16 annual report - nicgh.orgnicgh.org/wp-content/uploads/2018/02/nic_annual-report_2016.pdf · 2016...

TRANSCRIPT

& FINANCIAL STATEMENTSANNUAL REPORT16

National Insurance Commission2016 | Annual Report

National Insurance Commission

For More Information And Reservation, Please Call The Following Numbers 0302 238300 | 0302 238301

Location: Appiah-Ampofo House, Independence Ave, National Insurance CommissionTel: 233 302 238 300/1 | Fax: 233 302 237 248 | Email: [email protected] | Website: www.nicgh.Org

Ultra Modern Hall | Modern and State of the Art Facilities | Secured and Large Car Park | Central Location | Competitive Price | Spacious Lawns

NATIONAL INSURANCE COMMISSION Appiah-Ampofo House

Standard Conference Package Hall Rental (Seating Capacity 200)Power Point ProjectorP.A SystemOne Co�ee BreakBu�et Lunch Mineral WaterNote Pad, Folder And PenInternet Connectivity

Foreword 7

Chairman’s Report 8

The National Insurance CommissionCorporate Information 11

NIC’s Operations 12

Ghana Insurance Market Report2016 Economic Review 21

Ghana Insurance Market Report (2012 – 2016) 22

Financial & Ratio Analysis 36

Appendices2016 NIC Financial Reports 72

2016 Fire Maintenance Fund Financial Reports 86

List of Registered Insurance Companies 96

List of Registered Reinsurance Companies 103

List of Registered Broking Companies 104

Content

s

2016 Annual Report National Insurance Commission

6

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

7

FOREWORDIntroductionThe National Insurance Commission (NIC) issued the Governance and Risk Management framework in 2015. The activities of NIC in 2016 was geared at ensuring that the principles and values set out in the Governance and Risk Management framework are embedded in the regulated entities operations.

To this end, the NIC organised a number of workshops for key stakeholders in the insurance industry to educate them on what is expected of them in relation to the Governance and Risk Management framework.

In addition, the NIC worked to ensure that all the regulated entities were appropriately capitalised as per the NIC requirements. This was coupled with on-site inspections to ensure that firms have adequate measures in place to mitigate the risks inherent in their operations.

New Insurance Act

The NIC is in the process of reviewing the Insurance Act to make it more appropriate, given the changes witnessed in the insurance landscape. This will also ensure that the new Insurance bill, if passed into an Act, will be compliant with the most recent Insurance Core Principles (ICPs) of the International Association of Insurance Supervisors (IAIS).

The frameworks, directives and guidelines that the NIC has issued in the recent past will be included in the new Insurance Act. Other new areas to be included are as follows:

Group-Wide Supervision

It is generally accepted that the stand-alone view of an insurance company, which is part of a group of companies, does not give a full picture of the risks that policyholders are exposed to. This is the main risk that the following ICPs seeks to mitigate:

■ ICP 23: Group Wide Supervision

■ ICP 24: Macro Prudential Surveillance and Insurance Supervision

■ ICP 25 & 26: Cross Boarder Collaboration of the Supervision of Insurance Groups that are in more than one country.

However, a group-wide approach to the regulation of insurance groups is not currently part of the insurance regulations in Ghana. One of the key activities that the NIC will undertake in the coming years is to implement

a Group-wide supervisory framework.

Risk Based Capital Requirements

A key component of Risk Based Solvency Regime is Risk Based Capital Requirements. Risk Based Capital Requirement seeks to ensure that the capital requirement of an insurer is commensurate with the risks the insurer faces.

This will encourage robust risk management practices in (re) insurance companies in Ghana, as firms with robust risk management framework will hold less capital.

The introduction of the Risk Based Capital requirements will ensure that the regulation of insurance in Ghana is in line with international best practices such as Solvency II in EU, SAM in South Africa and C-ROSS in China. It will also make our regulations compliant with the ICPs.

Compulsory Insurance

There are currently two insurance products that are compulsory in Ghana. These are:

■ Third Party Motor Insurance

■ Fire Insurance for Private Commercial Buildings.

In addition to this, the NIC is considering other insurance products that should be compulsory. The aim of this exercise is to protect life and property as well as increase insurance penetration.

2016 Annual Report National Insurance Commission

8

1. INTRODUCTION

The National Insurance Commission (NIC) implemented various reforms in 2016. The Commission issued guidelines on Financial Conditions Reports, approval of Commission Rates, introduced the Risk Based Capital Requirement and Group-wide Supervision Framework. The Commission also organised workshops for key stakeholders to educate them on the corporate governance and risk management frameworks.

All the initiatives taken and directives or guidelines issued in 2016 were aimed at improving the operational efficiency of the regulated entities.

2. GUIDELINES ON COMMISSION RATES

The NIC in accordance with the requirements of section 77 of the Insurance Act 2006, Act 724 approved minimum commission rates payable to insurers and brokers for overseas facultative reinsurance placements of global multinational businesses by foreign intermediaries on the Ghanaian market.

3. ANTI-MONEY LAUNDERING AND COUNTER-ING THE FINANCING OF TERRORISM (AML/CFT)

Based on the Financial Action Task Force on Money Laundering (FATF) recommendations, the insurance industry was subjected to second round mutual evaluation in 2016. The Commission issued guidelines on Know Your Customer (KYC), Customer Due Diligence (CDD), Enhance Due Diligence (EDD), Beneficial Ownership, Independent Audit Assessment, Suspicious Transaction Reports, Record Keeping and Monitoring of Employee Conduct.

4. ENFORCEMENT OF COMPULSORY FIRE IN-SURANCE OF PRIVATE COMMERCIAL BUILD-INGS

The Compulsory Fire Insurance Task Force undertook several enforcement actions in Accra, Takoradi, Cape Coast, Tamale, Wa and Bolgatanga during the year under consideration. They inspected five hundred and seventy-three (573) Commercial buildings to demand evidence of compulsory fire insurance cover.

Out of the 573 buildings inspected 344 of them had procured compulsory fire insurance policies while the remaining 229 had not procured one as required under the Law.

The task force therefore arrested managers of the buildings and threatened to prosecute them if they failed to comply with the directive. They were further requested to report back to the various Police Headquarters with evidence of compliance.

Thereafter, managers of the 229 buildings had duly complied with the directive, with majority of them complying within 48 hours of arrest.

5. IMPLEMENTATION OF SOLVENCY FRAME-WORK

The New Solvency Frameworks for Life and Non-Life insurers were issued during the year after extensive consultations with all stakeholders on the Framework. This guideline uses a risk-sensitive approach to determining the solvency of insurance companies. The compliance date for the new solvency framework was 31st December, 2016.

In view of the above the commission issued a directive in 2016 to all life, non-life and reinsurance companies to maintain the recommended solvency levels.

6. IMPLEMENTATION OF GOVERNANCE AND RISK MANAGEMENT FRAMEWORK

The NIC as part of measures to adopt the Risk-Based approach to Supervision of Insurers, developed a Governance and Risk Management Framework to guide the operational activities of insurers as well as enhance the effective supervision of the Insurance and Reinsurance Companies.

Subsequent to the issuance of the frameworks the Commission organised capacity building seminars for Boards and Risk management control functions of all insurance and reinsurance companies to facilitate effective implementation. The Commission further issued directives on the requirements of the frameworks.

CHAIRMAN’S REPORTMr. Lionel Molbila

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

9

7. RISK BASED SUPERVISION AND LEGAL FRAME-WORK

Risk Based On-Site inspections: In line with the implementation of its Risk Based Supervision Framework, the NIC inspected a number of companies to enable it determine their Risk Rating and the way forward.

The Commission provided feedback on a set of the financial condition reports (FCR) submitted by companies. A key part was the need for regular stress and scenario testing.

The Commission issued a directive that set out the minimum set of stresses and scenarios that companies are required to undertake as part of the FCR reports.

8. INDUSTRY PERFORMANCE

Some key performance indicators of the industry is summarised below:

LIFE

2016 (GHS M) 2015 (GHS M) GROWTH RATE

TOTAL ASSETS 2241 1744 28%

TOTAL INVESTMENTS 1939 1465 32%

ACTUARIAL LIABILITIES 1434 1165 23%

TOTAL CAPITALIZATION 649 463 40%

NON-LIFE

2016 (GHS M) 2015 (GHS M) GROWTH RATE

TOTAL ASSETS 1506 1320 14%

TOTAL INVESTMENTS 886 620 43%

TECHNICAL PROVISIONS 547 566 (3.4)%

TOTAL CAPITALIZATION 704 545 29%

Industry gross premium amounted to GHC 1,929million at year end 2016. This represents a growth of 24% from GHC 1,560million over the same period in 2015. Total premium for life insurance stood at GHC 859m while non-life business amounted to GHC 1070m. This represented a contribution of 45% and 55% respectively in 2016 compares with a similar contribution of 45% and 55% in 2015.

YEAR PREMIUM INCOME(GHS M) GROWTH RATE

2016 1,928,838,573 24%

2015 1,560,679,185 26%

2014 1,239,853,442 17.8%

2013 1,052,090,981 23.6%

2012 850,657,054 35.3%

2011 628,528,775 37.2%

2010 458,117,746 33.5%

2009 342,973,719

9. INSURANCE PENETRATION

Insurance penetration is still very low in the country. Insurance penetration, which is defined as the contribution of total insurance premiums to Gross Domestic Product (GDP) is still less than 2%. Conscious efforts are being made to improve the penetration through the encouragement and development of microinsurance as well as the enforcement of compulsory insurances in the country.

10. CONCLUSION

The year 2016 was likewise interesting but challenging as many difficult decisions were made. It included Directives on the implementation of the New Solvency Requirements and Risk Based Onsite Inspections; implementation of Governance and Risk Management Framework; and Financial Condition Reports (FCR).

These developments and directives will assist to improve operational efficiency of the insurance industry.

2016 Annual Report National Insurance Commission

10

CORPORATE INFORMATION

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

11

CORPORATE INFORMATION

Board of Directors: Mr. Lionel Molbila Chairman

Miss. Lydia Lariba Bawa Commissioner of Insurance

Mr. Samuel Amankwah Member

Mr. Justin Amenuvor Member

Dr. Albert Gemegah Member

Ms. Sarah Fafa Kpodo Member

Mr. Emmanuel Baba Mahama Member

Secretary: Mrs. Emma Ocran

Management Team: Miss. Lydia Lariba Bawa Commissioner of Insurance

Mr. Simon N. K. Davor Deputy Commissioner of Insurance

Mrs. Emma Ocran Director, Legal Services

Mr. Michael Kofi Andoh Head, Supervision

Mr. Moses Ackah-Jayne Ag. Head, Finance

Mr. Joseph Bentor Head, Marketing, Research & External Relations

Mr. Martin Dornor Abayateye Head, Internal Audit

Auditors: Boateng, Offei & Co

Correspondent firm; Grant Thornton International

Chartered Accountants

P.O. Box CT 718

Cantonments, Accra

Tel: 0302-779065 / 0573233718/9

Bankers: Societe Generale Ghana

Universal Merchant Bank (Ghana) Limited

Cal Bank Limited

GCB Bank Limited

HFC Bank (Ghana) Limited

Zenith Bank (Ghana) Limited

The Royal Bank Ghana Limited

Registered office: National Insurance Commission

Appiah- Ampofo House

No. 67 Independence Avenue

North Ridge

P. O. Box CT 3456

Cantonments, Accra

Website: www.nicgh.org

Email Address: [email protected]

