the Highest Grade Gold Mines In The World Select Group of Producing Assets with +1Moz’s in Reserves

Mine Operator Location Gold Grade Reserves MRMR

g/t Au Date

Macassa Mine Complex Kirkland Lake Gold Canada (Ontario) (0.56 opt) 19.2 1.5 Moz Dec/2014

Turquoise Ridge Barrick USA (Nevada) 16.9 4.5 Moz Dec/2014

Pogo Gold Sumitomo Corp. USA 12.5 4.9Moz Dec/2013

Gosowong Newcrest Indonesia 12.0 1.2Moz Dec/2014

Moab Khotsong AngloGold Ashanti South Africa 10.0 6.1Moz Dec/2013

Mponeng AngloGold Ashanti South Africa 10.0 14.6Moz Dec/2013

Red Lake Gold Goldcorp Canada 10.0 2.1Moz Dec/2014

TauTona AngloGold Ashanti South Africa 9.1 1.4Moz Dec/2013

Kupol/Dvoinoye Kinross Russia 8.5 2.1Moz Dec/2014

19.2 16.9 12.5 12.0

10.0 10.0 10.0 9.1 8.5

0.05.0

10.015.020.025.0

Gra

de g

/t

Reserve Grades

www.klgold.com 8 TSX/AIM:KGI

Company Source – This is a select group of Companies that illustrate producing mines only with mineral reserves in excess of 1Moz’s (gold only, no equivalent Au ounces shown)

Reserves & Resources (Resources are Exclusive of Reserves)

See Appendix for more disclosure on MRMR statement which is as of December 31 ,2014.

Based on current level of Reserves and 70% conversion of Resources

(@ 200,000 oz p.a), KGI has a 14 year Mine Life

www.klgold.com 9 TSX/AIM:KGI

Property Wide

Mineral Reserves (P&P) Includes the ‘04 & Main Break and SMC

1.5 Moz’s 2.6M tons @ 0.56 opt

(19.2 g/t )

Mineral Resources (M&I) Includes the ‘04 & Main Break, SMC, Near Surface and other

2.0 Moz’s 4.2 M tons @ 0.49 opt

(16.8 g/t )

Mineral Resources (Inferred) Includes the ‘04 & Main Break, SMC, Near Surface and other

1.2 Moz’s 2.1 M tons @ 0.56 opt

(19.2 g/t)

SMC

0.9 Moz’s 1.5 M tons @ 0.65 opt

(22.3 g/t )

0.9 Moz’s 1.4 M tons @ 0.66 opt

(22.6 g/t )

0.9 Moz’s 1.4 M tons @ 0.65 opt

(22.3 g/t )

