11 policies, dynamics & trends that are shaping today’s solar industry ctf solar subgroup...

TRANSCRIPT

11

Policies, Dynamics & Trends That are Shaping Today’s

Solar Industry

CTF Solar SubgroupApril 5, 2010

2

Government Policies - Dave Government Policies Update

• US Programs Dave Fraser• Copenhagen Dinah Cheng• Global trends Paritosh Rajora

PV Technology & Roadmap Wen-Ben Chou US Market Dynamics

• Status & Trends Ranjeet Pancholy

• VCs & Funding Dinah Cheng Key Countries

• Germany Ravinder Sachdeva

• Spain Ranjeet Pancholy• China Mike Hsieh• India Ranjeet Pancholy

Career Options Steve Campbell• Solar Subgroup landings Keith Imai

Summary & coordinator Keith Imai

3

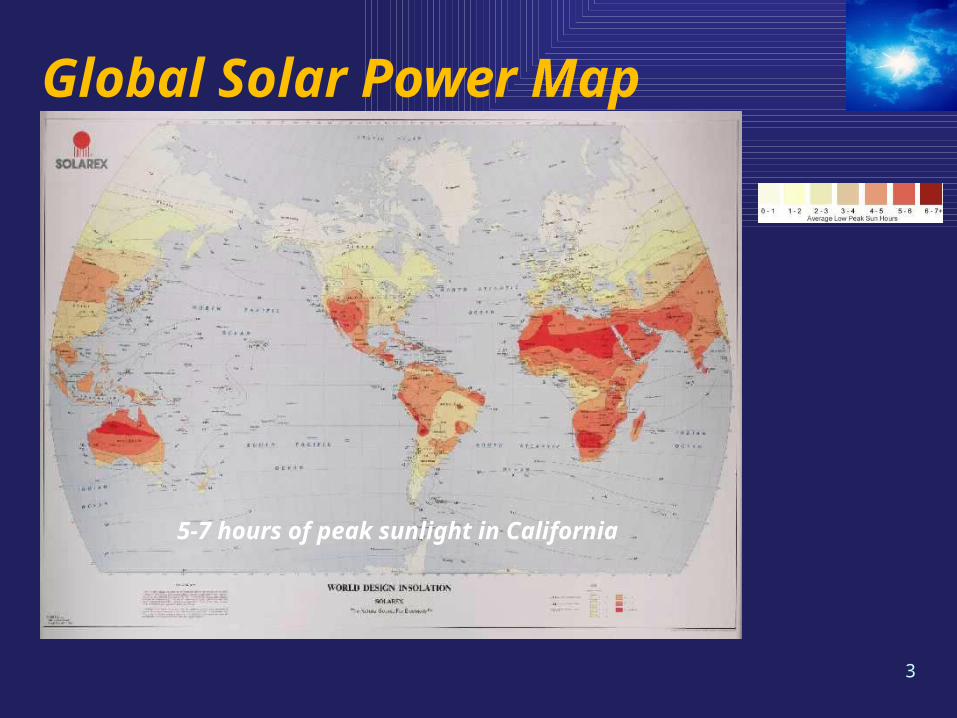