2016 Annual Report National Insurance Commission

12

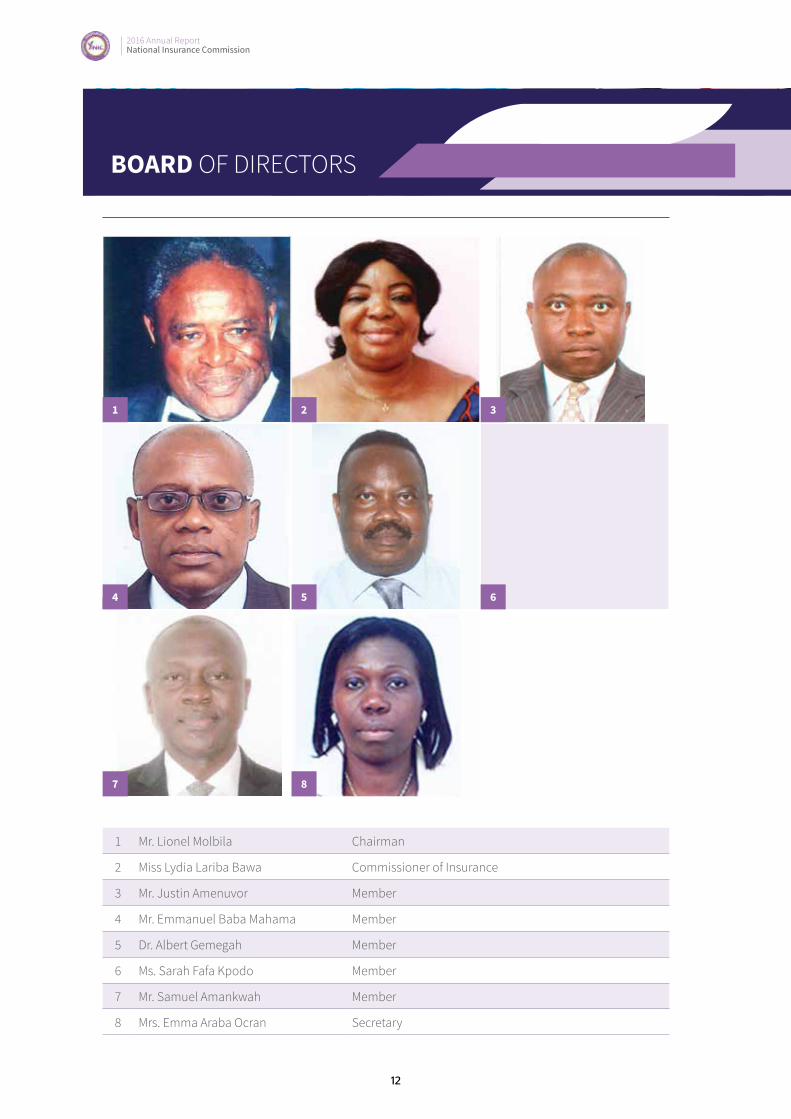

1 Mr. Lionel Molbila Chairman

2 Miss Lydia Lariba Bawa Commissioner of Insurance

3 Mr. Justin Amenuvor Member

4 Mr. Emmanuel Baba Mahama Member

5 Dr. Albert Gemegah Member

6 Ms. Sarah Fafa Kpodo Member

7 Mr. Samuel Amankwah Member

8 Mrs. Emma Araba Ocran Secretary

BOARD OF DIRECTORS

1

4

7

2

5

8

3

6

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

13

1

5

2

6

3 4

7

1 Miss Lydia Lariba Bawa Commissioner of Insurance

2 Mr. Simon N. K. Davor Deputy Commissioner of Insurance

3 Mrs. Emma Araba Ocran Director, Legal Services

4 Mr. Michael Kofi Andoh Head, Supervision

5 Mr. Joseph Bentor Head, Marketing, Research & External Relations

6 Mr. Martin Dornor Abayateye Head, Internal Audit

7 Mr. Moses Ackah-Jayne Acting Head, Finance and Administration

MANAGEMENT

2016 Annual Report National Insurance Commission

14

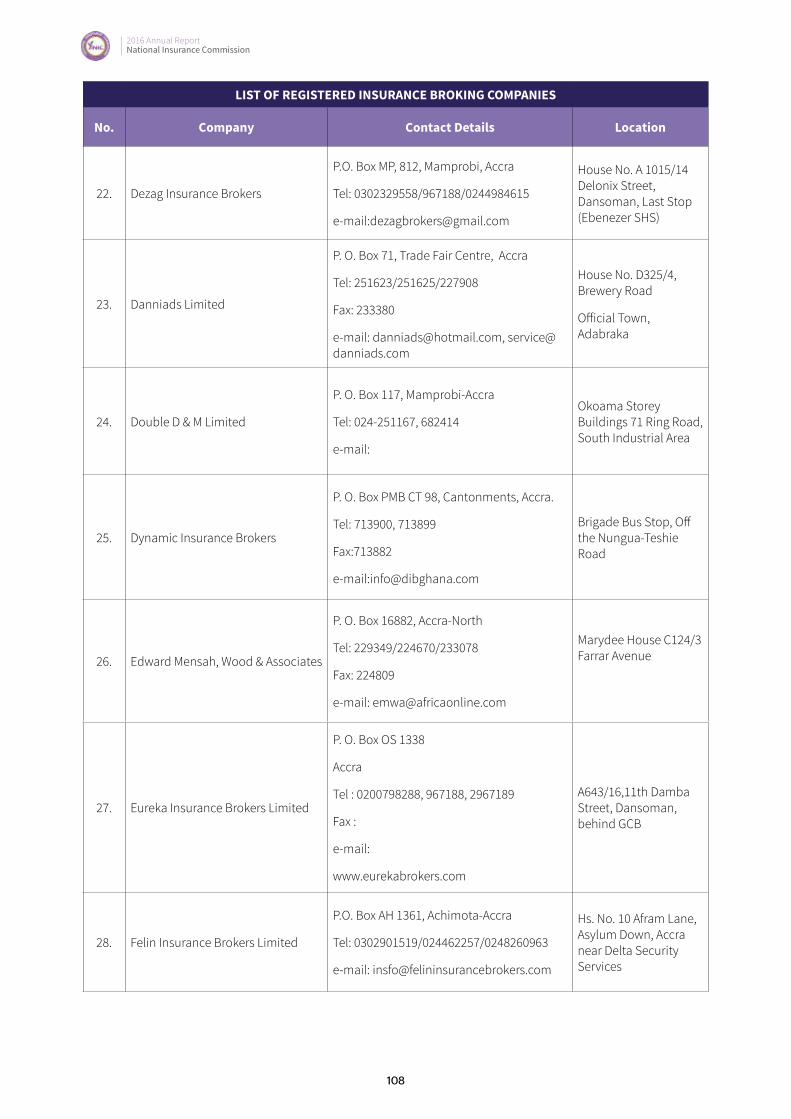

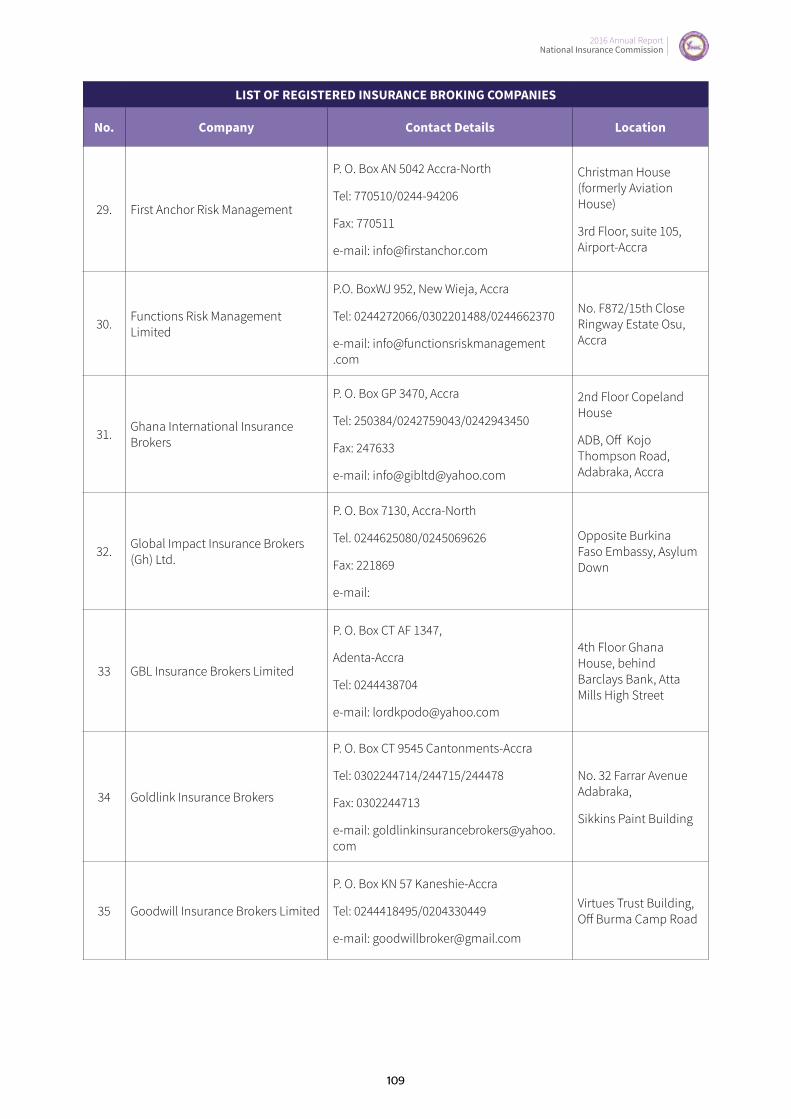

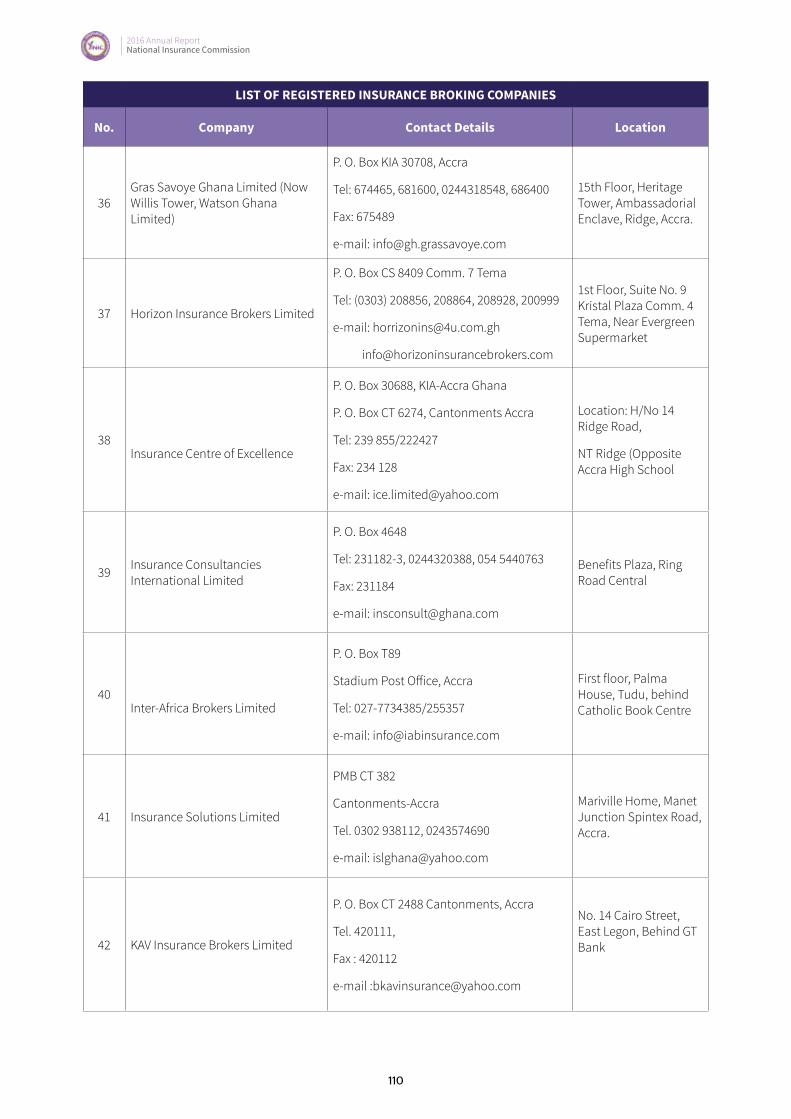

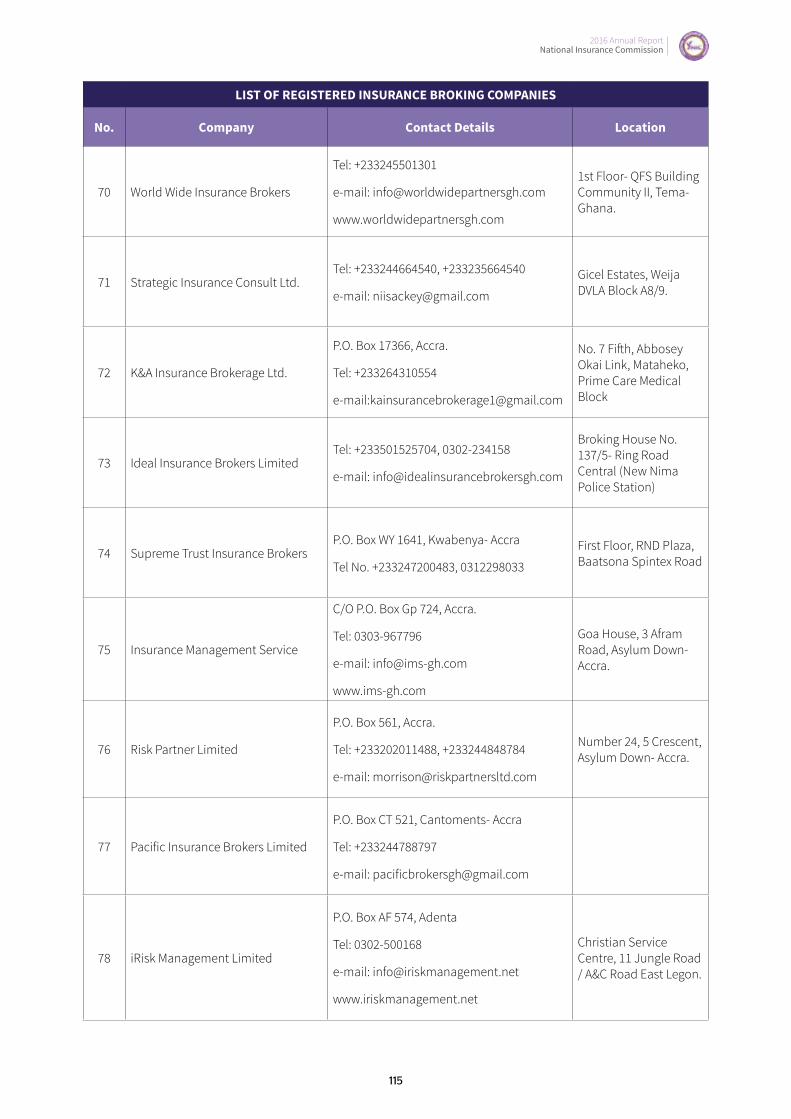

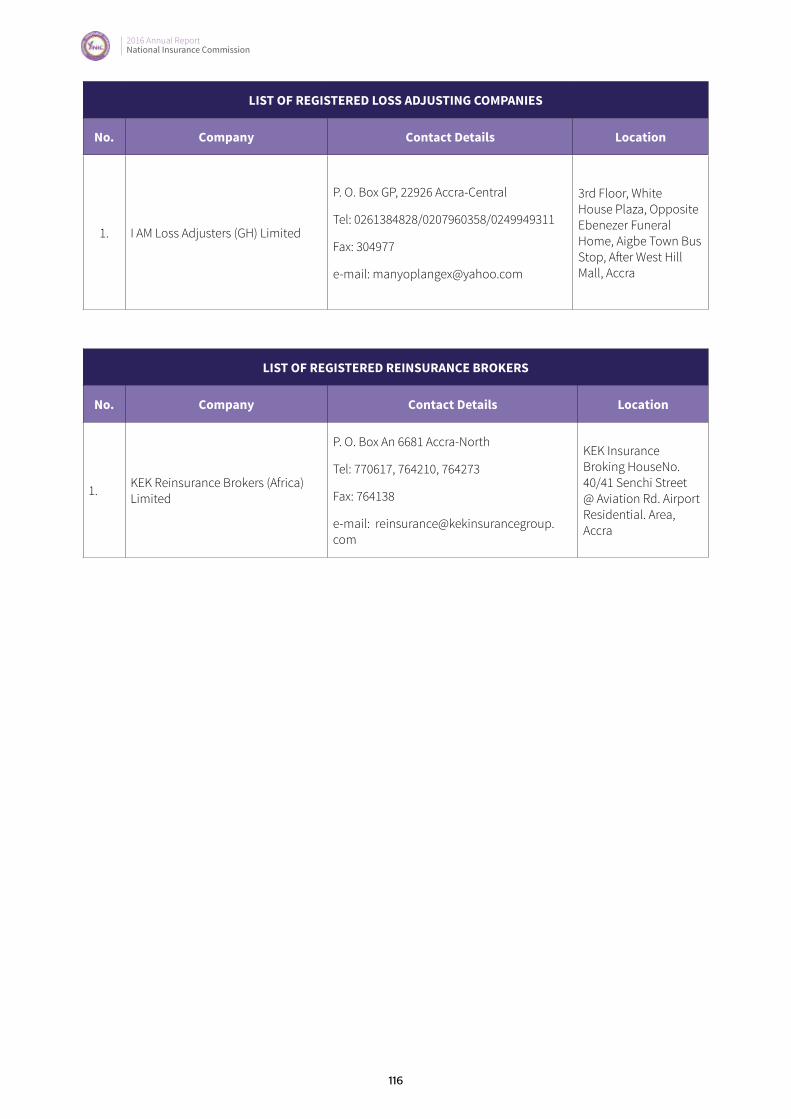

LICENSINGA total of fourteen (14) companies were licensed in 2016. One (1) Life, two (2) Non-Life companies, one (1) Loss Adjuster, and ten (10) Broking companies. The year ended with twenty-seven (27) Non-life, twenty-four (24) Life, three (3) Reinsurance and seventy-eight (78) Broking companies.

The 2 non-life companies were Loyalty Insurance Company Limited, located within the Shippers’ Authority building in Accra, and Multi Insurance Company Limited, with its head office in Kumasi. African Life Assurance Limited was also licensed within the year.

I AM Loss Adjusters & Surveyors Ghana Limited was the second loss adjusting company to be licensed since the inception of the Insurance Act, 2006 (Act 724).

The ten (10) new entrants to the broking sector are listed below:

i. Insurance Management Services Limited

ii. Worldwide Insurance Brokers Limited

iii. IRisk Management Limited

iv. Risk Partners Limited

v. Pacific Insurance Brokers Limited

vi. Strategic Insurance Consult Limited

vii. Anchor Premier Brokerage Limited

viii. Ideal Insurance Brokers Limited

ix. K & A Insurance Brokers Limited

x. Supreme Trust Insurance Brokers Limited

MergerThe NIC also approved a merger between Regency Alliance Insurance Limited and Nem Insurance Ghana Limited to form RegencyNem Insurance Ghana Limited. The Company’s equity is owned 60% and

40% between Regency Alliance and Nem Insurance respectively.

Regulatory DevelopmentsOne of the key objectives of the NIC in 2016 was the embedding of the Governance and Risk Management Frameworks into the operations of the regulated entities. As part of this, the National Insurance Commission (NIC) in Conjunction with the Ghana Insurance College (GIC) organised Directors’ Colleges for the Boards of Insurance and Reinsurance Companies. The purpose of this was to set out what was expected of the Board with regards to corporate governance and risk management.

In addition to the training for the Boards, the NIC also organised workshops for the following control functions:

1. Risk Management function

2. Internal audit function

3. Compliance function

4. Actuarial function

The purpose of these training programme was to expose the control functions to what is required of them as control functions and the tools they can use to achieve these objectives.

Risk based on-site inspectionsDuring the year 2016, the National Insurance Commission (NIC) undertook a number of risk based inspections. This assessed the risks inherent in the firms and the internal controls the firms had in place to mitigate these risks.

Circulars and Guidelines issued in the year 2016The table below summarises the Circulars and Guidance issued by the NIC in 2016.

NIC OPERATIONS

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

15

No Circulars and Guidelines Issued for year 2016

1 Guidelines on Financial Condition Reports

2 Approval of Commission Rates

3 Minimum Commission Rates for overseas facultative reinsurance placements

4 Exclusion of flood from fire policies

5 Implementation of corporate governance and risk management for life, non-life and reinsurers

6 Implementation of solvency framework for life, non-life and reinsurers

7 Indebtedness of insurers and reinsurers

8 Investment In microinsurance and non-bank financial institutions

9 Stress and Scenario Testing

10 Submission of Reinsurance Treaty Programe for 2017

11 Prohibition of unlicensed business as insurance intermediary

Compulsory Fire Insurance EnforcementThe Compulsory Fire Insurance task force undertook several enforcement actions in Accra, Takoradi, Cape Coast, Tamale, Wa and Bolgatanga during the year under consideration. They inspected five hundred and seventy-three (573) commercial buildings to demand evidence of compulsory fire insurance cover.

Out of the 573 buildings inspected 344 of them had procured compulsory fire insurance policies while the remaining 229 had not procured one as required under the Law.

The task force therefore arrested managers of the buildings and threatened to prosecute them if they failed to comply with the directive. They were further requested to report back to the various Police Headquarters with evidence of compliance.

Thereafter, managers of the 229 buildings had duly complied with the directive, with majority of them complying within 48 hours of arrest.

Penalties and Fines As part of efforts to ensure compliance with provisions of the Insurance Act 2006, Act 724 and Guidelines, the Commission levied penalties against four (4) insurance companies.

The breaches involved the placement of facultative reinsurances without approval, violation of market conduct rules in respect of motor insurance, resignation of a Board Chairman without informing the Commission and violation of the No Premium No Cover (NPNC) directive.

Regional OfficesThe NIC continued to oversee the activities of its Regional Offices in Kumasi, Takoradi and Tamale.

The Tamale office is responsible for the Northern sector of the country, Takoradi office serves the Western and Eastern sector of the country whilst the Kumasi office serves the Ashanti and Brong-Ahafo Regions of the country.

During the year under review a new office was opened in Ho to serve the Volta and Eastern Regions of the country.

The three (3) offices continued to carry out their core functions namely; to receive complaints from the public and to resolve the complaints, conduct branch inspections of insurance companies, undertake public education activities and enforcement actions to ensure compliance with compulsory fire insurance law. Where complaints were beyond their capabilities they were referred to the head office in Accra for resolution.

Court CasesIGI Life Assurance Company Limited (IGI Life) and Industrial & General Insurance Company Limited (IGI General)

Following the Fast Track High Court’s Order for the Official Liquidation of the two (2) companies the Official Liquidator proceeded with the sale of the companies’ assets.