Breakout of SMC only

South Mine Complex

• Access from 5400L and 5600L allows delineation drilling of

resources, especially below 5600L

• Remains Open at Depth and Across Strike

5025 Level

P+P 28,000 Tons @ 0.48 oz/ton 14,000 Oz’s

M+I 74,000 Tons @ 0.42 oz/ton 32,000 Oz’s

5300 Level

P+P 561,000 Tons @ 0.47 oz/ton 261,000 Oz’s

M+I 245,000 Tons @ 0.43 oz/ton 107,000 Oz’s

5400 Level

P+P 370,000 Tons @ 0.61 oz/ton 226,000 Oz’s

M+I 174,000 Tons @ 0.42 oz/ton 72,000 Oz’s

5600 Level

P+P 239,000 Tons @ 0.77 oz/ton 183,000 Oz’s

M+I 186,000 Tons @ 0.63 oz/ton 117,000 Oz’s

Original Two

Mining Horizons

Third Level

Started May 2014

Developing to

Gain Access

for F2016

OPEN

#3 S

HA

FT

#2 W

INZ

E

www.klgold.com 10 TSX/AIM:KGI

Development Legend

Completed

F2016 Development

F2017 Development

OPEN

OPEN

5700 Level

P+P 202,000 Tons @ 1.03 oz/ton 208,000 Oz’s

M+I 164,000 Tons @ 0.91 oz/ton 96,000 Oz’s

5800 to 6600 Level

P+P 50,000 Tons @ 0.83 oz/ton 41,000 Oz’s

M+I 551,000 Tons @ 0.91 oz/ton 499,000 Oz’s *Drawing not to scale

Reserve Grade Vs Head Grade

0.46 OPT

15.8 GPT

0.65 OPT

22.3 GPT

0.56 OPT

19.2 GPT

0.35 OPT

12.0 GPT

0.46 OPT

15.8 GPT

0.44 OPT

15.1 GPT

Takes into account all proven and probable material from the ‘04 & Main Break, plus all proven and

probable material from all levels of the South Mine Complex.

December 31, 2014 Reserve Calculation

Assumes ~30% of Ore Tons from ‘04 & Main Break, and ~70% of Ore Tons from the 5025, 5300

and 5400 Levels in the South Mine Complex.

F2015 Mine Plan

www.klgold.com 11 TSX/AIM:KGI

F2015 Production Update

Q1 F2015

38,543

93,880

0.45

Q2 F2015

38,335

92,146

0.41

Q3 F2015

39,722

91,148

0.44

Q4 F2015

39,109

92,532

0.42

YTD F2015

155,709

369,706

0.43

Ounces

Sold

Tons

Milled

Head Grade

(opt)

• Fourth stope brought into production on 5400 level during Q4

• 2 Electric Hydraulic Jumbo’s fully operational

• Main ramp towards the 5600 level progressing well and is on schedule

www.klgold.com 12 TSX/AIM:KGI

* Production guidance revised upwards from 140,000 – 155,000 ounces to 153,000 – 157,000 ounces on March 11, 2015

Monthly Production Profile

• Cut-off Grades Raised from 0.18 opt to 0.22 opt.

• Stopped Mining “Incremental Tons”

• Implemented Strict Ore/ Waste Segregation UG

• Increasing UG Delineation Drilling in SMC

• Employing more UG Geologists

• Assay Lab is Manned 24/7

• Restructuring Organization

• Implementing Leadership Training

• Looking to Upgrade MIS

www.klgold.com 13 TSX/AIM:KGI

0.34

0.31 0.30

0.26

0.29

0.45

0.39

0.34

0.37

0.34

0.47

0.51

0.39

0.43

0.41

0.47

0.44

0.42

0.52

0.40

0.35

-

0.10

0.20

0.30

0.40

0.50

0

5,000

10,000

15,000

20,000

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

Oz Recovered

Head Grade

F2015

F2015 YTD Average 0.43 opt

Hea

d G

rad

e (

Ou

nc

es

Pe

r To

n)

Go

ld P

rod

ucti

on

(O

un

ce

s)

0.37

0.40

0.37

0.32

0.41 0.37

0.31

0.33

0.43

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

-

50,000

100,000

150,000

200,000

250,000

07 08 09 10 11 12 13 14 15 16

Go

ld O

un

ce

s

Oz Recovered Guidance Head Grade Linear (Oz Recovered)

Fiscal Year

Previous Guidance

0.43

Annual Production Profile

Expectation Gap

• Fiscal 2015 YTD Actual Head Grade is 0.43 opt Vs guided grade of 0.37 opt

• F2016 Production Guidance increased grade to 0.43 opt from 0.39 opt, assumes 96% recovery and average

throughput of 1,070 tpd. F2017 guidance is as stated in press release dated June 24, 2014

www.klgold.com 14 TSX/AIM:KGI

Hea

d G

rad

e (

Ou

nc

es

Pe

r To

n)