Global Solar Power Map

5-7 hours of peak sunlight in California

4

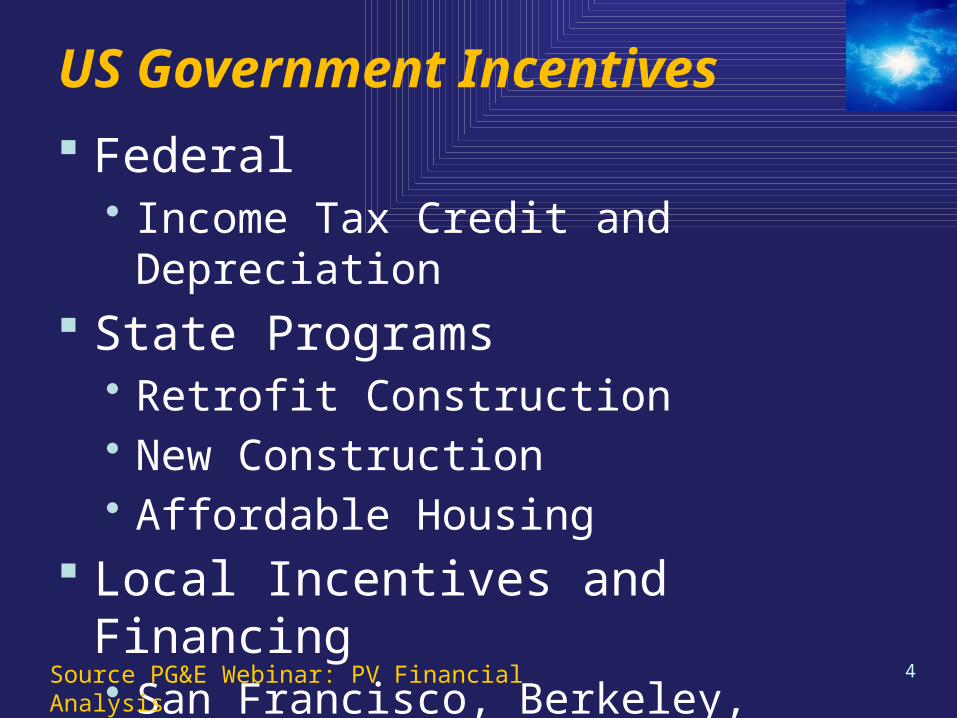

US Government Incentives

Federal • Income Tax Credit and Depreciation

State Programs• Retrofit Construction• New Construction• Affordable Housing

Local Incentives and Financing• San Francisco, Berkeley, Sonoma

Source PG&E Webinar: PV Financial Analysis

5

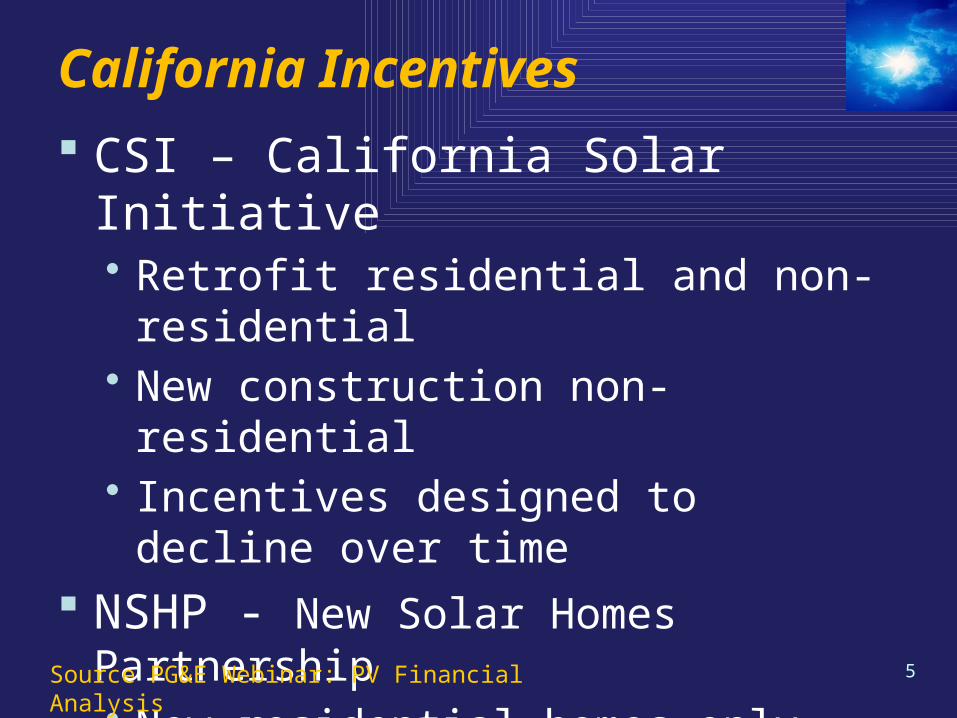

California Incentives

CSI – California Solar Initiative• Retrofit residential and non-residential• New construction non-residential• Incentives designed to decline over time

NSHP - New Solar Homes Partnership• New residential homes only• Builders, developers, custom homeowners