The total amount realised from the sale of the assets is as follows;

IGI General - GHS2,300,000.00

IGI Life - GHS362,200.00

The amounts stated above were paid to IGI General and IGI Life claimants on a pro-rata basis as follows:

IGI General - 40% of actual claim

IGI Life - 70% of actual claim

2016 Annual Report National Insurance Commission

16

E & E Platinum Investment vrs SIC Insurance Company Ltd, Ecobank Ghana Limited, National Insurance CommissionThe plaintiff E & E Platinum Investments Limited proceeded to the Commercial Division of the High Court and secured an Order for Garnishee Nissi against Ecobank, GCB Bank and the NIC as custodians of monies held on behalf of SIC Insurance Company.

SIC Insurance Company issued a Credit Guarantee Bond on behalf of T-7 Enterprise in favour of E & E Platinum Investments Limited. T-7 Enterprise defaulted and E&E Platinum called on the bond but SIC failed to honour the claim on suspicion of fraud.

E & E Platinum Investments Limited sued SIC Insurance Company and secured judgement for an amount of Twenty-three thousand Ghana Cedis (GHS23,000.00) and One hundred and ninety-two thousand, eight hundred and seventy-four US dollars (USD192,874) respectively.

At the request of the Lawyers of SIC, the parties involved agreed to withdraw the application for an order for Garnishee proceedings and settled the matter out of Court amicably and the Court granted the request.

CONSUMER COMPLAINTS In 2016, the Commission received 354 complaints from

the public. One hundred and thirty-eight (138) complaints had been resolved as at the end of 2016.

As has been the case in previous years, most of the complaints received related to motor claims. The areas of common complaints from persons pursuing motor claims were as follows:

Repudiation of claim by insurers

Delay in settlement of claims

Dispute over quantum

Delay in payment of settled claims.

The complaints received from life policyholders centered on the following areas:

Benefits promised by insurers differ from benefits on policy documents.

Insurance company’s failure to cease deductions after policy had been surrendered

Payment of low surrender values

Delay in processing matured policies for payment

Delay in returning refund of wrongful deductions

Unauthorized premium deductions

Failure by insurance companies to submit policy documents

TYPE OF COMPLAINTS TOTALSBodily Injury 162

Death 45

Life 94

Own Damage 9

Third Party Property Damage (TPPD) 18

Bonds 8

Marine 1

Others* 17

Total 354 *Others: Employee Grievances and Broker/Agent Commissions

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

17

BodilyInjury45.8%

Death12.7%

Life26.6%

OwnDamage2.5%

TPPD5.1%

Bonds2.3%

Marine0.2%

Others4.8%

TYPEOFCOMPLAINTS(2016)

BodilyInjury Death Life OwnDamage TPPD Bonds Marine Others

Complaints and Settlement Bureau ProcedureCompanies, against whom complaints were made, were informed in writing.

Depending on the nature of the complaint, a company was either requested to react, or invited to meet with the complainant(s) and officers of the National Insurance commission (NIC) in an effort to resolve the complaint.

In some instances the “Bureau” referred cases to the Motor Compensation Fund Committee.

These included complaints from injured motor victims of uninsured vehicles, claims repudiated by insurers on grounds of change of ownership or for other breaches under the Motor Insurance Third Party Insurance Act and Hit and Run cases.

The Bureau received the necessary co-operation from insurers and petitioners during the year under review.

Written commendations were received from petitioners and companies expressing appreciation to the Commission for its mediation efforts.

Distribution of Complaints against Insurance CompaniesOut of the total number of complaints received, 258 were brought against non-life insurance companies, 94 against life insurance companies and two against brokers. Forty-Seven complaints were received in respect of uninsured vehicles.

The tables below reflect the trend of complaints brought against life and non-life insurance companies over the past five years.

CompaniesNumber of Complaints per Year

2012 2013 2014 2015 2016

Non-life insurance companies 165 199 193 217 258

Life insurance companies 67 113 327 222 94

Total 232 222 520 439 352

Others (including uninsured vehicles) 83 68 35 47 2

2016 Annual Report National Insurance Commission

18

Distribution of Complaints by Companies (Non-Life)

CompaniesYear

2012 2013 2014 2015 2016

1 Activa International Insurance Co. Ltd - 1 1 1 -

2 Allianz Insurance Co. Ltd 1 - 1 1 -

3 Best Assurance Company Limited - - - - -

4 Donewell Insurance Co. Ltd 9 21 19 15 16

5 Ecowas Brown Card 3

6 Enterprise Insurance Co. Ltd 2 2 3 8 6

7 Equity Assurance Co. Ltd 14 6 10 11 20

8 Ghana Union Assurance Co. Ltd 2 2 - - 1

9 Glico General Insurance Co. Ltd 2 1 - 1 5

10 Hollard Insurance Co. Ltd - - - - 7

11 Heritage Energy Insurance Co. Ltd (formally IEI) 2 - 3 4 3

12. IGI (Ghana) Insurance Co. Ltd* 11 - - - -

13. Metropolitan Insurance Co. Ltd - 4 3 4 -

14. Millennium Insurance Co. Ltd - - - 1 2

15. NEM Insurance (Ghana) Co. Ltd 1 1 8 15 -

16. NSIA Insurance (Ghana) Co. Ltd 3 2 5 3 2

17. Phoenix Insurance Co. Ltd 2 3 7 4 7

18. Provident Insurance Co. Ltd 10 12 2 13 8

19. Prime Insurance Co. Ltd - 2 - 3 1

20. Priority Insurance Company Limited - - - - -

21. Quality Insurance Co. Ltd 4 9 10 11 16

22. Regency Alliance Insurance Co. Ltd 1 2 2 1 -

23. RegencyNem Insurance Co. Ltd** 17

24. Saham Insurance Ghana Limited 1 2 8 6 2

25. SIC Insurance Co. Ltd 52 70 45 60 59

26. Star Insurance Co. Ltd 16 24 28 25 46

27. Unique Insurance Co. Ltd 20 16 20 15 11

28. Vanguard Assurance Co. Ltd 10 14 16 14 14

29. Wapic Insurance Co. Ltd 2 5 2 1 12

TOTALS 165 199 193 217 258* Under liquidation** merger Regency Insurance and NEM Insurance

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

19

Distribution of Complaints by Companies (Life)

CompaniesYear

2012 2013 2014 2015 20161 Adamas Life Insurance Company - - - - 1

2 A-Plus Assurance Company - - - - 1

3 Capital Express Life Insurance Co. Ltd 1 2 8 4 5

4 Donewell Life Insurance Co. Ltd 2 1 5 3 0

5 Esich Life Insurance Company Ltd - - - 3 8

6 Enterprise Life Assurance Co. Ltd 9 25 31 18 20

7 Prudential Life Insurance Co. Ltd 4 7 84 65 0

8 Ghana Life Insurance Co. Ltd 3 10 3 4 2

9 Glico Life Insurance Co. Ltd 8 18 29 10 2

10 IGI Life Insurance Co. Ltd 1 - - - 0

11 Metropolitan Life Insurance Co. Ltd 10 17 45 19 5

12 Old Mutual Life Insurance Co. Ltd* - - 6 3 13

13 Phoenix Life Insurance Co. Ltd 2 2 11 - 3

14 Provident Life Insurance Co. Ltd 3 2 3 - 0

15 Prudential Life Insurance Co Ltd - - - - 5

16 Quality Life Insurance Co. Ltd 2 2 8 4 3

17 Saham Life Insurance Co. Ltd 5 - 9 4 6

18 SIC Life Insurance Co. Ltd 6 18 42 52 6

19 Star Life Insurance Co. Ltd 6 5 16 12 3

20 Unique Life Insurance Co. Ltd 2 2 10 13 5

21 UT Life Insurance Co. Ltd 1 2 4 3 4

22 Vanguard Life Insurance Co. Ltd 2 - 13 5 2

TOTAL 67 113 327 222 94

*previously Provident Life

Distribution of Complaints by Companies (Brokers)

CompaniesYear

2012 2013 2014 2015 2016

1 Shield Insurance Brokers Limited - - - - 1

2 Tri-Star Insurance Brokers Limited - - - - 1

TOTAL - - - - 2

STATUTORY FUNDSMotor Compensation FundThe Motor Compensation Fund Committee continued with its mandate to achieve the object of the Fund as prescribed under section 192 of the Insurance Act 2006, (Act 724) namely:-

a. To compensate persons who suffer injury or death through a motor accident and who are unable to obtain compensation from an insurance company, and

2016 Annual Report National Insurance Commission

20

b. To promote public education on motor insurance in particular and insurance business in general.

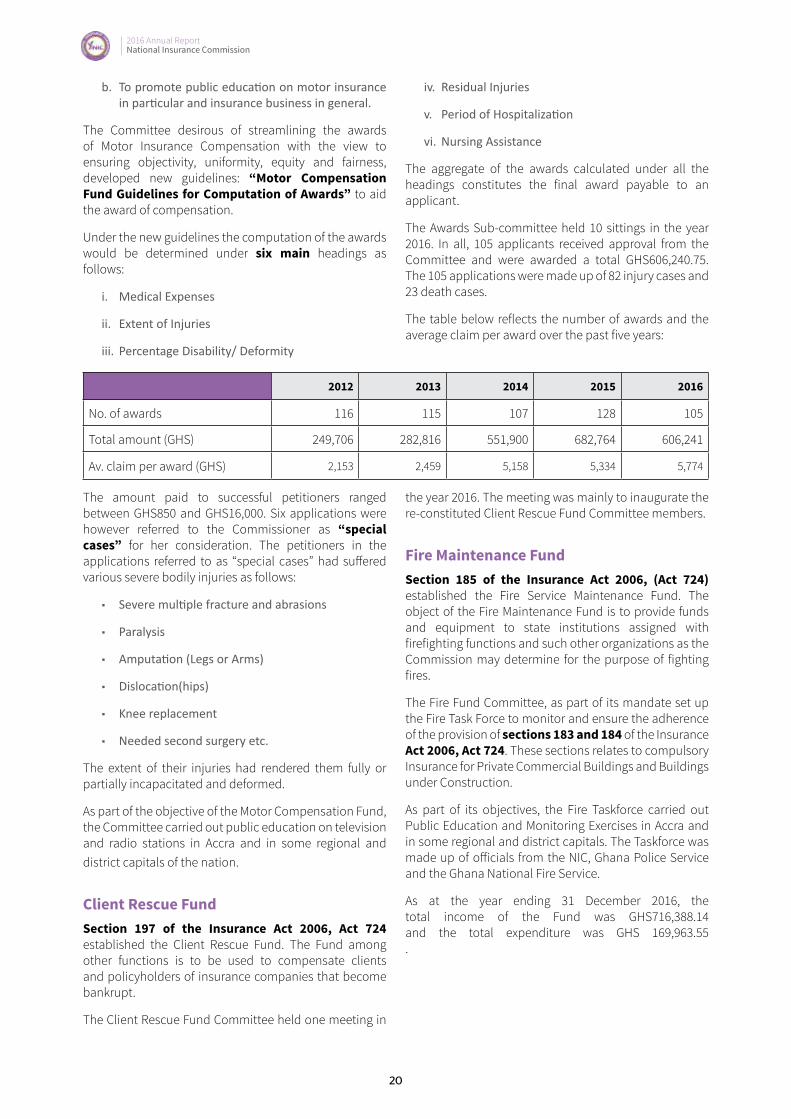

The Committee desirous of streamlining the awards of Motor Insurance Compensation with the view to ensuring objectivity, uniformity, equity and fairness, developed new guidelines: “Motor Compensation Fund Guidelines for Computation of Awards” to aid the award of compensation.

Under the new guidelines the computation of the awards would be determined under six main headings as follows:

i. Medical Expenses

ii. Extent of Injuries

iii. Percentage Disability/ Deformity

iv. Residual Injuries

v. Period of Hospitalization

vi. Nursing Assistance

The aggregate of the awards calculated under all the headings constitutes the final award payable to an applicant.

The Awards Sub-committee held 10 sittings in the year 2016. In all, 105 applicants received approval from the Committee and were awarded a total GHS606,240.75. The 105 applications were made up of 82 injury cases and 23 death cases.

The table below reflects the number of awards and the average claim per award over the past five years:

2012 2013 2014 2015 2016

No. of awards 116 115 107 128 105

Total amount (GHS) 249,706 282,816 551,900 682,764 606,241

Av. claim per award (GHS) 2,153 2,459 5,158 5,334 5,774

The amount paid to successful petitioners ranged between GHS850 and GHS16,000. Six applications were however referred to the Commissioner as “special cases” for her consideration. The petitioners in the applications referred to as “special cases” had suffered various severe bodily injuries as follows:

■ Severe multiple fracture and abrasions

■ Paralysis

■ Amputation (Legs or Arms)

■ Dislocation(hips)

■ Knee replacement

■ Needed second surgery etc.

The extent of their injuries had rendered them fully or partially incapacitated and deformed.

As part of the objective of the Motor Compensation Fund, the Committee carried out public education on television and radio stations in Accra and in some regional and district capitals of the nation.

Client Rescue FundSection 197 of the Insurance Act 2006, Act 724 established the Client Rescue Fund. The Fund among other functions is to be used to compensate clients and policyholders of insurance companies that become bankrupt.

The Client Rescue Fund Committee held one meeting in

the year 2016. The meeting was mainly to inaugurate the re-constituted Client Rescue Fund Committee members.

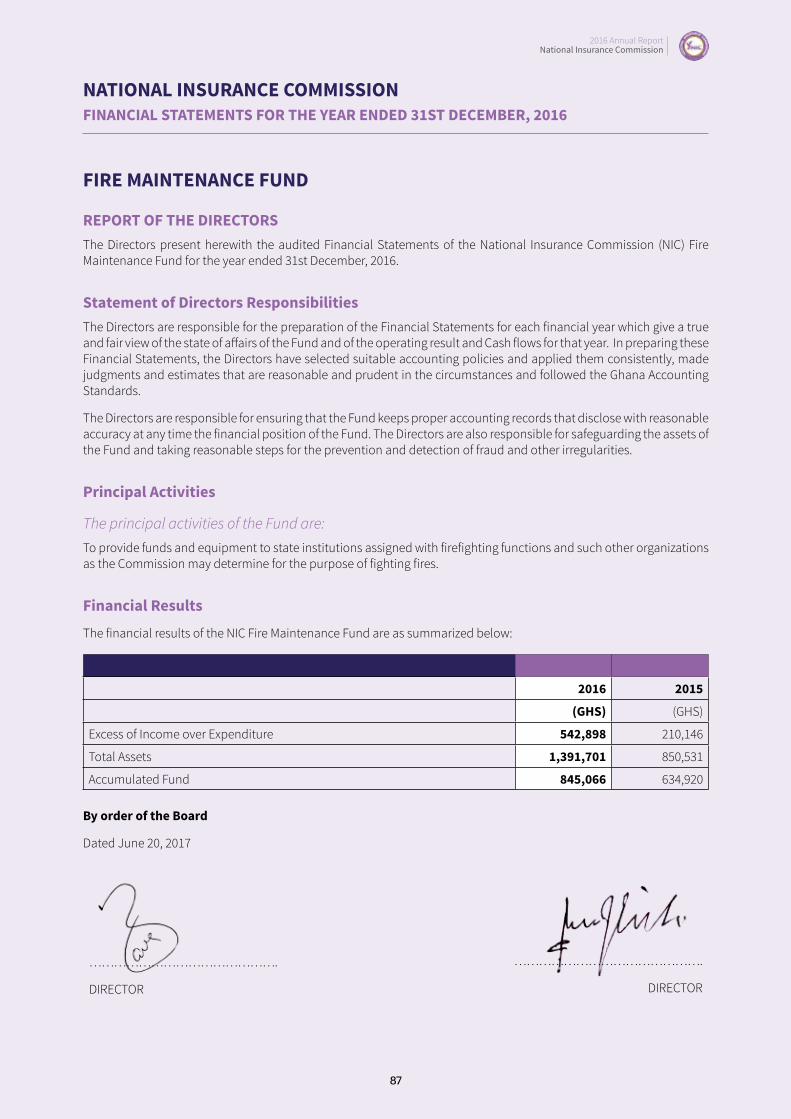

Fire Maintenance FundSection 185 of the Insurance Act 2006, (Act 724) established the Fire Service Maintenance Fund. The object of the Fire Maintenance Fund is to provide funds and equipment to state institutions assigned with firefighting functions and such other organizations as the Commission may determine for the purpose of fighting fires.

The Fire Fund Committee, as part of its mandate set up the Fire Task Force to monitor and ensure the adherence of the provision of sections 183 and 184 of the Insurance Act 2006, Act 724. These sections relates to compulsory Insurance for Private Commercial Buildings and Buildings under Construction.

As part of its objectives, the Fire Taskforce carried out Public Education and Monitoring Exercises in Accra and in some regional and district capitals. The Taskforce was made up of officials from the NIC, Ghana Police Service and the Ghana National Fire Service.