= 200 employees

Gu

ida

nce fo

r F

20

17

an

d F

20

18

will

be

rele

ase

d a

fte

r F

20

15

YE

ea

rnin

gs

Q3 Results

Q3/15 Vs Q3/14

YTD Results

F2015 Vs F2014

CO

ST

S

Cash Cost Per Ton $328

US$281

-5%

-13%

$340

US$302

0%

-7%

Cash Operating Cost Per

Ounce

$766

US$656

-30%

-36%

$813

US$728

-26%

-32%

All-In Cash Costs $1,249

US$1,070

-35%

-40%

$1,289

US$1,153

-38%

-42%

SA

LES

Gold Sales 39,722 +18% 116,600 +23%

Average Sales Price $1,371 0% $1,389 0%

Revenues $54.5MM +18% $161.9MM +24%

CA

SH

FLO

W

Cash Flow from Operations $23.7MM +85% $57.3MM +59%

Free Cash Flow $11.6MM NA $22.8MM NA

Q3 & YTD F2015 Financial Highlights

- All US$ equivalents are converted at the average CAD to USD exchange rate during the reporting period.

- See Pg. 23 for fiscal 2015 guidance on certain financial metrics provided above and Pg.24 in the appendix for further financial results.

www.klgold.com 15 TSX/AIM:KGI

CO

ST

S

SA

LES

C

AS

H

FLO

W

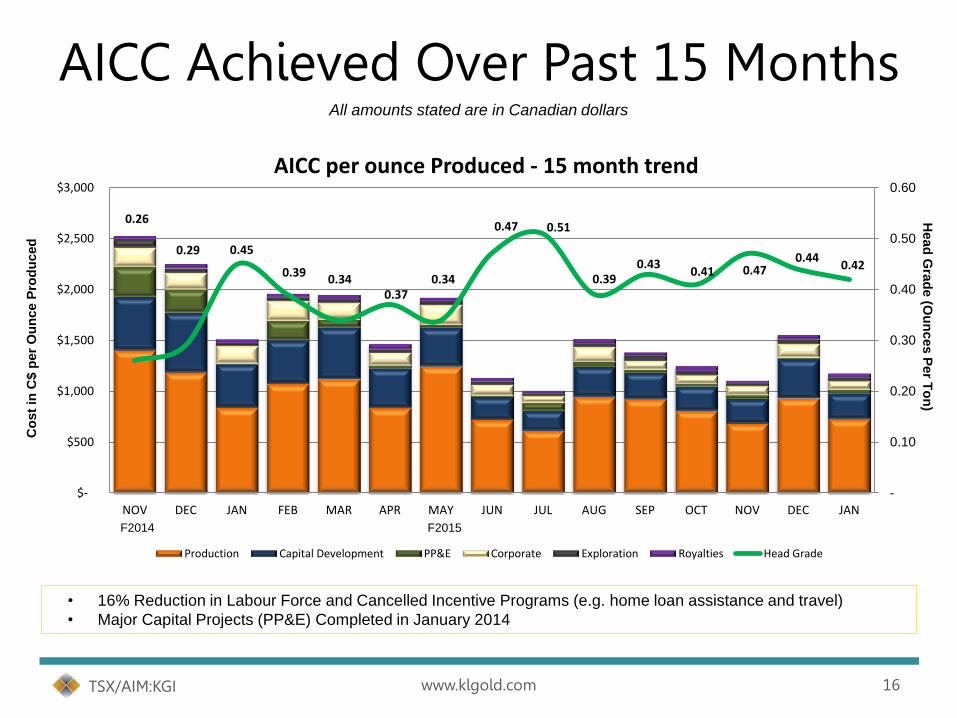

0.26

0.29 0.45

0.39 0.34

0.37 0.34

0.47 0.51

0.39 0.43

0.41 0.47 0.44

0.42

-

0.10

0.20

0.30

0.40

0.50

0.60

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

NOV DEC JAN FEB MAR APR MAY2014

JUN JUL AUG SEP OCT NOV DEC JAN

AICC per ounce Produced - 15 month trend

Production Capital Development PP&E Corporate Exploration Royalties Head Grade

AICC Achieved Over Past 15 Months All amounts stated are in Canadian dollars

• 16% Reduction in Labour Force and Cancelled Incentive Programs (e.g. home loan assistance and travel)