Source PG&E Webinar: PV Financial Analysis

6

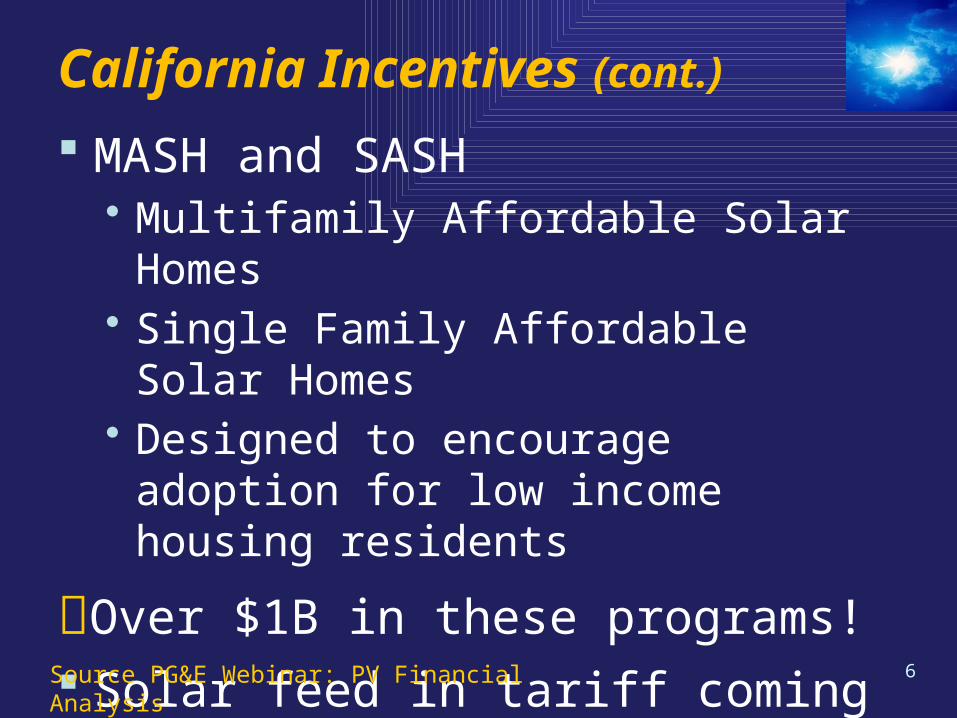

California Incentives (cont.)

MASH and SASH• Multifamily Affordable Solar Homes• Single Family Affordable Solar Homes • Designed to encourage adoption for low

income housing residents

Over $1B in these programs! Solar feed in tariff coming soon

Source PG&E Webinar: PV Financial Analysis

7

Making Solar Affordable

“Energy Conservation First” strategyEnergy Audits Retrofit projects Smart Meters + home management systemsGovernment + PG+E incentives for conservation with rebates and tax credits

8

2009 Copenhagen Mission Set new agreement to

extend the Kyoto Protocol beyond 20121. Ambitious emission targets

for developed countries

2. Appropriate mitigation actions of developing countries

3. Financial and technological support for both adaptation and mitigation

4. Effective institutional framework with governance structures to address the needs of developing countries

GHG Emissions Control

9

Pre-conference Announcements from the Top Four Emitters China

• Cut CO2 emission intensity (CO2 per GDP) by 40%-45% from 2005 level

US• Cut GHG emissions by ~17% below 2005 levels by 2020• EPA rule that CO2 and other GHG as a toxic gas

• Allows regulation of planet-warming gases without legislation in Congress

Indonesia• Reduce annual carbon emission by 5% and preserving

the Kampar peninsula Brazil

• Reduce >36% of carbon emissions by 2020

10

2009 Copenhagen Accord

Drafted by US, China, India, Brazil, & South Africa Judged a "meaningful agreement" by US Non-legally binding commitments Not passed unanimously

• Opposed by many countries and NGO Recognized that climate change is one of the

greatest challenges…actions needed to keep global temperature increases to below 2°C

11

Global Government Policies

64 countries have some type of policy to promote renewable power generation

Feed-in tariffs are most widely used policy• 45 countries• Adopted first time: South Africa, Philippines,