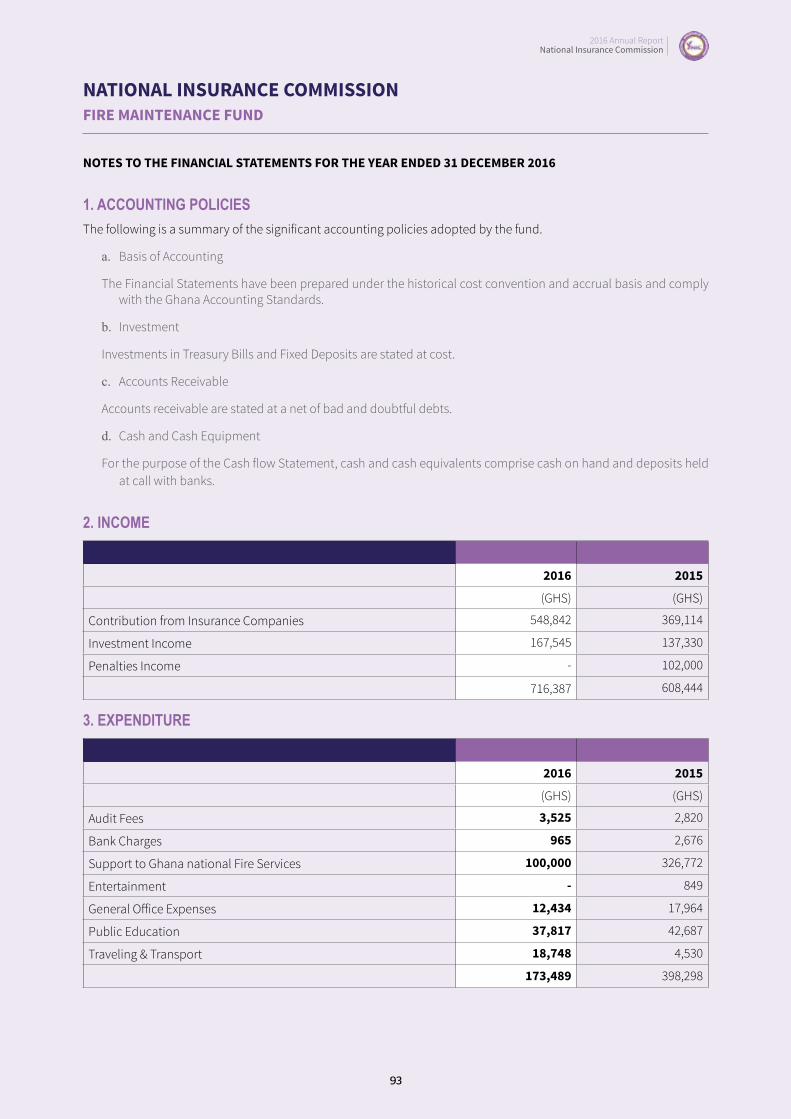

As at the year ending 31 December 2016, the total income of the Fund was GHS716,388.14 and the total expenditure was GHS 169,963.55.

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

21

GHANA INSURANCE MARKET REPORT

ECONOMIC REVIEW

Overview of the EconomyPolitical uncertainty, unstable commodity prices and weak global demand characterised the global economy in 2016. The unexpected vote of the United Kingdom to exit the European Union (‘Brexit’) in June 2016 was a shock to many throughout the world and impacted on the financial markets greatly. Similarly, the expected elections in the US and many other parts of the world created political uncertainty that brought with it turbulence in the economic environment. The global economy therefore recorded a lower growth rate of 3.1% compared to the 3.4% recorded for 2015.

Generally, growth in the advanced economies was subdued, recording an average growth of 1.7% for 2016. The major economic powers in Europe recorded mixed growth in 2016. Germany and Italy recorded positive growth albeit marginally; Britain and France recorded a marginal drop in growth while growth in Spain was maintained. Generally, the euro zone growth dropped from 2.0% in 2015 to 1.7% in 2016. The United States recorded 1.6% growth in 2016 compared to the 2.6% achieved in 2015. The Asia region continue to be the fastest growing region in the world driven by strong domestic demand. Economic growth in South Asia rose by 6.7% in 2016 while the East Asia and Pacific region grew by 6.3% in 2016. Growth in China fell marginally from 6.9% to 6.7%. (Source: World Economic Outlook, April 2017)

Fall in commodity prices adversely affected the economies of Sub-Sahara African leading to revenue shortfalls. Fall in the price of crude oil for example significantly affected Ghana and Nigeria who are major economic brokers in Sub-Sahara Africa. The economy of Nigerian contracted by 1.5%, dropping from 2.7% in 2015.

Crude oil prices were quite low for most of the year. It started the year at $31.9 per barrel but ended the year at $54.9. Gold prices averaged a rise of 7.7% from $1,069.4 in 2015 to $1,151.2 in 2016. Cocoa prices fell from $3,301 in 2015 to $2,268 in 2016. (Source: MOF)

The Ghanaian Economy experienced subdued growth as a result of various challenges in 2016. While

low oil revenues led to revenue shortfalls, utility tariffs hike, transport cost and rising interest rate impacted heavily on inflation. The never ending power sector crisis and poor domestic demand coupled with the introduction of numerous taxes adversely affected disposable income especially as we got closer to the general elections in December.

Overall real GDP recorded a drop from the growth of 3.9% in 2015, achieving a growth of 3.5% against a target of 4.1%. Non-oil GDP achieved a growth of 4.6%. The 2016 GDP growth of 3.6% was mostly aided by the growth in the services sector of 5.9% and the Agriculture sector: 3.6%. (Source: MOF)

The year ended with a budget deficit of 7.8% of GDP with the debt stock rising marginally from 72.2% of GDP in 2015 to 72.5% of GDP at the end of 2016.

InflationHeadline inflation rose sharply from 17.7% in December 2015 to 19.0% in January 2016 and reached a high of 19.2% by March 2016. This was due mainly to upward adjustment in ex-pump prices of petroleum products and the utility tariff hikes introduced in the last quarter of 2015. Inflation however declined steadily to 15.4% by the end of the year. This was aided by the IMF extended credit facility programme which was aimed at restoring fiscal discipline and macroeconomic stability.

Interest RateThe Monetary Policy Committee of the Bank of Ghana maintained the Monetary Policy Rate at 26% for much of the year but eventually reduced it by 50 basis points to 25.5% in November, 2016. Short-term securities however, declined significantly during the course of the year with the benchmark 91-Day Treasury bill ending the year at 16.4% from 23.1% at the beginning of the year. The 182-Day Treasury bill also declined from 24.4% to 17.6%. The longer term securities such as the 1-Year and 2-Year Treasury notes on the other hand declined very marginally from 22.8% to 21.5% and 23.3% to 22.5% respectively.

2016 Annual Report National Insurance Commission

22

Exchange RateThe Ghana cedi did much better in 2016 than the previous year, depreciating by 9.6% against the US dollar as compared to 31.2% recorded in 2015. The US dollar ending the year at GHS4.2/USD. For the Euro the depreciated was 5.3% ending the year at GHS4.4/Euro while the Pound Sterling appreciated by as much as 10% ending the year at GHS5.2/GBP.

Developments on the Ghana Stock Market 2016 was a challenging year for the Ghana Stock Exchange as the high returns on short term securities was more attractive to most investors. The difficult economic environment characterized by poor industry performance and coupled with the tough tax regime all impacted negatively on most listed companies. The Composite Index (GSE-CI) declined during the year by 15.33% in 2016 compared with a loss of 11.7% in 2015. About 23 stocks recorded losses with only 6 gainers for the year. Market capitalisation also declined by 7.7% to GHS 52,910 at the

end of 2016 from GHS 57,116.8 million in 2015.

GHANA INSURANCE MARKET REPORT

Assets and Liabilities (excluding Reinsurance)Aggregate insurance industry assets stood at GHS 3.76bn as at the end of 2016, representing a growth of 23% from GHS 3.06bn in the prior year. Life’s contribution to total industry assets was GHS 2.25bn representing 60% as against Non-life’s contribution of GHS 1.51bn representing 40%.

Total assets mainly consist of Investments, Cash and Property, Plant and Equipment (PPE). Figures 1 (b) and (c) show that investments form the largest portion of total assets. It makes up about 87% of the assets of long-term insurers (Life) and 59% of the assets of the short-term insurers (Non-life).

Total Technical provision by the end of the year 2016, stood at GHS 1.98bn representing a growth of 14% from GHS 1.73bn in 2015. The figures below show pictorial analyses of Total Assets between Life and Non-life for the years under review.

Fig. 1(a)

0

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

2016 2015 2014

2,24

1,04

1,44

6

1,74

4,17

1,94

3

1,38

3,42

7,95

8

1,50

5,67

6,46

3

1,32

0,37

0,21

2

886,65

9,34

6

TotalAssets:YearlyAggregateIndustryContribution

Life Non-life

Source: Financial returns from regulated entities

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

23

Fig. 1(b) Composition of Total Life Industry Assets

87%

5%4%4%

Annual,2016

Investments Cash

Other Assets PPEor FixedAssets

83%

6% 6% 4%

Annual,2015

Investments Cash

OtherAssets PPEorFixedAssets

81%

7% 8% 5%

Annual,2014

Investments CashOtherAssets PPEorFixedAssets

Fig 1(c) Composition of Total Non-Life Industry Assets

59%

7%

24%

10%

Annual,2016

Investments Cash OtherAssets PPE

47%

10%

34%

9%

Annual,2015

Investments Cash OtherAssets PPE

2016 Annual Report National Insurance Commission

24

62% 11%

18%

9%

Annual,2014

Investments Cash OtherAssets PPE

Source: Based on data submitted to the NIC by licensed companies.

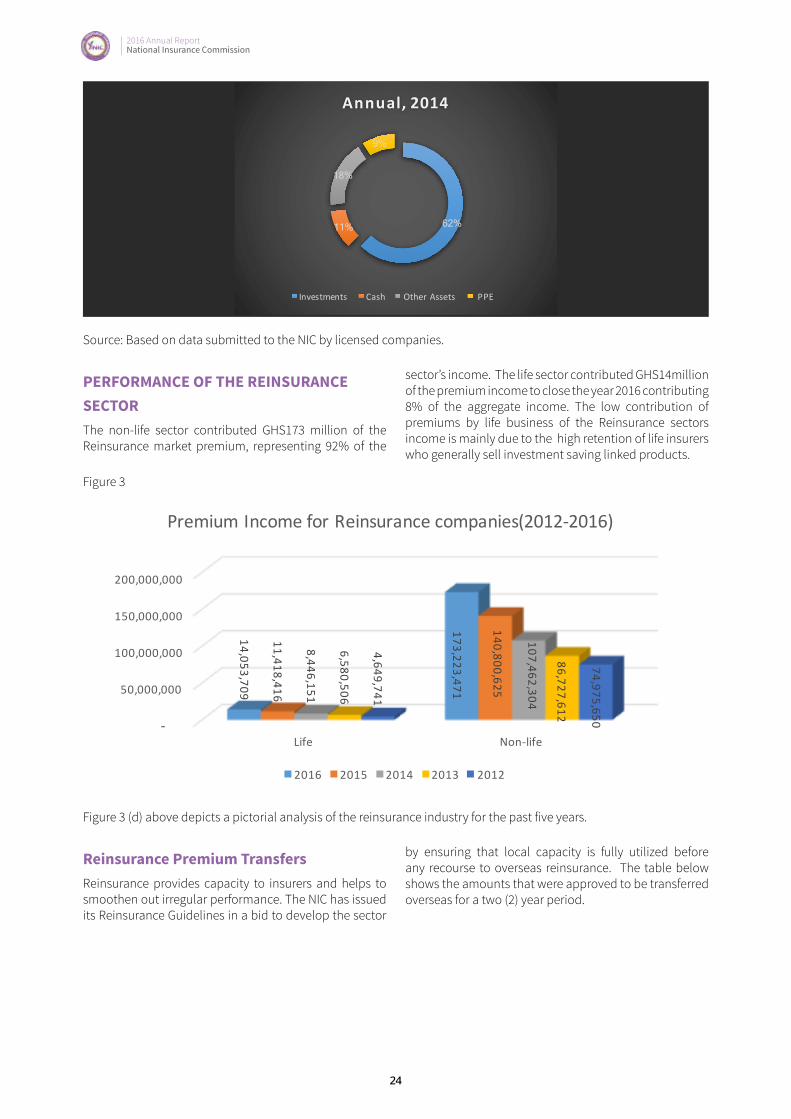

PERFORMANCE OF THE REINSURANCE SECTORThe non-life sector contributed GHS173 million of the Reinsurance market premium, representing 92% of the

sector’s income. The life sector contributed GHS14million of the premium income to close the year 2016 contributing 8% of the aggregate income. The low contribution of premiums by life business of the Reinsurance sectors income is mainly due to the high retention of life insurers who generally sell investment saving linked products.

Figure 3

-

50,000,000

100,000,000

150,000,000

200,000,000

Life Non-life

14,053,709

173,223,471

11,418,416

140,800,625

8,446,151

107,462,304

6,580,506

86,727,612

4,649,741

74,975,650

PremiumIncomeforReinsurancecompanies(2012-2016)

2016 2015 2014 2013 2012

Figure 3 (d) above depicts a pictorial analysis of the reinsurance industry for the past five years.

Reinsurance Premium TransfersReinsurance provides capacity to insurers and helps to smoothen out irregular performance. The NIC has issued its Reinsurance Guidelines in a bid to develop the sector

by ensuring that local capacity is fully utilized before any recourse to overseas reinsurance. The table below shows the amounts that were approved to be transferred overseas for a two (2) year period.

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

25

Overseas Reinsurance Premium Transfers

Currency 2016 2015

Dollars (US$) 9.72m 4.45m

Pounds Sterling (£) 862 4,568

Euros (€) 36,052 427,337

Ghana Cedis (GHS) 4.68m 18.1m

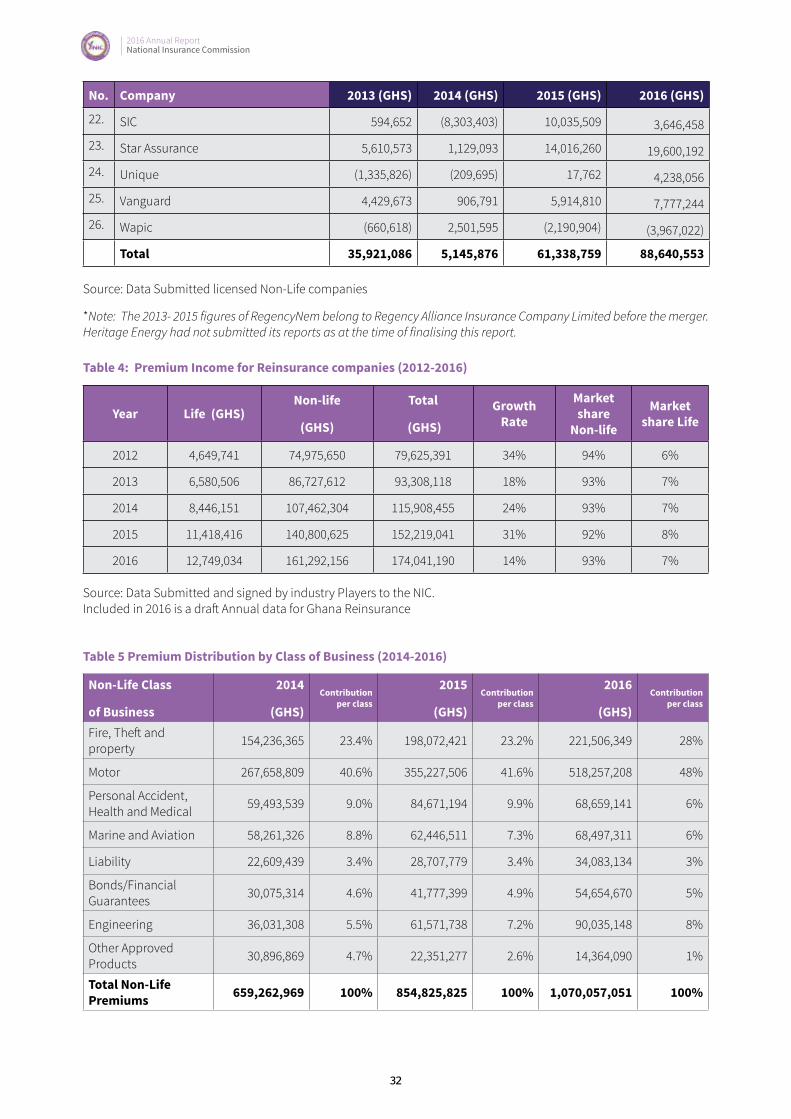

PREMIUM BY CLASS OF BUSINESS NON-LIFEThe motor class of business continued its dominance with a premium income of GHS 518m, contributing 48% of the overall premium income for 2016. It grew by 46% over the 2015 premium of GHS355m. Fire, Theft and Property contributed 21% of the total premium for 2016 and grew by 12% compared to the 2015 results. Marine & Aviation, and Personal Accident & Medical both came

third with an overall contribution of 6% of the total premium of GHS1.07bn in 2016. Engineering contributed a gross market premium of GHS90m and a market share of 8%.

Expectations for Marine to grow remain high due to the on-going enforcement of section 37 of Insurance Act, 2006 (Act 724). Importers are obliged to insure their goods locally for the industry to reap the benefits of an increase in premium income. Refer to Table 5 below for premiums per class of business.