• Major Capital Projects (PP&E) Completed in January 2014

www.klgold.com 16 TSX/AIM:KGI

Co

st

in C

$ p

er

Ou

nce P

rod

uced

H

ead

Gra

de (O

un

ces P

er T

on

)

F2014 F2015

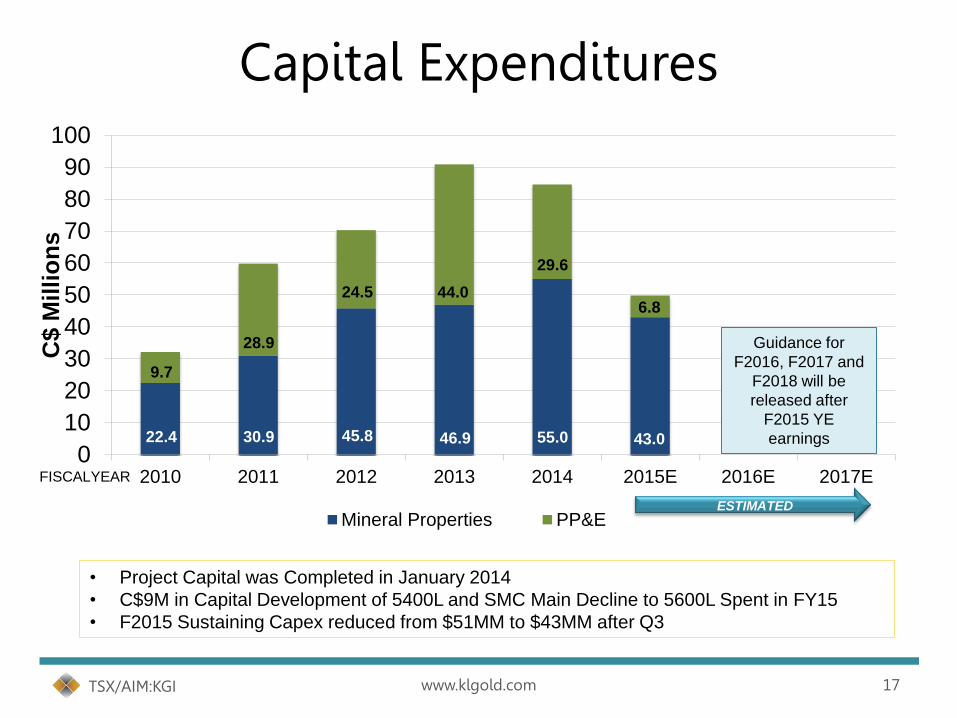

Capital Expenditures

• Project Capital was Completed in January 2014

• C$9M in Capital Development of 5400L and SMC Main Decline to 5600L Spent in FY15

• F2015 Sustaining Capex reduced from $51MM to $43MM after Q3

0

10

20

30

40

50

60

70

80

90

100

2010 2011 2012 2013 2014 2015E 2016E 2017E

C$ M

illi

on

s

Mineral Properties PP&EESTIMATED

9.7

22.4 30.9 45.8 46.9 55.0 43.0 51.0 51.0

28.9

24.5 44.0

29.6

6.8

www.klgold.com 17 TSX/AIM:KGI

FISCALYEAR

Guidance for

F2016, F2017 and

F2018 will be

released after

F2015 YE

earnings

Exploration Potential In A Historic Camp

www.klgold.com 18 TSX/AIM:KGI

Current Underground and

Surface Drilling Targets

Currently mining and

exploring on one of

these five targets.

Three main areas

currently being

explored from

surface and

underground.

Regional exploration

to test eastwards

along the Main Break

will be next phase of

drilling.