Ukraine, Poland, Kenya• Engaged in developing Feed-in-policies: UK,

Japan, Israel, Egypt, Nigeria

12

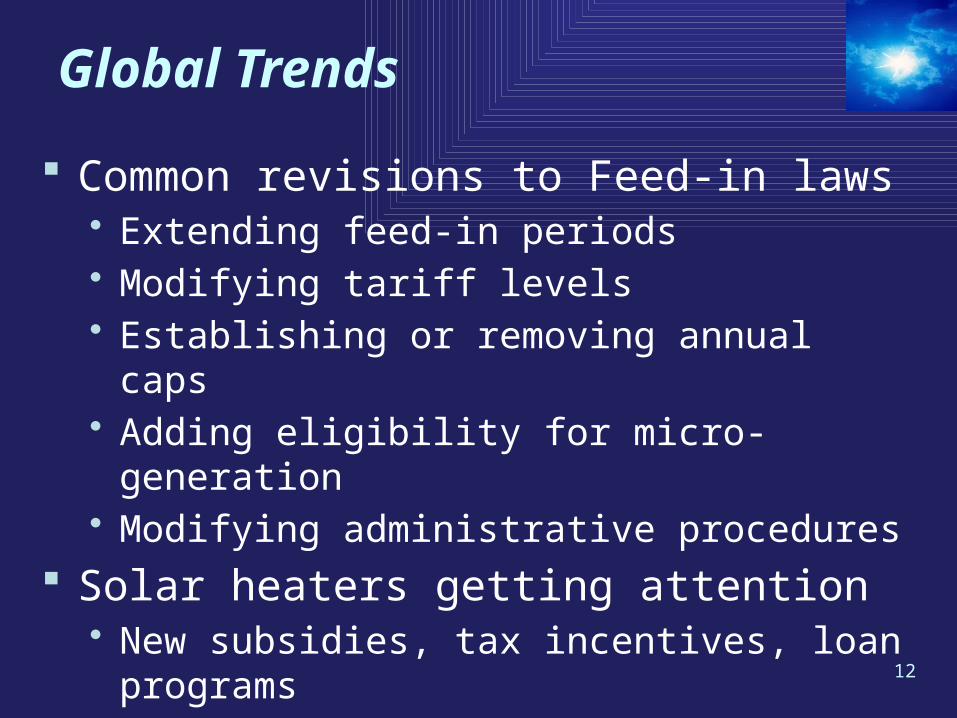

Global Trends

Common revisions to Feed-in laws• Extending feed-in periods• Modifying tariff levels• Establishing or removing annual caps• Adding eligibility for micro-generation• Modifying administrative procedures