Fig 4: Analysis of Non-Life Premiums by Class of Business

21%

48% 6%

6% 3%

5%8%

1%

2016:NonLifeClass ofbusiness

F,T&P Motor P,H&M M&A Liability FinancialLoss Engineering Others

Note:F, T & P - Fire, Theft and PropertyP, H &M - Personal Accident, Health and MedicalM & A - Marine and AviationFinancial Guarantee: Bonds

2016 Annual Report National Insurance Commission

26

INSURANCE BROKING MARKETIn 2016, brokers received revenue amounting to GHS 72.5m representing a growth rate of 12%. As shown in Table 6 below, 64% of the total commission income was contributed by the top ten (10) brokers which stood at GHS 45.1m.

With a contribution of GHS 15m and GHS 6m representing 33% and 13%, KEK Insurance and Edward Mensah, Wood & Associates Limited maintained their respective positions as 1st and 2nd in the sector. Gras Savoye (now Willis Towers Watson Ghana limited), Safety, Shield and Crown improved to 3rd, 5th, 8th and 9th positions

respectively. However, KEK Reinsurance and Horizon declined to the 4th and 7th positions respectively. Midas Insurance made it to the 10th position with income in excess of GHS 2m representing 5% of the market share for 2016. Tri-Star and Crown Insurance Brokers Limited both maintained their respective 6th and 9th positions in 2016 as in prior year. This analysis does not include figures from the 10 newly licensed brokers because they are start-ups and were inactive during the year.

Below is the list of top ten brokers based on their market share /commission income:

NAME OF BROKER COMMISSION INCOME

1 KEK Insurance Brokers Limited 14,921,591

2 Edward Mensah, Wood & Associates Limited 6,031,736

3 Gras Savoye Ghana Limited (now Willis Watson Towers Gh.) 5,230,618

4 KEK Reinsurance Brokers (Africa) Limited 3,678,527

5 Safety Insurance Brokers Limited 3,019,912

6 Tri-star Insurance Services Limited 2,766,881

7 Horizon Insurance Brokers Limited 2,748,823

8 Shield Insurance & Risk Management Company Limited 2,597,133

9 Crown Insurance Brokers Limited 2,089,394

10 Midas Insurance Brokers Ltd 2,054,216

Total (GHS) 45,138,831

Fig. 4 Analysis of Brokerage Commission

2835

48

67

7135

26

3639

11

0

5

10

15

20

25

30

35

40

45

0

10

20

30

40

50

60

70

80

2012 2013 2014 2015 2016

Reve

nues(inGHSmillion)

Brokeragegrowthoverfiveyears(2012-2016)

Source: Data submitted by licensed Brokers

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

27

Figure 4 above shows a pictorial analysis of the growth of brokerage income over the past five years. As indicated, the rate of growth has been fluctuating. From 35% in 2012, the growth rate fell sharply to 26% in 2013. It then increased substantially in 2014 and 2015 partly due to the upward review in motor tariffs and then plummeted to 11% in 2016.

Table 1 Products Approved in 2016

No. COMPANY PRODUCT

1 African Life Insurance Company Limited Care Education Plan

2 African Life Insurance Company Limited Care Funeral Plan

3 African Life Insurance Company Limited Care Protection/Credit Life Plan

4 African Life Insurance Company Limited Care Term Life (Keyman) Plan

5 African Life Insurance Company Limited Care Group Term Life Plan

6 Best Assurance Company Limited Foreign Travel Insurance

7 Enterprise Life Assurance Company Limited Educare

8 Enterprise Life Assurance Company Limited Life Time Needs Plus

9 Enterprise Life Assurance Company Limited Elac Living Plus Plan

10 Enterprise Life Assurance Company Limited Elac Executive Plus plan

11 Enterprise Life Assurance Company Limited Transitions

12 Esich Life Insurance Company Limited Asomdwe Policy

13 First Insurance Company Limited Annuity (Immediate and Deferred)

14 Glico Life Insurance Company Limited Annuity (Immediate and Deferred)

15 GN Life Insurance Company Limited Group Term Policy

16 Hollard Insurance (Gh) Limited Lost Card Protection Policy

17 Metropolitan Life Insurance (Ghana) Limited Revised Investment Product (Goal Achiever Plan)

18 Old Mutual Life Assurance Company Limited Ecobank Retirement Savings Plan

19 Old Mutual Life Assurance Company Limited Transition Product

20 Prudential Life Insurance Ghana Limited PRU Smarter Life Plan/(Prudent Life Plan)

21 Prudential Life Insurance Ghana Limited SGBank Classic Funeral plan

22 Prudential Life Insurance Ghana Limited Changes Made to Tigo Family and hospital support plans

23 Prudential Life Insurance Ghana Limited BIMA PEG Hospital Cash

24 Prudential Life Insurance Ghana Limited BIMA Family Health Plan

25 Prudential Life Insurance Ghana Limited Tigo Income Protection Plan

26 Prudential Life Insurance Ghana Limited Petra trust Savings Insurance/ Savings Dream Guide

27 Saham Insurance Ghana Limited Directors & Officers Liability Protect

28 Saham Insurance Ghana Limited Home & Household Protect

29 Saham Insurance Ghana Limited Office Protect

30 Saham Insurance Ghana Limitedl Motor Protect

31 UT Life Insurance Company Limited Educational Plan

32 UT Life Insurance Company Limited Funeral Plan

33 UT Life Insurance Company Limited Update of UT Group Life Plan

Source: Data from Actuarial Department of the NIC.

2016 Annual Report National Insurance Commission

28

Table 2(a) Growth in Industry Gross Premium (2012 - 2016)

Year Premium Income (GHS) Growth Rate %

2012 850,679,973 -

2013 1,052,090,981 24

2014 1,239,853,442 18

2015 1,560,679,185 262016 1,928,838,573 24

Table 2(b) Growth in Gross premium for Non-Life Insurance (2012 -- 2016)

Year Premium Income (GHS) Growth Rate %

2012 494,891,864 -

2013 582,456,306 18

2014 659,262,969 13

2015 854,825,825 30

2016 1,070,057,051 25

Table 2(c) Growth in Gross Premium for Life Insurance (2012-2016)

Year Premium Income (GHS) Growth Rate %

2012 355,788,109 -

2013 469,634,675 32

2014 580,590,473 23

2015 705,853,360 22

2016 858,781,522 22

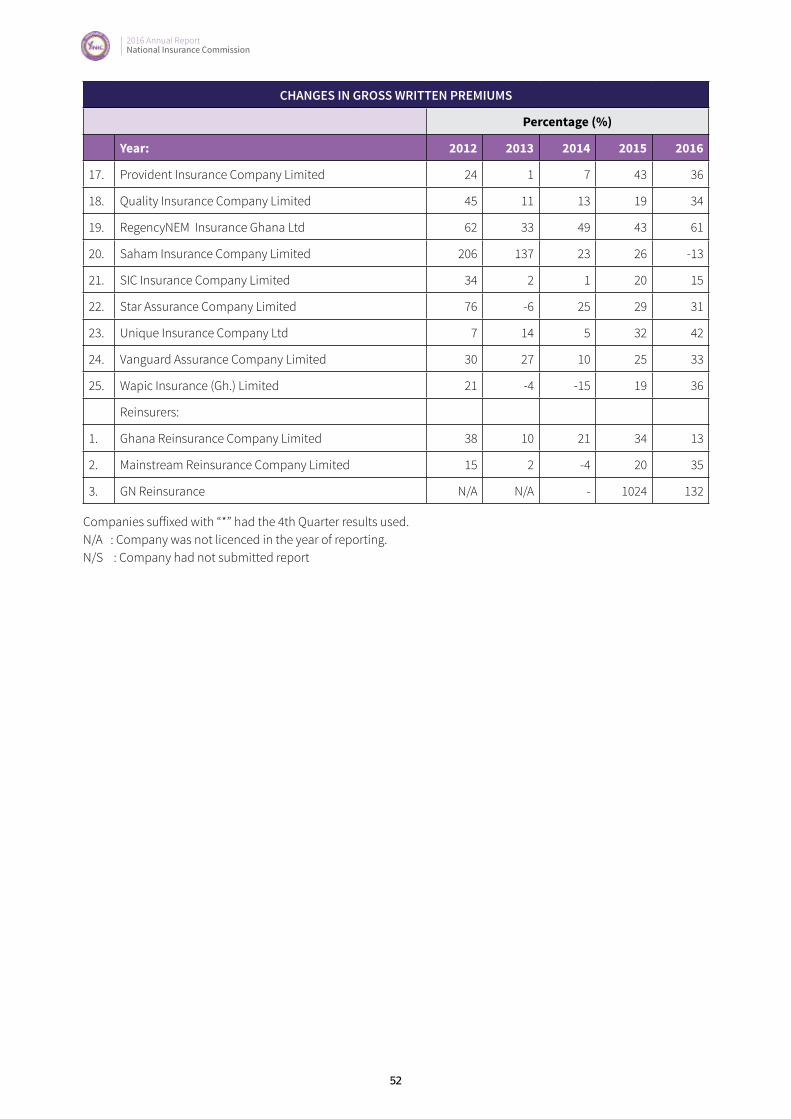

Table 2 (d) GROSS PREMIUMS OF NON-LIFE COMPANIES (2012 - 2016)

No COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

1. Activa Int. 16,066,559 21,720,151 26,900,589 38,268,180 40,818,428

2. Allianz Ins. 14,222,126 16,666,082 26,624,368 21,858,529 27,183,279

3. Best Ass. NA NA NA NA 4,918,453

4. Donewell Ins. 12,545,982 14,570,013 14,970,003 20,357,071 30,530,398

5. Enterprise Ins. 43,178,409 61,330,000 70,398,623 100,996,493 135,446,537

6. Equity Ass. 10,792,727 12,608,637 15,696,407 21,294,662 31,468,150

7. Ghana Union* 14,519,988 21,856,982 22,348,675 31,536, 467 33,526,207

8. Glico Gen. 31,905,202 39,691,703 46,397,194 68,638,428 69,660,874

9 Imperial Gen. NA 966,772 5,571,696 6,508,200 9,239,314

10 Heritage Energy 7,814,808 8,196,429 6,132,835 6,721,760 N/S

11. Hollard Ins. 44,405,519 53,899,625 63,307,559 77,273,501 84,094,685

12 Millennium Ins. 4,122,644 7,259,603 6,637,176 8,161,485 12,930,952

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

29

No COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

13 NSIA Ghana 7,234,632 8,157,332 5,428,571 7,948,287 10,998,238

14 Phoenix Ins. 20,908,895 24,296,304 25,178,385 34,770,287 46,278,553

15 Prime Ins. 575,000 2,163,114 5,306,379 12,158,093 29,389,566

16 Priority Ins. 27,888 2,135,922 2,597,458 3,872,158 8,940,836

17 Provident Ins. 9,842,235 9,793,754 10,462,289 14,952,407 20,364,746

18 Quality Ins. 15,520,067 17,170,940 19,356,125 23,090,012 30,946,446

19 RegencyNEM 6,323,879 8,382,758 12,476,495 17,807,025 28,733,674

20 Saham Ins. 4,940,299 8,308,085 10,221,468 12,913,133 11,207,580

21 SIC Ins. 109,965,628 111,897,149 113,069,892 138,984,920 160,111,229

22 Star Assurance 60,895,352 57,005,894 71,228,815 91,584,258 119,710,991

23 Unique Ins. 5,020,265 5,726,279 5,983,230 7,856,036 11,167,973

24 Vanguard Ass. 41,776,384 53,039,656 58,172,319 72,775,120 97,100,246

25 Wapic 8,536,786 9,409,454 8,013,773 11,211,667 15,289,696

TOTALS 494,891,864 582,456,306 659,262,969 854,825,825 1,070,057,051

Source: Data Submitted and signed by industry Players to the NIC

Note: ‘NA’ companies were either not licensed or yet to provide operational result ‘*’ means 4th Quarter data was used due to late submission of audited annual data N/S - Heritage Energy had not submitted its reports at the time this report was finalised.

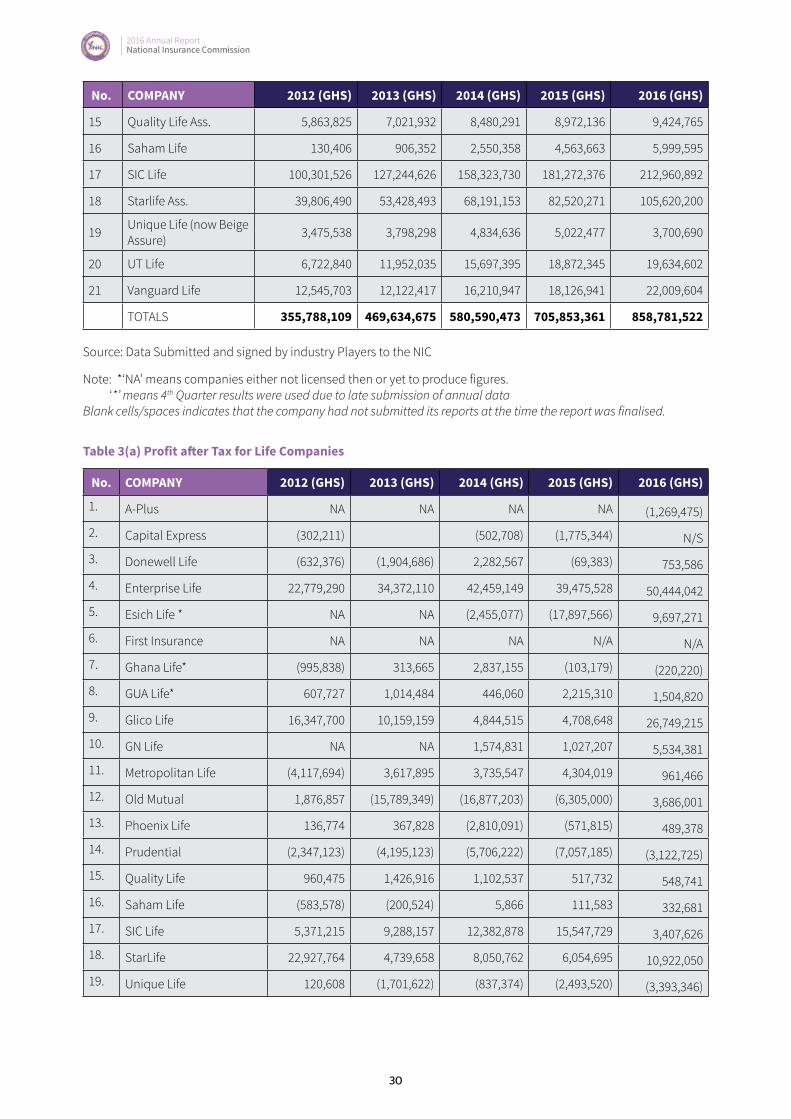

Table 2(e) GROSS PREMIUM OF LIFE COMPANIES (2012 – 2016)

No. COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

1 A-Plus NA NA NA NA 56,742

2 Capital Express (Now Aviance Life) 812,057 809,346 580,154 477,366

3 Donewell Life 7,186,954 8,118,905 8,241,894 7,705,518 7,134,666

4 Enterprise Life 89,118,307 123,846,285 156,244,014 200,438,627 235,311,893

5 Esich Life* NA NA 1,663,326 8,200,464 12,375,460

6 First Insurance Comp. NA NA NA NA

7 Ghana Life Ins*. 8,278,234 10,533,661 12,731,893 14,740,234 17,911,223

8 Ghana Union Life* 2,498,486 4,724,564 5,014,211 7,395,373 7,636,506

9 Glico Life Ins. 36,022,000 55,546,000 59,654.05 64,926,000 82,733,226

10 GN Life Ass. NA NA NA 1,179,090 7,270,045

11 Metropolitan Life 19,642,000 21,574,030 26,344,298 29,924,473 31,595,032

12 Old Mutual Ass. 15,760,743 15,458,278 16,477,834 22,765,849 33,425,000

13 Phoenix Life Ins. 5,841,693 7,121,098 7,627,824 8,029,873 10,224,115

14 Prudential Life Ins. 1,781,307 5,378,355 11,722,469 20,720,285 33,814,009

2016 Annual Report National Insurance Commission

30

No. COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

15 Quality Life Ass. 5,863,825 7,021,932 8,480,291 8,972,136 9,424,765

16 Saham Life 130,406 906,352 2,550,358 4,563,663 5,999,595

17 SIC Life 100,301,526 127,244,626 158,323,730 181,272,376 212,960,892

18 Starlife Ass. 39,806,490 53,428,493 68,191,153 82,520,271 105,620,200

19 Unique Life (now Beige Assure) 3,475,538 3,798,298 4,834,636 5,022,477 3,700,690

20 UT Life 6,722,840 11,952,035 15,697,395 18,872,345 19,634,602

21 Vanguard Life 12,545,703 12,122,417 16,210,947 18,126,941 22,009,604

TOTALS 355,788,109 469,634,675 580,590,473 705,853,361 858,781,522 Source: Data Submitted and signed by industry Players to the NIC

Note: *‘NA’ means companies either not licensed then or yet to produce figures. ‘*’ means 4th Quarter results were used due to late submission of annual dataBlank cells/spaces indicates that the company had not submitted its reports at the time the report was finalised.