SMC Underground Drilling

www.klgold.com 19 TSX/AIM:KGI

UG DRILLING • SMC continues to be expanded

• Multi-ounce intersections

• 3 drills turning underground

• Open in multiple directions

53-2493 (NSZ)

1.85 opt/ 11.6 feet (63.43 gpt/ 3.5 metres)

53-2597 (NSZ)

0.36 opt/14.7 feet (12.34 gpt/ 4.5 metres)

53-2595 (NFZ)

3.55 opt/ 11.4 feet (121.72 gpt/ 3.5 metres)

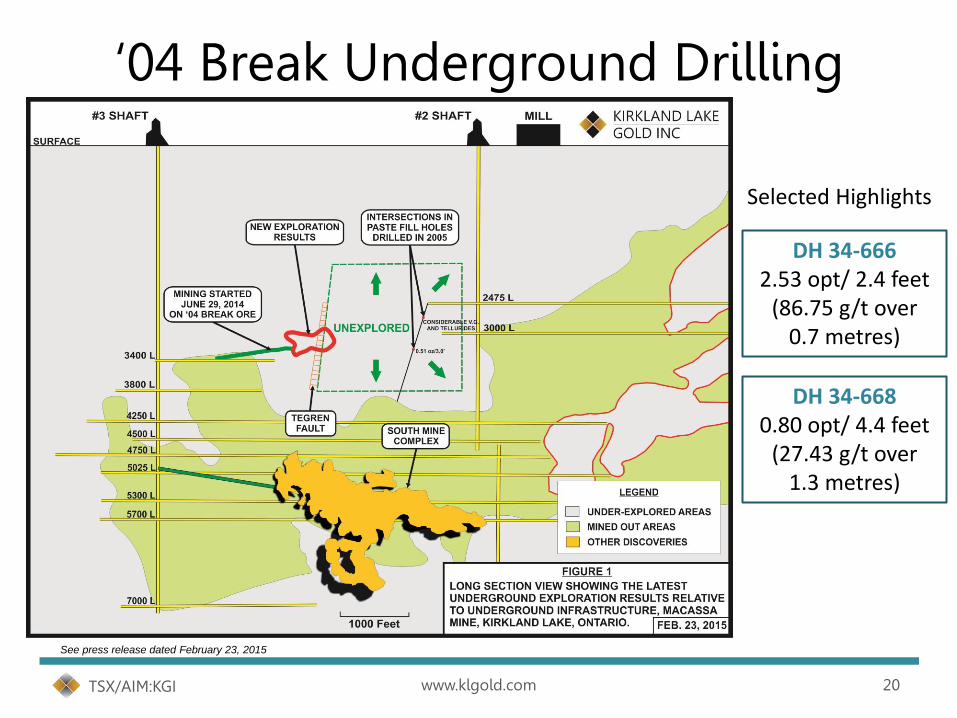

‘04 Break Underground Drilling

www.klgold.com 20 TSX/AIM:KGI

Selected Highlights

DH 34-666 2.53 opt/ 2.4 feet

(86.75 g/t over 0.7 metres)

DH 34-668 0.80 opt/ 4.4 feet

(27.43 g/t over 1.3 metres)

See press release dated February 23, 2015

Near Surface Exploration Target

• Near surface mineralization is within 2 Km’s of mill

• Mill has excess capacity of +/- 1,000 tpd

• Mineralization from 100’ to 1,000’ below surface

• Open across strike

• M&I 330,000 tons @0.34opt (11.7gpt) 112,000 oz

• Infer 100,000 tons @0.42opt (14.4gpt) 42,000 oz

www.klgold.com 21 TSX/AIM:KGI

Outlook for F2015

Guidance Metric YTD 2015

Actual

Revised

Guidance

$800 – 850/ Oz Cash Operating Cost Per Ounce $813

US$723 No Change

$1,250 - 1,350/ Oz AICC Per Ounce Produced $1,289

US$1,144 No Change

$58 million* Capital Expenditures $36 million $43 million

$200 million Revenue $162 million $218 - $222 million

$50 - 60 million Cash Flow from Operations $57 million $73 - $78 million

$15 - 20 million Free Cash Flow Generation $22 million $30 - $35 million

All amounts stated are in Canadian dollars

www.klgold.com 22 TSX/AIM:KGI

* Capital was revised from $58 million to $53 million on October 31, 2014, and revised to $50 million on January 31, 2015