Solar heaters getting attention• New subsidies, tax incentives, loan programs

13

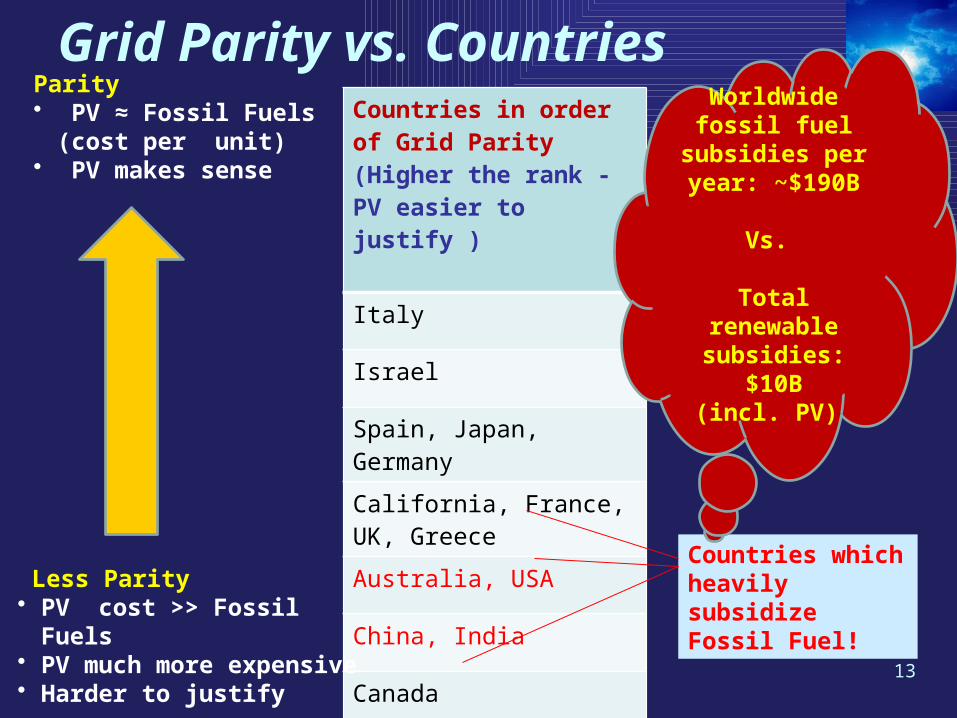

Grid Parity vs. CountriesCountries in order of Grid Parity(Higher the rank - PV easier to justify )

Italy

Israel

Spain, Japan, Germany

California, France, UK, Greece

Australia, USA

China, India

Canada

Russia

Parity • PV ≈ Fossil Fuels (cost

per unit)• PV makes sense

Less Parity• PV cost >> Fossil Fuels• PV much more expensive• Harder to justify

Countries which heavily subsidize Fossil Fuel!

Worldwidefossil fuel

subsidies per year: ~$190B

Vs.

Total renewable subsidies: $10B

(incl. PV)

14

Global Incentives

Top Financial Incentives Countries: (Feed-in-Tariffs, Tax Incentives, Loan Programs)

Germany

France

Greece

California

Italy

USA

Top Regulatory Incentives Countries: (Easing admin. procedures, easing eligibility, removing annual caps)