Table 3(a) Profit after Tax for Life Companies

No. COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

1. A-Plus NA NA NA NA (1,269,475)

2. Capital Express (302,211) (502,708) (1,775,344) N/S

3. Donewell Life (632,376) (1,904,686) 2,282,567 (69,383) 753,586

4. Enterprise Life 22,779,290 34,372,110 42,459,149 39,475,528 50,444,042

5. Esich Life * NA NA (2,455,077) (17,897,566) 9,697,271

6. First Insurance NA NA NA N/A N/A

7. Ghana Life* (995,838) 313,665 2,837,155 (103,179) (220,220)

8. GUA Life* 607,727 1,014,484 446,060 2,215,310 1,504,820

9. Glico Life 16,347,700 10,159,159 4,844,515 4,708,648 26,749,215

10. GN Life NA NA 1,574,831 1,027,207 5,534,381

11. Metropolitan Life (4,117,694) 3,617,895 3,735,547 4,304,019 961,466

12. Old Mutual 1,876,857 (15,789,349) (16,877,203) (6,305,000) 3,686,001

13. Phoenix Life 136,774 367,828 (2,810,091) (571,815) 489,378

14. Prudential (2,347,123) (4,195,123) (5,706,222) (7,057,185) (3,122,725)

15. Quality Life 960,475 1,426,916 1,102,537 517,732 548,741

16. Saham Life (583,578) (200,524) 5,866 111,583 332,681

17. SIC Life 5,371,215 9,288,157 12,382,878 15,547,729 3,407,626

18. StarLife 22,927,764 4,739,658 8,050,762 6,054,695 10,922,050

19. Unique Life 120,608 (1,701,622) (837,374) (2,493,520) (3,393,346)

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

31

No. COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

20.

21.UT Life 403,975 2,008,795 786,428 (3,980,163) (10,431,350)

22. Vanguard Life (662,411) 211,151 (466,020) (2,800,994) 373,524

Total By Year 61,891,154 43,728,514 50,853,600 30,908,304 98,237,141

Table 3(a) Profit After Tax for Life Companies

Source: Data Submitted by licensed Life companies

Note: N/A – A Plus Esich and First Insurance had not been licensed. N/S – Capital Express had not submitted their reports at the time of finalising this report‘*’ means 4th Quarter results were used due to late submission of annual data

Table 3(b) Profit After Tax for Non-Life Companies

No. Company 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

1. Activa 1,885,345 781,634 2,575,779 2,582,380

2. Allianz (469,397) (788,624) (2,512,678) (1,592,056)

3. Best Assurance NA NA N/A 439,553

4. Donewell 1,561,159 3,235,787 3,454,261 5,071,865

5. Enterprise 13,522,000 8,314,907 9,238,477 17,023,497

6. Equity 1,425,393 1,263,176 2,177,456 4,177,606

7. GUA* 1,024,264 1,221,690 3,388,629 913,913

8. Glico General 812,653 (3,489,527) (1,492,335) 3,813,043

9. Hollard 2,823,074 1,560,741 4,428,310 8,124,290

10. Imperial Gen. 220,543 228,339 122,011 (1,254,015)

11. IEI / Heritage (5,390,403) (3,281,638) 249,233 N/S

12. Millennium 1,621,823 601,201 (155,221) 1,828,426

13. NEM 261,515 329,888 542,667 N/A

14. NSIA (2,816,023) (3,623,029) 602,653 1,202,744

15. Phoenix (91,960) 2,011,860 1,701,742 5,752,775

16. Prime (1,204,301) (6,135,082) (889,655) 745,706

17. Priority 881,056 1,317,602 2,680,385 1,628,931

18. Provident 9,119,943 3,174,096 5,839,491 5,514,311

19. Quality 1,137,964 140,242 650,405 2,937,363

20. RegencyNem 784,781 2,135,023 529,167 2,725,976

21. Saham 173,203 123,209 414,546 (4,290,683)

2016 Annual Report National Insurance Commission

32

No. Company 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

22. SIC 594,652 (8,303,403) 10,035,509 3,646,458

23. Star Assurance 5,610,573 1,129,093 14,016,260 19,600,192

24. Unique (1,335,826) (209,695) 17,762 4,238,056

25. Vanguard 4,429,673 906,791 5,914,810 7,777,244

26. Wapic (660,618) 2,501,595 (2,190,904) (3,967,022)

Total 35,921,086 5,145,876 61,338,759 88,640,553 Source: Data Submitted licensed Non-Life companies

*Note: The 2013- 2015 figures of RegencyNem belong to Regency Alliance Insurance Company Limited before the merger. Heritage Energy had not submitted its reports as at the time of finalising this report.

Table 4: Premium Income for Reinsurance companies (2012-2016)

Year Life (GHS)Non-life

(GHS)

Total

(GHS)Growth

Rate

Market share

Non-life

Market share Life

2012 4,649,741 74,975,650 79,625,391 34% 94% 6%

2013 6,580,506 86,727,612 93,308,118 18% 93% 7%

2014 8,446,151 107,462,304 115,908,455 24% 93% 7%

2015 11,418,416 140,800,625 152,219,041 31% 92% 8%

2016 12,749,034 161,292,156 174,041,190 14% 93% 7%

Source: Data Submitted and signed by industry Players to the NIC.Included in 2016 is a draft Annual data for Ghana Reinsurance

Table 5 Premium Distribution by Class of Business (2014-2016)

Non-Life Class

of Business

2014

(GHS) Contribution

per class

2015

(GHS)Contribution

per class

2016

(GHS)Contribution

per class

Fire, Theft and property 154,236,365 23.4% 198,072,421 23.2% 221,506,349 28%

Motor 267,658,809 40.6% 355,227,506 41.6% 518,257,208 48%

Personal Accident, Health and Medical 59,493,539 9.0% 84,671,194 9.9% 68,659,141 6%

Marine and Aviation 58,261,326 8.8% 62,446,511 7.3% 68,497,311 6%

Liability 22,609,439 3.4% 28,707,779 3.4% 34,083,134 3%

Bonds/Financial Guarantees 30,075,314 4.6% 41,777,399 4.9% 54,654,670 5%

Engineering 36,031,308 5.5% 61,571,738 7.2% 90,035,148 8%

Other Approved Products 30,896,869 4.7% 22,351,277 2.6% 14,364,090 1%

Total Non-Life Premiums 659,262,969 100% 854,825,825 100% 1,070,057,051 100%

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

33

LIFE AND NON-LIFE 2014 Market share 2015 Market

Share 2016

Total Non-Life Premiums 659,262,969 53% 854,825,825 55%

1,070,057,051 55%

Life Business (All the classes) 580,590,473 47% 705,853,361 45%

858,781,522 45%

Grand Total (Life and Non-Life) 1,239,855,456 100% 1,560,681,201 100% 1,928,838,573 100%

Source: Data Submitted and signed by industry Players to the NIC

*The Non-Life product lines have been realigned, thus separating Bonds/Financial Guarantees, Engineering and Liability from Personal Accident line of business.

Table 6: Brokerage Commission for 2012 – 2016 expressed in Cedis

No. COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

1. AG & Assoc. 48,850 146,423 220,709 326,800 N/S

2. Akoto Risk 458,838 542,781 630,740 960,550 1,203,754

3. All Risks 742,283 689,827 721,166 763,677 879,618

4. AllStar - 415,953 538,093

5. Allied 59,645 52,343 134,279 75,579 110,051

6. Alpha 352,147 352,147 474,200 554,134 701,662

7. Apex 78,316 64,457 318,336 374,483 628,716

8. ARB 264,395 494,090 800,266

9. ARK 118,399 162,741 254,695 311,321 347,425

10. Arrowclass 774,653 999,791 1,324,991

11. Ascoma Ghana 416,587 679,537 1,225,130 1,134,591 1,401,987

12. Asterix 108,911 131,319 192,507 129,207 197,194

13. Baobab 9,682 36,185 103,687 188,203

14. Boaitey & Associates - 264,810 542,177

15. Byllwych - 3,694 N/S

16. Cardinal Brokers * - 193,340 363,280 273,582

17. Ceris Int’l 251,312 325,020 801,849 577,793 N/S

18. CLAIM Ltd. 354,390 242,468 511,109 483,781 340,547

19. Corporate Trust 162,367 542,789 249,279 982,734 N/S

20. Crown 1,016,883 1,165,184 1,611,389 1,874,542 2,089,394

21. Danniads 837,503 981,531 1,367,910 1,369,603 1,458,624

22. Dezag Insurance Brokers Limited 48,958 171,380 190,253

23. Double D & M 15,561 20,907 - 62,906 N/S

2016 Annual Report National Insurance Commission

34

No. COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

24. Dynamic 281,379 270,994 402,873 461,250 444,832

25. Edward Mensah, Wood & Associates. 3,472,549 3,718,846 4,060,201 6,596,403 6,031,736

26. Eureka 51,289 84,015 - N/S

27. Felin Brokers 147,350 427,251 592,832 905,780

28. First Anchor 588,822 638,421 1,195,548 1,478,209 1,424,594

29. Functions Risk 27,657 144,511 202,619

30. GBL Insurance Brokers Ltd. 3,694 23,270

31. Ghana Int’l Brokers 41,105 118,096 N/A N/A N/S

32. Global Impact 96,336 91,763 125,550 113,395 129,673

33. Goldlink 40,140 46,708 95,300

34. Goodwill - 2,704 73,442

35. Gras Savoye 1,618,102 2,091,824 2,229,774 3,232,346 5,230,618

36. Horizon 1,046,989 1,544,717 2,143,062 2,721,601 2,749,823

37. Insurance Centre 102,167 124,892 189,745 280,919 376,241

38. Insurance Consult. 380,056 232,232 204,661 193,349 295,054

39. Insurance Solutions 252,466 385,187 723,412 1,053,551 1,466,311

40. KAV 60,261 130,216 114,770 98,677 224,683

41. KEK 6,812,012 8.272,563 10,909,117 13,265,860 14,921,591

42. KEK Reins. 1,020,834 1,450,312 2,507,054 3,293,701 3,678,527

43. Khols & Hols 23,301 272,412

44. Liberty Brokers 78,117 171,056 191,365 277,784 229,930

45. Lordship 272,579 327,665 470,040 531,091 669,372

46. M & G Ins. Brok. 436,770 478,626 758,816 928,308 1,090,259

47. Maxpal Interm. 162,498 152,932 63,166 83,574 143,009

48. Metrix 90,330 218,222 328,624

49. Midas 664,353 1,034,889 1,474,030 1,802,416 2,054,216

50. Multinational 65,266 211,036 362,427

51. NDL Consult 69,400 206,702 230,157 232,442

52. Novelty - 144,950 152,198

53. OAK Brokers - 40,161 -

54. Premier Brokers 14,715 31,697 129,152 137,180 230, 211

55. Progressive 507,379 881,760 924,358 1,126,622 1,418,800

56. Prudent Ins. Brokers 301,714 320,226 324,768 270,249 302,425

57. Riscovery Ltd. 40,108 181,171 682,218 722,401 840,990

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

35

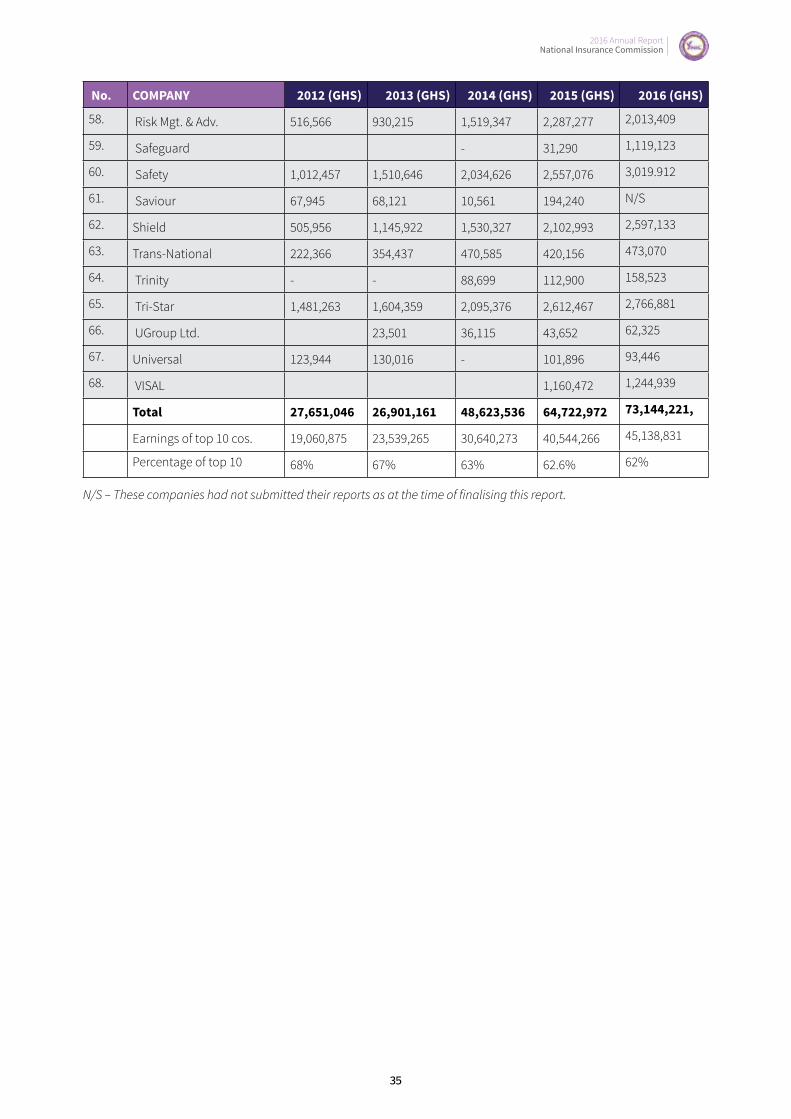

No. COMPANY 2012 (GHS) 2013 (GHS) 2014 (GHS) 2015 (GHS) 2016 (GHS)

58. Risk Mgt. & Adv. 516,566 930,215 1,519,347 2,287,277 2,013,409

59. Safeguard - 31,290 1,119,123

60. Safety 1,012,457 1,510,646 2,034,626 2,557,076 3,019.912

61. Saviour 67,945 68,121 10,561 194,240 N/S

62. Shield 505,956 1,145,922 1,530,327 2,102,993 2,597,133

63. Trans-National 222,366 354,437 470,585 420,156 473,070

64. Trinity - - 88,699 112,900 158,523

65. Tri-Star 1,481,263 1,604,359 2,095,376 2,612,467 2,766,881

66. UGroup Ltd. 23,501 36,115 43,652 62,325

67. Universal 123,944 130,016 - 101,896 93,446

68. VISAL 1,160,472 1,244,939

Total 27,651,046 26,901,161 48,623,536 64,722,972 73,144,221,

Earnings of top 10 cos. 19,060,875 23,539,265 30,640,273 40,544,266 45,138,831

Percentage of top 10 68% 67% 63% 62.6% 62%

N/S – These companies had not submitted their reports as at the time of finalising this report.

2016 Annual Report National Insurance Commission

36

LIFE COMPANIESThe Life sector grew by 21% in 2016 in terms of gross premium income. The analyses below do not include Adamas Life, First Insurance, Capital Express and Millennium Life Insurance Company. Companies with ratios out of range have not been included in determining the industry averages for the periods under review.