APPENDIX

Notes, additional disclosure and other information

www.klgold.com 23 TSX/AIM:KGI

Analyst Coverage

Firm Analyst

Dundee Securities Joe Fazzini

CIBC World Markets Cosmos Chiu

Macquarie Capital Markets Michael Siperco

National Bank Financial Raj Ray

BMO Capital Markets Brian Quast

Clarus Securities Jamie Spratt

PI Financial Philip Ker

Firm Analyst

M Partners Derek Macpherson

Pareto Securities John McClintock

Mirabaud Securities Richard Morgan

Panmure Gordon & Co Alison Turner

Investec Bank Hunter Hillcoat

Very Independent Research John Tumazos

KIRKLAND LAKE GOLD IS FOLLOWED BY THE ANALYSTS LISTED ABOVE. THIS LIST IS PROVIDED FOR INFORMATION PURPOSES ONLY AND IS

SUBJECT TO CHANGE AS COVERAGE IS ADDED OR DROPPED BY A FIRM.

OPINIONS, ESTIMATES OR FORECASTS REGARDING KIRKLAND LAKE GOLD'S PERFORMANCE THAT ARE MADE BY THESE ANALYSTS ARE THEIRS

ALONE AND DO NOT REPRESENT THE OPINIONS, ESTIMATES OR FORECASTS OF KIRKLAND LAKE GOLD OR ITS MANAGEMENT.

KIRKLAND LAKE GOLD DOES NOT IMPLY ITS ENDORSEMENT OF, OR CONCURRENCE WITH, SUCH INFORMATION, CONCLUSIONS OR

RECOMMENDATIONS AND TAKES NO RESPONSIBILITY FOR MONITORING, SUPPLEMENTING OR CORRECTING ANY INFORMATION OR FORECASTS

PROVIDED BY THE ANALYSTS.

www.klgold.com 24 TSX/AIM:KGI

F2014 & Q3 F2015 Financial Results

Financial FY2015

YTD

FY2014

YTD Y/Y

Change Q3/15 Q2/15 Q3/14

Q3/15

vs.

Q2/15

Q3/15

vs.

Q3/14

Gold Sales

(ounces) 116,600 94,502 +23% 39,722 38,335 33,719 +4% +18%

Average Price Sold

(per ounce)

$1,389

US$1,243

$1,385

US$1,348

0%

- 6%

$1,371

US$1,175

$1,395

US$1,262

$1,369

US$1,280

-2%

-7%

0%

-8%

Revenue (000’s) 161,953 84,737 +24% 54,471 53,479 46,165 +2% +18%

Cash Operating

Cost per Ton

Produced

$340

US$302

$340

US$324

0%

-7%

$328

US$281

$350

US$317

$347

US$324

-6%

-11%

-5%

-13%

Cash Operating

Cost per Ounce

Produced

$813

US$723

$1,109

US$1,073

-26%

-32%

$766

US$656

$889

US$804

$1,094

US$1,023

-14%

-18%

-30%

-36%

All-in Cash Cost

(“AICC”) per Ounce

Produced

$1,289

US$1,144

$2,102

US$2,033

-38%

-42%

$1,249

US$1,070

$1,374

US$1,243

$1,923

US$1,797

-9%

-14%

-35%

-40%

All amounts stated are in Canadian dollars unless otherwise stated

www.klgold.com 25 TSX/AIM:KGI

- All US$ equivalents are converted at the average CAD to USD exchange rate during the reporting period.