Greece

Italy

California

Australia, UK, Spain, France

Germany, India

China

USA

15

PV Technology & US Market - Srikanth Government Policies Update

• US Programs Dave Fraser• Copenhagen Dinah Cheng• Global trends Paritosh Rajora

PV Technology & Roadmap Wen-Ben Chou US Market Dynamics

• Status & Trends Ranjeet Pancholy

• VCs & Funding Dinah Cheng Key Countries

• Germany Ravinder Sachdeva

• Spain Ranjeet Pancholy• China Mike Hsieh• India Ranjeet Pancholy

Career Options Steve Campbell• Solar Subgroup landings Keith Imai

Summary & coordinator Keith Imai

16

PV Efficiency Roadmap

17

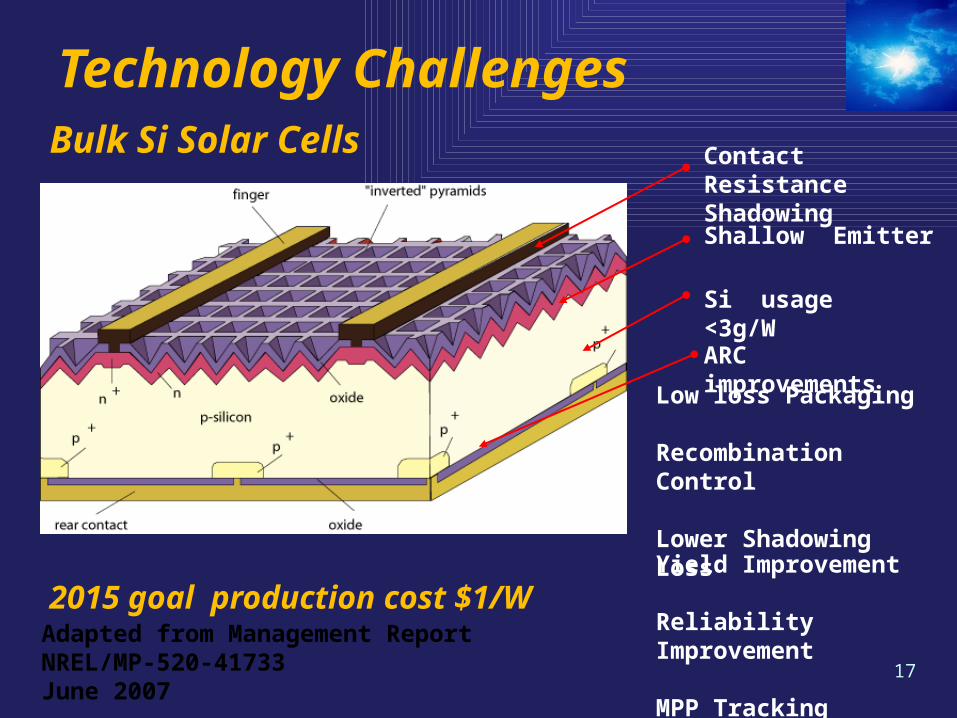

Technology Challenges

Si usage <3g/W

Contact ResistanceShadowing

Shallow Emitter

ARC improvements

Low loss Packaging

Recombination Control

Lower Shadowing Loss

Bulk Si Solar Cells

Yield Improvement

Reliability Improvement

MPP Tracking

2015 goal production cost $1/WAdapted from Management Report NREL/MP-520-41733 June 2007