Key Income Statement Figures (2013-2015)

2016 2015 2014 2013

(GHS’m) (GHS’m) (GHS’m)

Gross Premium 858,781,522 705,853,360 578,927,147 469,825,330

Reinsurance 20,759,532 15,873,558 8,663,319 6,212,561

Net Premiums 838,021,990 688,003,933 571,818,794 462,612,769

Transfer to Life Fund (277,458,482) (268,854,540) (182,727,720) (210,035,111)

Underwriting Results (261,652,225) (312,247,111) (139,587,727) (23,352,153)

Net Policyholder Benefits Paid 443,544,001 392,832,147 305,093,314 213,783,081

Commissions 98,572,197 85,751,897 63,568,911 48,832,669

Management Expenses 253,938,737 252,806,835 169,075,741 114,070,306

Other Income 14,340,046 34,539,660 25,352,347 6,403,376

Investment Income 378,305,473 283,663,463 176,907,615 172,877,282

Net Profit after tax 98,237,141 (5,831,749) 54,648,759 46,298,727

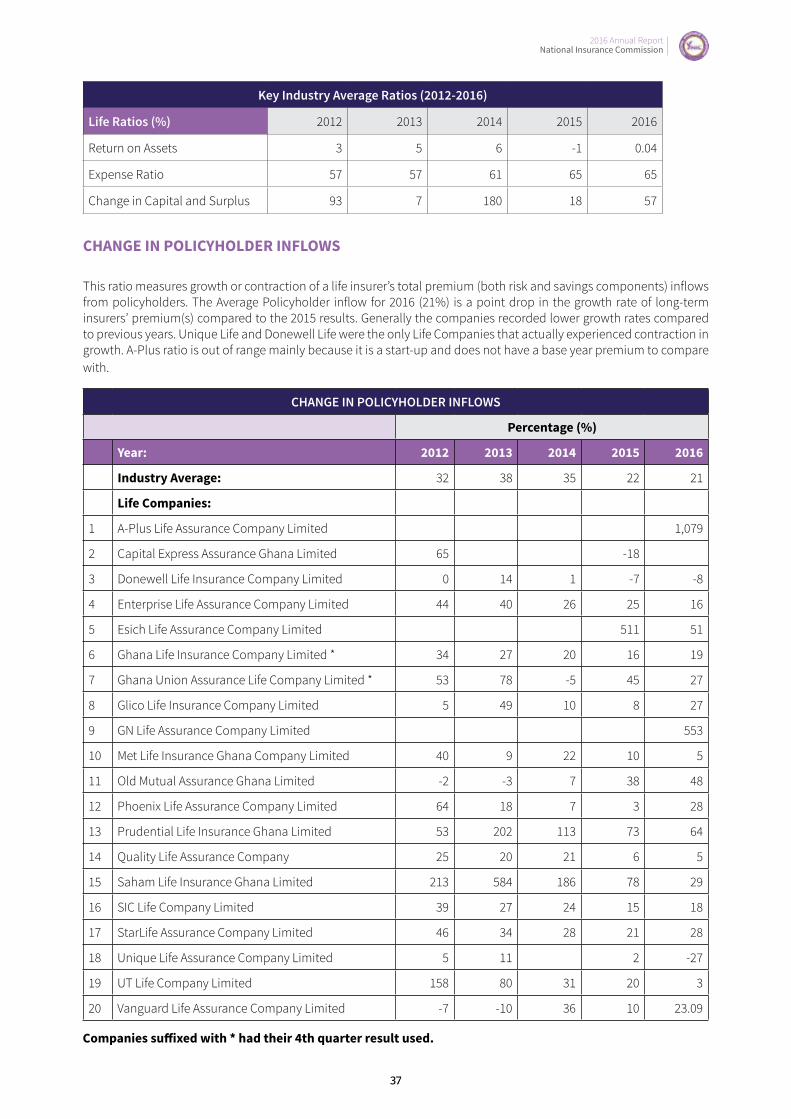

Key Industry Average Ratios (2012-2016)

Life Ratios (%) 2012 2013 2014 2015 2016

Change in policyholder inflows 32 31 35 22 21

Policyholder Coverage (TP/Equity) 2.7x 2.6x 1.9x 1.8x 1.6x

Investment to Total Asset 70 70 78 84 84

Policyholder Benefits Cover (Inv./TP) 168 138 154 144 253

Retention Ratio 97 97 95 91 91

Investment Yield 12 19 18 17 16

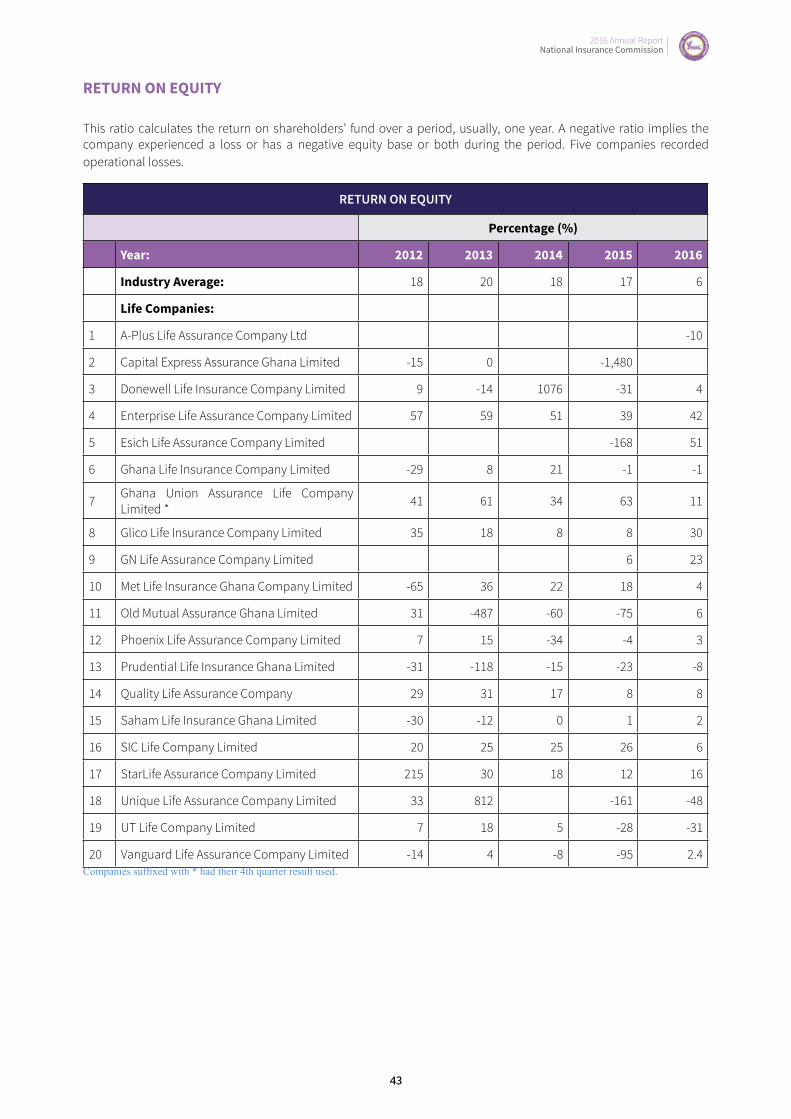

Return on Equity 7.5 20 18 17 6

PERFORMANCE INDICATORS

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

37

Key Industry Average Ratios (2012-2016)

Life Ratios (%) 2012 2013 2014 2015 2016

Return on Assets 3 5 6 -1 0.04

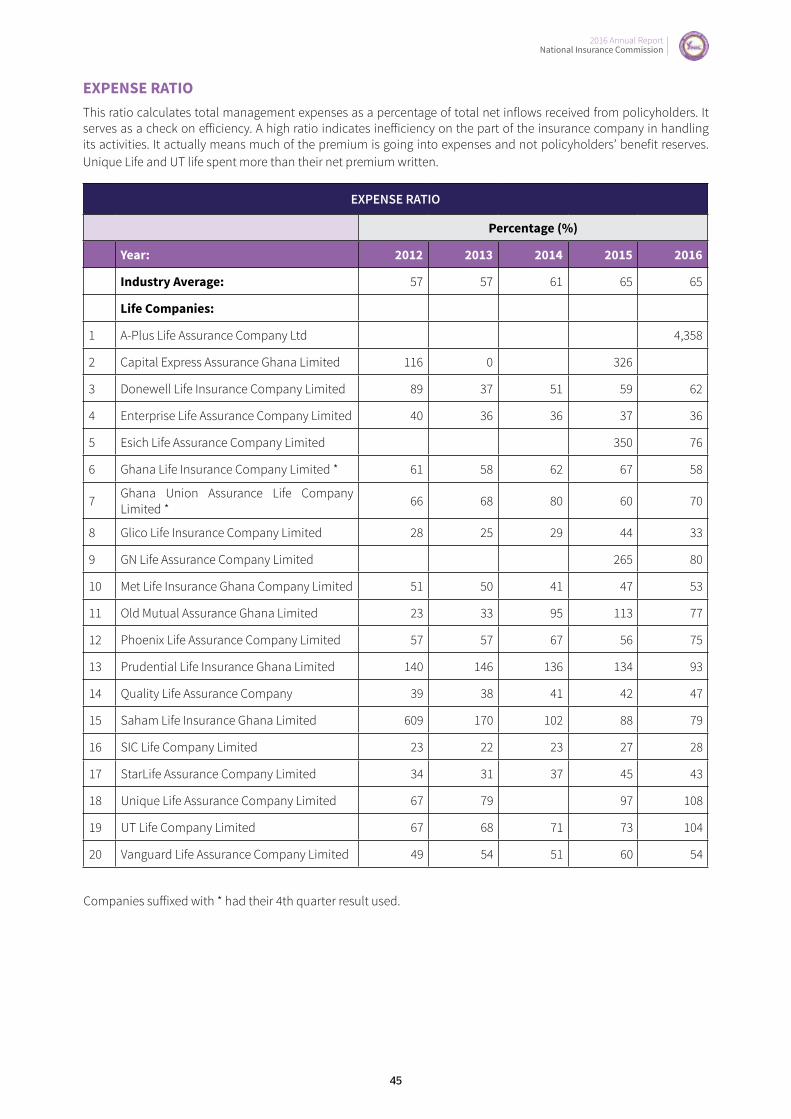

Expense Ratio 57 57 61 65 65

Change in Capital and Surplus 93 7 180 18 57

CHANGE IN POLICYHOLDER INFLOWS

This ratio measures growth or contraction of a life insurer’s total premium (both risk and savings components) inflows from policyholders. The Average Policyholder inflow for 2016 (21%) is a point drop in the growth rate of long-term insurers’ premium(s) compared to the 2015 results. Generally the companies recorded lower growth rates compared to previous years. Unique Life and Donewell Life were the only Life Companies that actually experienced contraction in growth. A-Plus ratio is out of range mainly because it is a start-up and does not have a base year premium to compare with.

CHANGE IN POLICYHOLDER INFLOWS

Percentage (%)

Year: 2012 2013 2014 2015 2016

Industry Average: 32 38 35 22 21

Life Companies:

1 A-Plus Life Assurance Company Limited 1,079

2 Capital Express Assurance Ghana Limited 65 -18

3 Donewell Life Insurance Company Limited 0 14 1 -7 -8

4 Enterprise Life Assurance Company Limited 44 40 26 25 16

5 Esich Life Assurance Company Limited 511 51

6 Ghana Life Insurance Company Limited * 34 27 20 16 19

7 Ghana Union Assurance Life Company Limited * 53 78 -5 45 27

8 Glico Life Insurance Company Limited 5 49 10 8 27

9 GN Life Assurance Company Limited 553

10 Met Life Insurance Ghana Company Limited 40 9 22 10 5

11 Old Mutual Assurance Ghana Limited -2 -3 7 38 48

12 Phoenix Life Assurance Company Limited 64 18 7 3 28

13 Prudential Life Insurance Ghana Limited 53 202 113 73 64

14 Quality Life Assurance Company 25 20 21 6 5

15 Saham Life Insurance Ghana Limited 213 584 186 78 29

16 SIC Life Company Limited 39 27 24 15 18

17 StarLife Assurance Company Limited 46 34 28 21 28

18 Unique Life Assurance Company Limited 5 11 2 -27

19 UT Life Company Limited 158 80 31 20 3

20 Vanguard Life Assurance Company Limited -7 -10 36 10 23.09

Companies suffixed with * had their 4th quarter result used.

2016 Annual Report National Insurance Commission

38

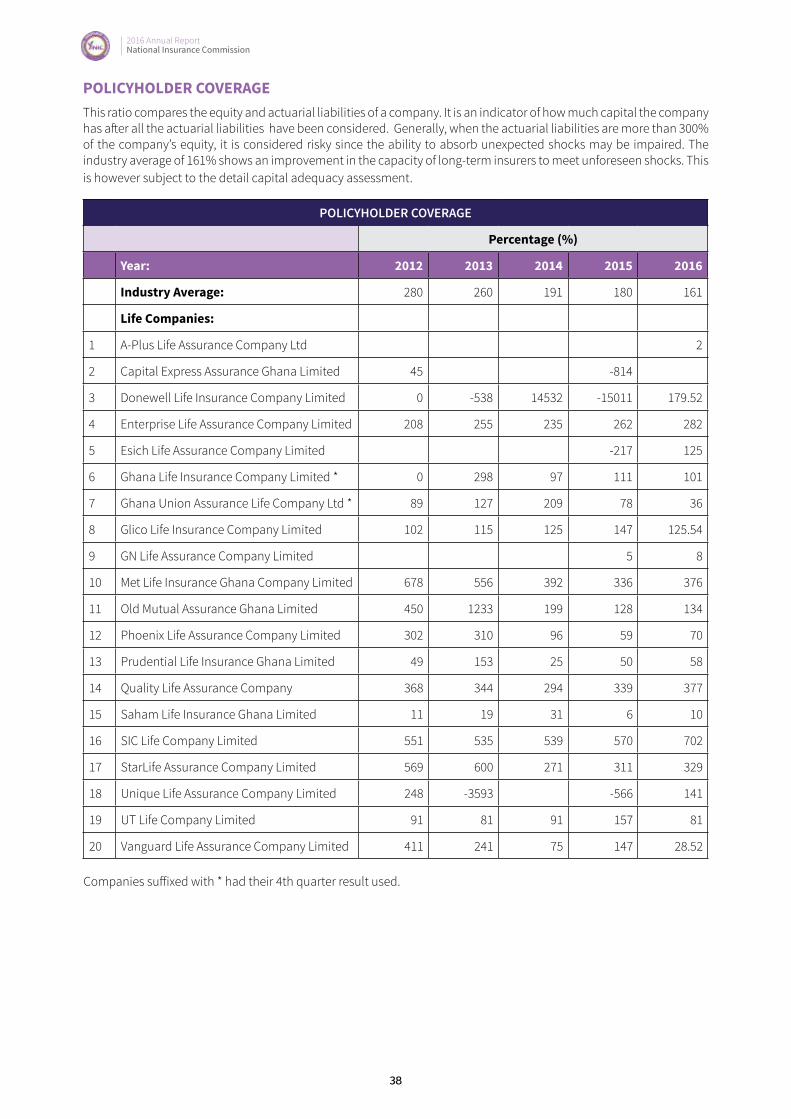

POLICYHOLDER COVERAGEThis ratio compares the equity and actuarial liabilities of a company. It is an indicator of how much capital the company has after all the actuarial liabilities have been considered. Generally, when the actuarial liabilities are more than 300% of the company’s equity, it is considered risky since the ability to absorb unexpected shocks may be impaired. The industry average of 161% shows an improvement in the capacity of long-term insurers to meet unforeseen shocks. This is however subject to the detail capital adequacy assessment.

POLICYHOLDER COVERAGE

Percentage (%)

Year: 2012 2013 2014 2015 2016

Industry Average: 280 260 191 180 161

Life Companies:

1 A-Plus Life Assurance Company Ltd 2

2 Capital Express Assurance Ghana Limited 45 -814

3 Donewell Life Insurance Company Limited 0 -538 14532 -15011 179.52

4 Enterprise Life Assurance Company Limited 208 255 235 262 282

5 Esich Life Assurance Company Limited -217 125

6 Ghana Life Insurance Company Limited * 0 298 97 111 101

7 Ghana Union Assurance Life Company Ltd * 89 127 209 78 36

8 Glico Life Insurance Company Limited 102 115 125 147 125.54

9 GN Life Assurance Company Limited 5 8

10 Met Life Insurance Ghana Company Limited 678 556 392 336 376

11 Old Mutual Assurance Ghana Limited 450 1233 199 128 134

12 Phoenix Life Assurance Company Limited 302 310 96 59 70

13 Prudential Life Insurance Ghana Limited 49 153 25 50 58

14 Quality Life Assurance Company 368 344 294 339 377

15 Saham Life Insurance Ghana Limited 11 19 31 6 10

16 SIC Life Company Limited 551 535 539 570 702

17 StarLife Assurance Company Limited 569 600 271 311 329

18 Unique Life Assurance Company Limited 248 -3593 -566 141

19 UT Life Company Limited 91 81 91 157 81

20 Vanguard Life Assurance Company Limited 411 241 75 147 28.52 Companies suffixed with * had their 4th quarter result used.