- See Pg. 23 for fiscal 2015 guidance on certain financial metrics provided above

$1,073 $1,119

$836

$1,244

$720 $614

$947 $924 $809

$684

$931

$728

$1,250

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$2,200

FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN Q4E

Production Capital Development PP&E Corporate Exploration Royalties

AICC Projection for F2015 All amounts stated are in Canadian dollars

• Projection Based on Assumptions of 1,150 tpd, 0.37 opt and 96% Mill Recovery

• KGI now has three consecutive quarters of Free Cash Flow generation

• AICC excludes any mining and income tax (of which the Company only pays a nominal amount in mining taxes)

www.klgold.com 26 TSX/AIM:KGI

F2015

Co

st

in C

$ p

er

Ou

nce P

rod

uced

F2015_YTD Average Sales Price C$1,389

F2015_YTD AICC C$1,289

C$35MM Bought Deal Offering

www.klgold.com 27 TSX/AIM:KGI

Shares Issued Price

Gross Proceeds

C$30MM Offering 6,900,000 $4.35 $30MM

Over-allotment* 1,035,000 $4.35 $ 5MM

Total 7,935,000 $4.35 $35MM

Notes: - Over-allotment was exercised in full upon closing - Proceeds will be used to strengthen the balance sheet and for general

corporate purposes.

Expansion Capital

• Hoisting system capable of hoisting 3,600 tpd

• Mary-Anne Compartment installed in Shaft providing service cage

• Mill upgraded to handle 2,200 tpd

• Underground infrastructure and battery equipment in place for SMC

www.klgold.com 28 TSX/AIM:KGI

Reserve & Resource Estimates Resources are exclusive of Reserves

Grade Grade Au Grade Grade Au Grade Grade Au

opt g/t (000's) opt g/t (000's) opt g/t (000's)

'04 & Main Break 545 0.43 494 14.7 236 583 0.48 529 16.5 278 1,128 0.46 1023 15.8 514

South Mine Complex 346 0.51 314 17.5 177 1,120 0.69 1016 23.7 773 1,467 0.65 1,331 22.3 949

Macassa Mine Complex 891 0.46 808 15.8 412 1,703 0.62 1,545 21.3 1,051 2,595 0.56 2,354 19.2 1,463

Proven

Tonnes

(000's)

Tons

(000's)

Tonnes

(000's)

ZoneProbable Proven & Probable

Tons

(000's)

Tonnes

(000's)

Tons

(000's)

MINERAL RESERVES - As at December 31, 2014

Note: Columns may not add due to rounding. Macassa Mine Complex reserves the ’04 & Main Break and the SMC.

MINERAL RESOURCES - As at December 31, 2014

Grade Grade Au

opt g/t (000's)

04 & Main Break 485 0.41 440 14.1 201

SMC 1,358 0.65 1,232 22.3 876

Near Surface Target 100 0.42 91 14.4 42

Property Wide 2,114 0.56 1,918 19.2 1,777

ZoneTons (000's) Tonnes (000's)

InferredNote: Columns may not add due to rounding. Property Wide resources include the ’04 &

Main Break, SMC, Near Surface Target, as well as peripheral resources blocks (such as

the Lakeshore Ramp).

www.klgold.com 29 TSX/AIM:KGI

Grade Grade Au Grade Grade Au Grade Grade Au

opt g/t (000's) opt g/t (000's) opt g/t (000's)

04 & Main Break 1063 0.4 964 13.7 430 1148 0.42 1041 14.4 483 2,211 0.41 2006 14.1 913

SMC 33 0.37 30 12.7 12 1377 0.67 1249 23.0 917 1,410 0.66 1279 22.6 929

Near Surface Target - - - - - 330 0.34 299 11.7 112 330 0.34 299 11.7 112

Property Wide 1106 0.4 1003 13.7 447 3,096 0.52 2,809 17.8 1,599 4,202 0.49 3,812 16.8 2,047