18

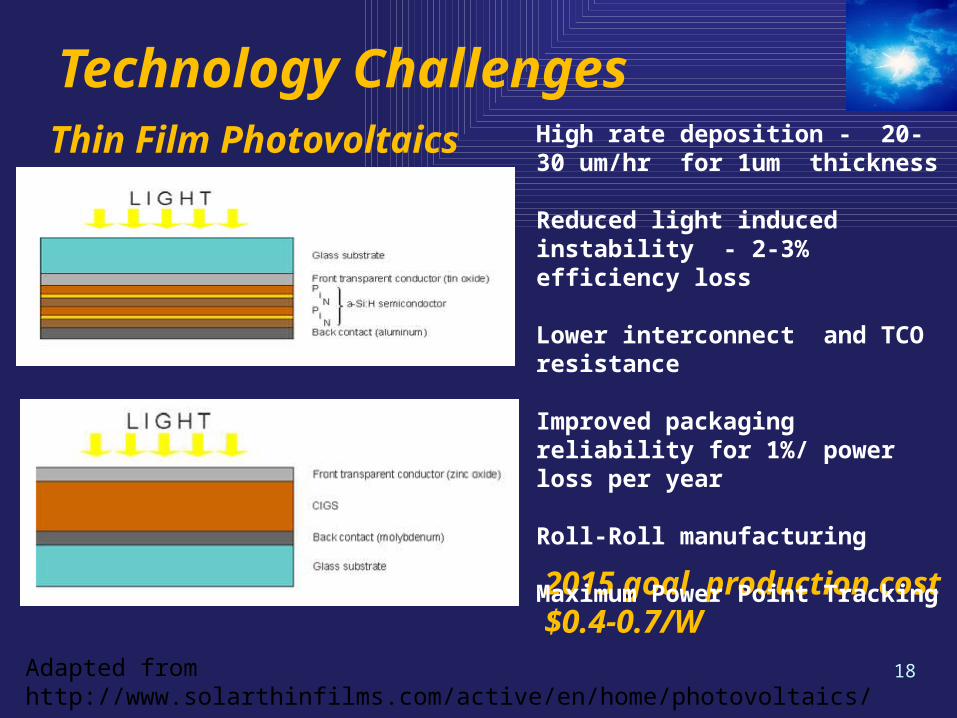

Technology Challenges

Adapted from http://www.solarthinfilms.com/active/en/home/photovoltaics/

2015 goal production cost $0.4-0.7/W

Thin Film Photovoltaics High rate deposition - 20-30 um/hr for 1um thickness

Reduced light induced instability - 2-3% efficiency loss

Lower interconnect and TCO resistance

Improved packaging reliability for 1%/ power loss per year

Roll-Roll manufacturing

Maximum Power Point Tracking

19

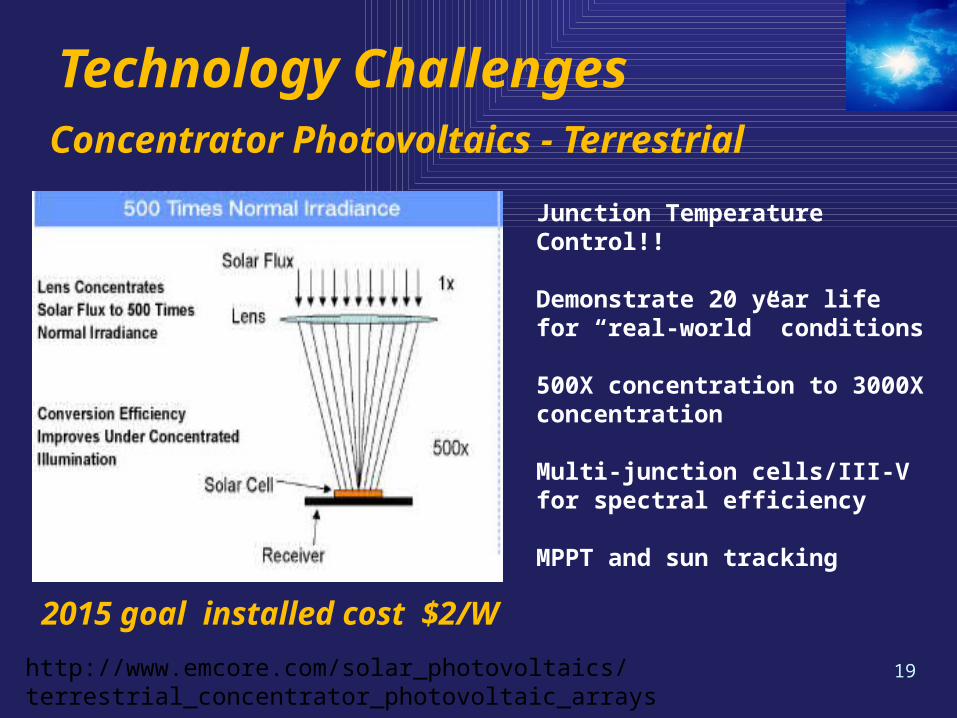

Technology Challenges

http://www.emcore.com/solar_photovoltaics/terrestrial_concentrator_photovoltaic_arrays

2015 goal installed cost $2/W

Concentrator Photovoltaics - Terrestrial

Junction Temperature Control!!

Demonstrate 20 year life for “real-world” conditions

500X concentration to 3000X concentration

Multi-junction cells/III-V for spectral efficiency

MPPT and sun tracking

20

Policy Requirements 2010 - 2020

Long term utility targets and supporting policies• Builds confidence for investment in manufacturing

capacity and deployment of utility scale PV systems

Implement incentive schemes and low cost financing• Catalyses consumer market creation• Incentives will be transitional and decrease over time

Increase R&D funding to sustain technology roadmap• Reduces production and ramp-up costs• Supports longer term technology breakthroughs