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

39

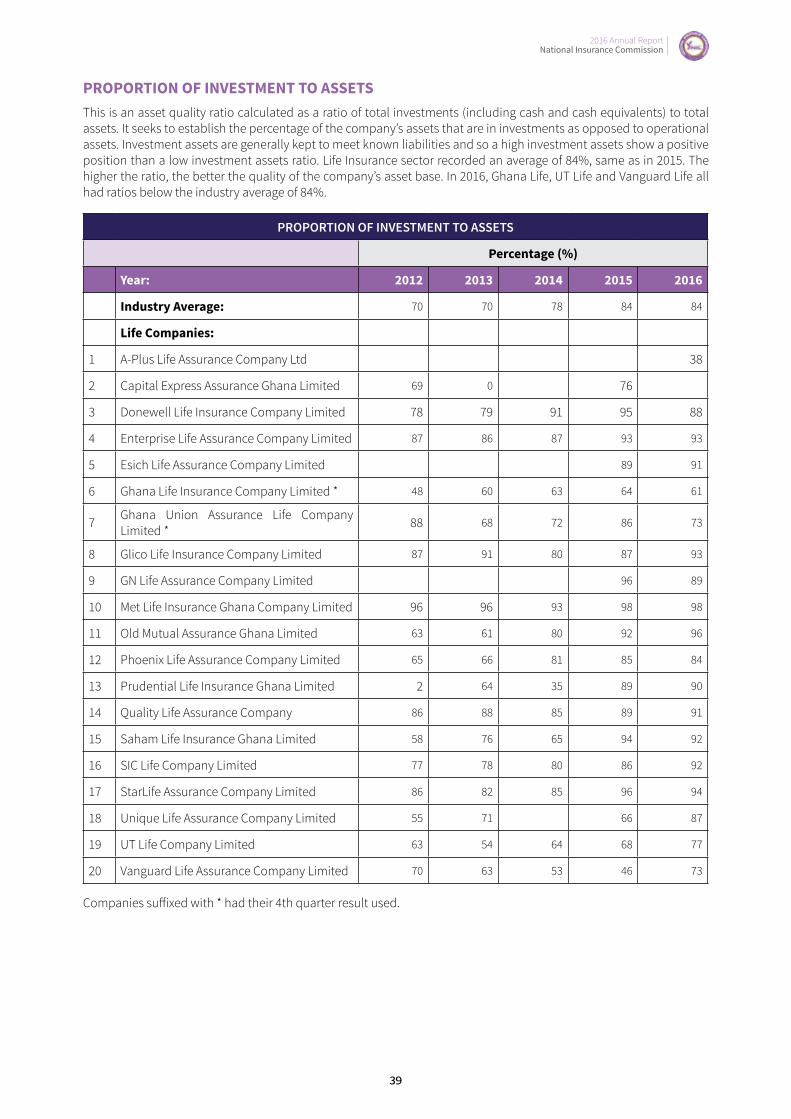

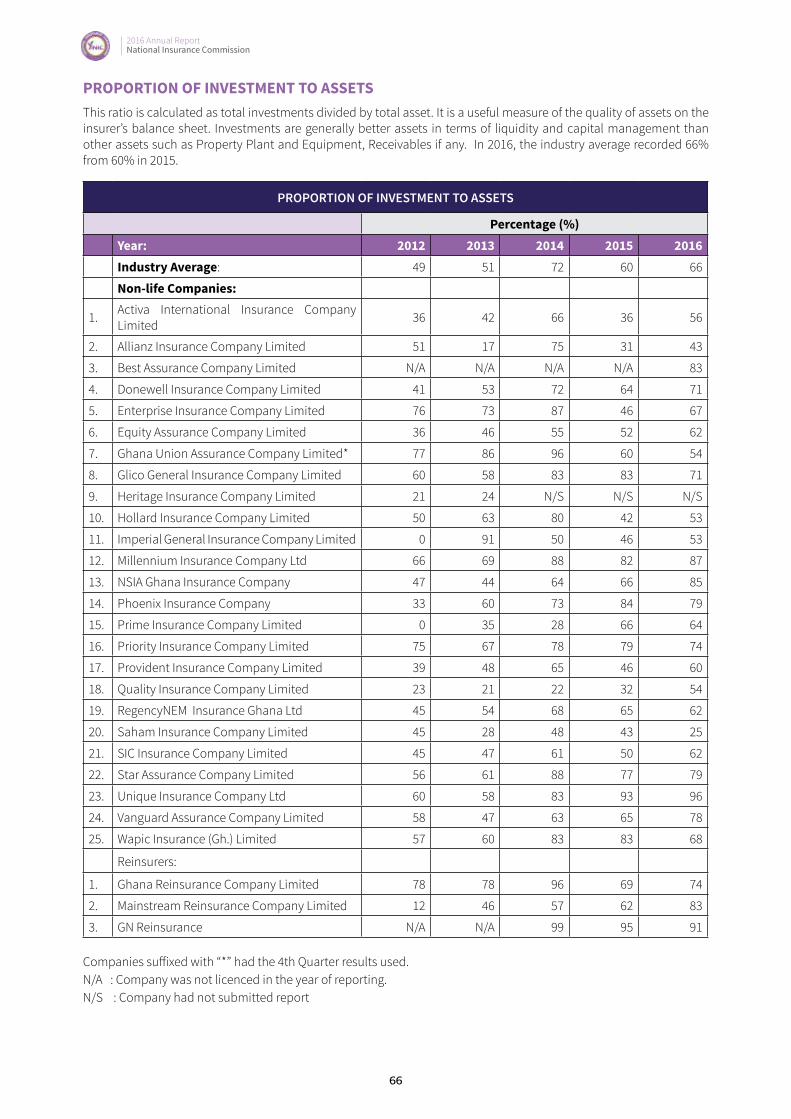

PROPORTION OF INVESTMENT TO ASSETSThis is an asset quality ratio calculated as a ratio of total investments (including cash and cash equivalents) to total assets. It seeks to establish the percentage of the company’s assets that are in investments as opposed to operational assets. Investment assets are generally kept to meet known liabilities and so a high investment assets show a positive position than a low investment assets ratio. Life Insurance sector recorded an average of 84%, same as in 2015. The higher the ratio, the better the quality of the company’s asset base. In 2016, Ghana Life, UT Life and Vanguard Life all had ratios below the industry average of 84%.

PROPORTION OF INVESTMENT TO ASSETS

Percentage (%)

Year: 2012 2013 2014 2015 2016

Industry Average: 70 70 78 84 84

Life Companies:

1 A-Plus Life Assurance Company Ltd 38

2 Capital Express Assurance Ghana Limited 69 0 76

3 Donewell Life Insurance Company Limited 78 79 91 95 88

4 Enterprise Life Assurance Company Limited 87 86 87 93 93

5 Esich Life Assurance Company Limited 89 91

6 Ghana Life Insurance Company Limited * 48 60 63 64 61

7 Ghana Union Assurance Life Company Limited * 88 68 72 86 73

8 Glico Life Insurance Company Limited 87 91 80 87 93

9 GN Life Assurance Company Limited 96 89

10 Met Life Insurance Ghana Company Limited 96 96 93 98 98

11 Old Mutual Assurance Ghana Limited 63 61 80 92 96

12 Phoenix Life Assurance Company Limited 65 66 81 85 84

13 Prudential Life Insurance Ghana Limited 2 64 35 89 90

14 Quality Life Assurance Company 86 88 85 89 91

15 Saham Life Insurance Ghana Limited 58 76 65 94 92

16 SIC Life Company Limited 77 78 80 86 92

17 StarLife Assurance Company Limited 86 82 85 96 94

18 Unique Life Assurance Company Limited 55 71 66 87

19 UT Life Company Limited 63 54 64 68 77

20 Vanguard Life Assurance Company Limited 70 63 53 46 73

Companies suffixed with * had their 4th quarter result used.

2016 Annual Report National Insurance Commission

40

POLICYHOLDER BENEFIT COVERThis is a measure of investment adequacy with respect to an insurer’s liability. It is calculated as a ratio of total investments to actuarial liabilities. It seeks to assess the adequacy of the company’s investments to cover the policyholder liabilities. The Life Sector recorded an average of 253% in 2016. This is the best in five years. The investment assets should, as a minimum, cover policyholder benefits. A ratio of less than 100% means that the company does not have enough investments to cover the policyholder liabilities. No company recorded a ratio below 100%. This ratio helps to analyse the adequacy of a company’s technical provisions and must be considered alongside policyholder benefit cover to ensure a company is not associated with the risk of under provisioning. A-Plus and GN Life ratios are out of range because it is a start-up.

POLICYHOLDER BENEFIT COVER

Percentage (%)

Year: 2012 2013 2014 2015 2016

Industry Average: 121 138 144 144 253

Life Companies:

1 A-Plus Life Assurance Company Ltd 1,796

2 Capital Express Assurance Ghana Limited 240 0 106

3 Donewell Life Insurance Company Limited 59 68 96 99 142

4 Enterprise Life Assurance Company Limited 138 132 134 135 134

5 Esich Life Assurance Company Limited 93 211

6 Ghana Life Insurance Company Limited * 72 91 146 135 135

7 Ghana Union Assurance Life Company Limited * 206 128 115 204 283

8 Glico Life Insurance Company Limited 183 180 150 158 194

9 GN Life Assurance Company Limited 2407 1353

10 Met Life Insurance Ghana Company Limited 121 128 122 135 131

11 Old Mutual Assurance Ghana Limited 77 69 132 175 178

12 Phoenix Life Assurance Company Limited 99 102 183 256 234

13 Prudential Life Insurance Ghana Limited 7 99 191 313 272

14 Quality Life Assurance Company 112 116 117 119 117

15 Saham Life Insurance Ghana Limited 815 702 393 1883 1,059

16 SIC Life Company Limited 96 97 99 103 109

17 StarLife Assurance Company Limited 104 101 123 134 131

18 Unique Life Assurance Company Limited 77 72 59 155

19 UT Life Company Limited 151 159 161 127 185

20 Vanguard Life Assurance Company Limited 89 96 145 103 407

Companies suffixed with * had their 4th quarter result used.

2016 Annual Report National Insurance Commission

2016 Annual Report National Insurance Commission

41

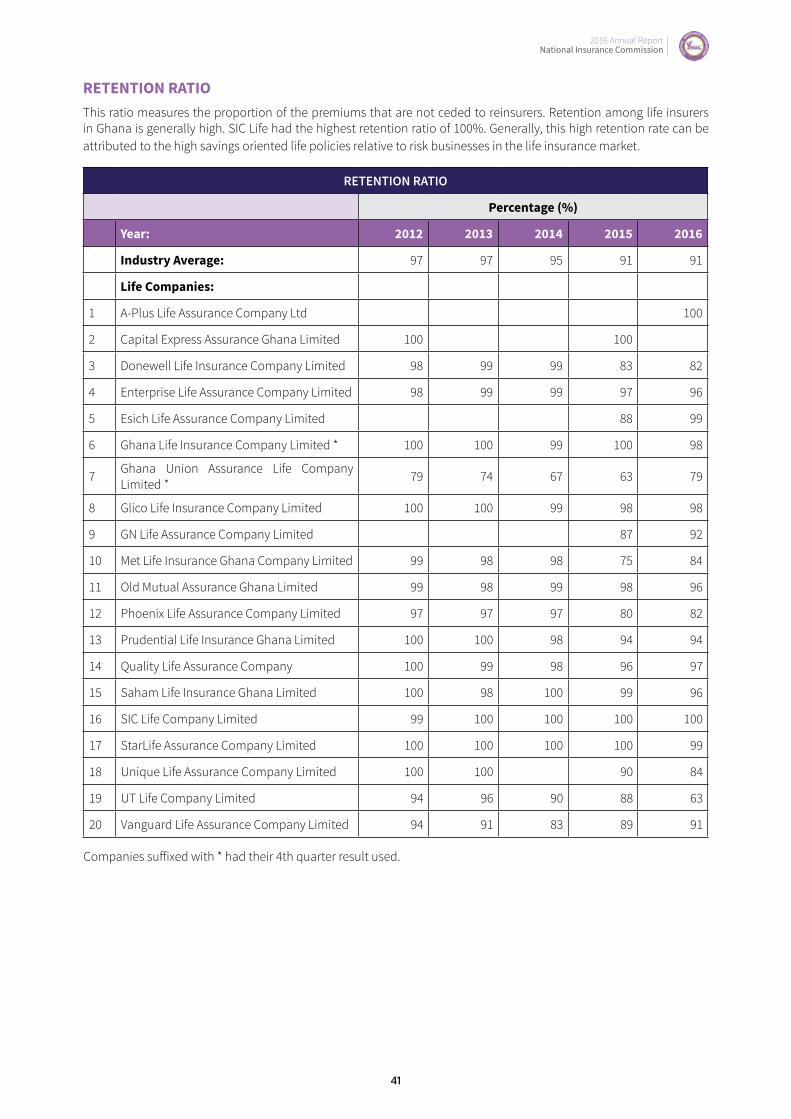

RETENTION RATIOThis ratio measures the proportion of the premiums that are not ceded to reinsurers. Retention among life insurers in Ghana is generally high. SIC Life had the highest retention ratio of 100%. Generally, this high retention rate can be attributed to the high savings oriented life policies relative to risk businesses in the life insurance market.

RETENTION RATIO

Percentage (%)

Year: 2012 2013 2014 2015 2016

Industry Average: 97 97 95 91 91

Life Companies:

1 A-Plus Life Assurance Company Ltd 100

2 Capital Express Assurance Ghana Limited 100 100

3 Donewell Life Insurance Company Limited 98 99 99 83 82

4 Enterprise Life Assurance Company Limited 98 99 99 97 96

5 Esich Life Assurance Company Limited 88 99

6 Ghana Life Insurance Company Limited * 100 100 99 100 98

7 Ghana Union Assurance Life Company Limited * 79 74 67 63 79

8 Glico Life Insurance Company Limited 100 100 99 98 98

9 GN Life Assurance Company Limited 87 92

10 Met Life Insurance Ghana Company Limited 99 98 98 75 84

11 Old Mutual Assurance Ghana Limited 99 98 99 98 96

12 Phoenix Life Assurance Company Limited 97 97 97 80 82

13 Prudential Life Insurance Ghana Limited 100 100 98 94 94

14 Quality Life Assurance Company 100 99 98 96 97

15 Saham Life Insurance Ghana Limited 100 98 100 99 96

16 SIC Life Company Limited 99 100 100 100 100

17 StarLife Assurance Company Limited 100 100 100 100 99

18 Unique Life Assurance Company Limited 100 100 90 84

19 UT Life Company Limited 94 96 90 88 63

20 Vanguard Life Assurance Company Limited 94 91 83 89 91

Companies suffixed with * had their 4th quarter result used.

2016 Annual Report National Insurance Commission

42

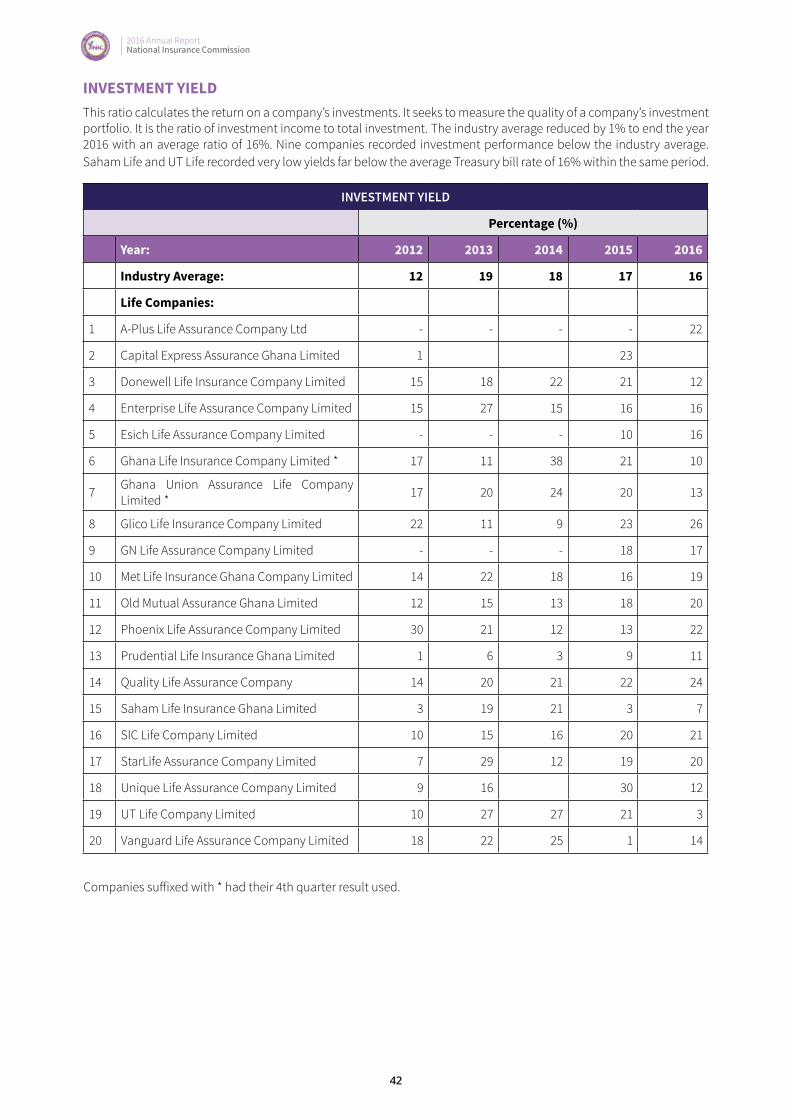

INVESTMENT YIELDThis ratio calculates the return on a company’s investments. It seeks to measure the quality of a company’s investment portfolio. It is the ratio of investment income to total investment. The industry average reduced by 1% to end the year 2016 with an average ratio of 16%. Nine companies recorded investment performance below the industry average. Saham Life and UT Life recorded very low yields far below the average Treasury bill rate of 16% within the same period.

INVESTMENT YIELD

Percentage (%)

Year: 2012 2013 2014 2015 2016

Industry Average: 12 19 18 17 16

Life Companies:

1 A-Plus Life Assurance Company Ltd - - - - 22

2 Capital Express Assurance Ghana Limited 1 23

3 Donewell Life Insurance Company Limited 15 18 22 21 12

4 Enterprise Life Assurance Company Limited 15 27 15 16 16

5 Esich Life Assurance Company Limited - - - 10 16

6 Ghana Life Insurance Company Limited * 17 11 38 21 10

7 Ghana Union Assurance Life Company Limited * 17 20 24 20 13

8 Glico Life Insurance Company Limited 22 11 9 23 26

9 GN Life Assurance Company Limited - - - 18 17

10 Met Life Insurance Ghana Company Limited 14 22 18 16 19

11 Old Mutual Assurance Ghana Limited 12 15 13 18 20

12 Phoenix Life Assurance Company Limited 30 21 12 13 22

13 Prudential Life Insurance Ghana Limited 1 6 3 9 11

14 Quality Life Assurance Company 14 20 21 22 24

15 Saham Life Insurance Ghana Limited 3 19 21 3 7

16 SIC Life Company Limited 10 15 16 20 21

17 StarLife Assurance Company Limited 7 29 12 19 20

18 Unique Life Assurance Company Limited 9 16 30 12

19 UT Life Company Limited 10 27 27 21 3

20 Vanguard Life Assurance Company Limited 18 22 25 1 14

Companies suffixed with * had their 4th quarter result used.