Measured

Tons

(000's)

Tonnes

(000's)

ZoneIndicated Measured & Indicated

Tons

(000's)

Tonnes

(000's)

Tons

(000's)

Tonnes

(000's)

QP Info and Notes to Reserves & Resources The reserve and resource estimates have been audited and verified, and the technical disclosure in thie press release dated April 13, 2015, has been

approved, by the Company’s independent reserve and resource engineer, Glenn R. Clark, P. Eng., of Glenn R. Clark & Associates Limited. Mr. Clark

is a ‘qualified person’ under National Instrument 43-101, Standards of Disclosure for Mineral Projects, of the Canadian Securities Administrators. The

report detailing the December 31, 2014, reserve and resource estimates will be filed on SEDAR (www.sedar.com) within 45 days of this press release.

See ‘Notes for Reserves and Resources’ below for key assumptions, parameters and methods used to estimate the foregoing reserves and

resources.

Notes for Reserves and Resources:

The reserves and resources have been classified according to the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Standards on

Mineral Resources and Reserves: Definition and Guidelines (December 2005).

1. The reserves and resources are estimated using the polygonal method.

2. Resources do not include reserves.

3. All intersections are calculated to a 6.0 foot minimum horizontal mining width for structures dipping at greater than 45 degrees. The minimum

mining height for structures dipping less than 45 degrees is 9.0 feet.

4. Dilution is added to reserves at varying rates depending on the mining method, and the width of the ore. The average dilution of the reserves at

December 31, 2014, is 27% at 0.02 opt, marginally up from an average of 24.0% the previous year. Long-hole stopes are diluted by anywhere

between 50-100% (mostly 50%). Cut and fill stopes are diluted by anywhere between 10-50%.

5. All higher grades are cut to 3.50 opt. Based on a statistical analysis completed by Scott Wilson Roscoe Postle Associates Inc. in 2007, the

Company has implemented various higher grade cutting factors for four zones in the South Mine Complex. These four zones are the New South

Zone (7.20 opt), Lower D North (9.30 opt), Lower D North Footwall (4.80 opt), and the #7 and #7 HW Zones (6.40 opt). Cut-off grades of 0.22 opt

and 0.18 opt are used for reserve and resource calculations respectively, depending on the location, and economics of the block. Generally, a cut-

off of 0.22 opt is required on a whole-block basis to achieve profitability and reserve classification. It is possible to have sub-blocks within an ore

reserve block that assay less than any cut-off which have been incorporated for mining or geotechnical reasons. Ore blocks that grade between

0.18 opt and the cut-off of 0.22 opt have been classified as resource. The cut-off grade for near-surface resources (surface to -1,000 foot

elevation) is 0.12 opt. An internal report completed by Roscoe Postle and Associates in October 2014, suggest that the cutting factor for

mineralization on the Amalgamated Trend be set at 2.50 opt. This grade capping was implemented by the Company and incorporated in the

estimates for 2014.

6. The area of influence of the proven and measured categories are 30 feet from development chip samples, probable and indicated categories are

50 feet of radius from a known sample point (drill holes) and inferred is another 50 feet of influence (between 50 – 100 feet).

7. A 94.2% tonnage recovery is used. Continuity of the veins appears very good.

8. The assumptions used include CAD$1,350.00 (US$1,200) per ounce of gold.

9. The Company is not aware of any environmental, permitting, legal, title, taxation, socio-political, marketing or other issue that may materially affect

its estimate of mineral resources.

10. Mineral resources which are not mineral reserves do not have demonstrated economic viability.

www.klgold.com 30 TSX/AIM:KGI

WWW.KLGOLD.COM

Suzette N Ramcharan, CPIR

Director of Investor Relations

+1-416-840-7884

Mobile: +1-647-284-5315

Tim Blythe / Halimah Hussain

(Blytheweigh)

Investor Relations / PR

+44-207-138-3204

TSX /AIM: KGI