21

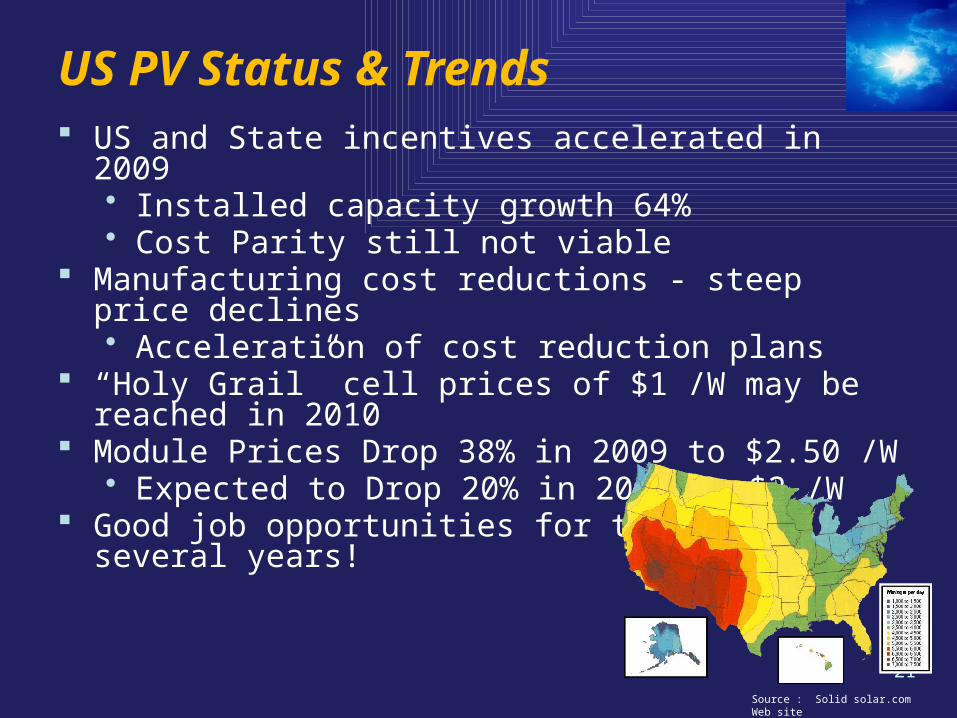

US PV Status & Trends US and State incentives accelerated in 2009

• Installed capacity growth 64%• Cost Parity still not viable

Manufacturing cost reductions - steep price declines• Acceleration of cost reduction plans

“Holy Grail” cell prices of $1 /W may be reached in 2010 Module Prices Drop 38% in 2009 to $2.50 /W

• Expected to Drop 20% in 2010 to $2 /W Good job opportunities for the next several years!

Source : Solid solar.com Web site

22

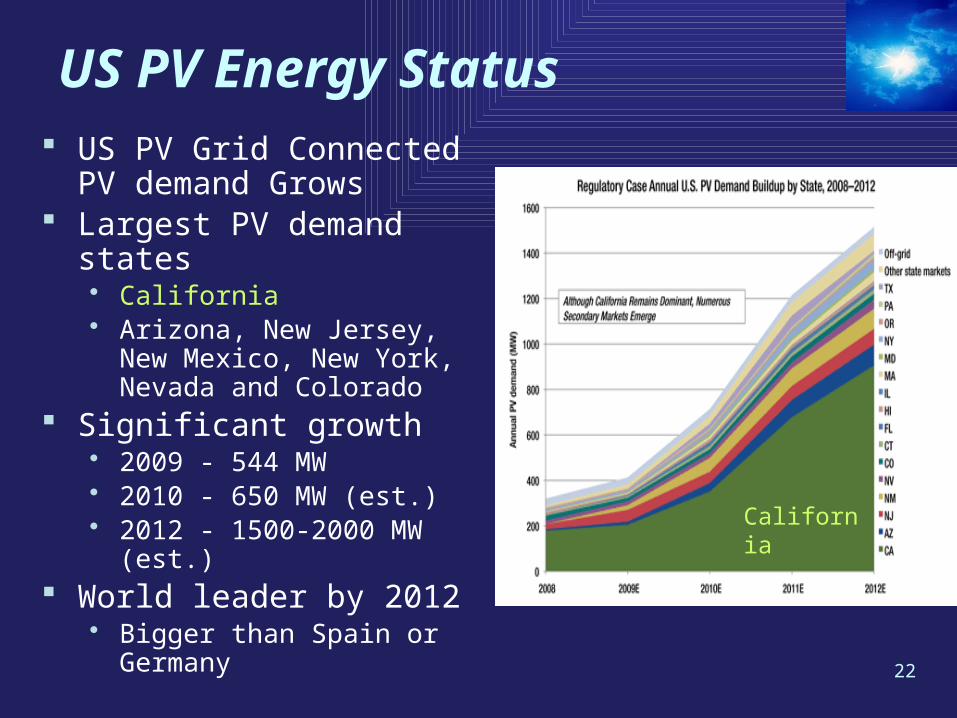

US PV Energy Status US PV Grid Connected PV

demand Grows Largest PV demand states

• California• Arizona, New Jersey, New

Mexico, New York, Nevada and Colorado

Significant growth• 2009 - 544 MW • 2010 - 650 MW (est.)• 2012 - 1500-2000 MW (est.)

World leader by 2012• Bigger than Spain or Germany

California

23

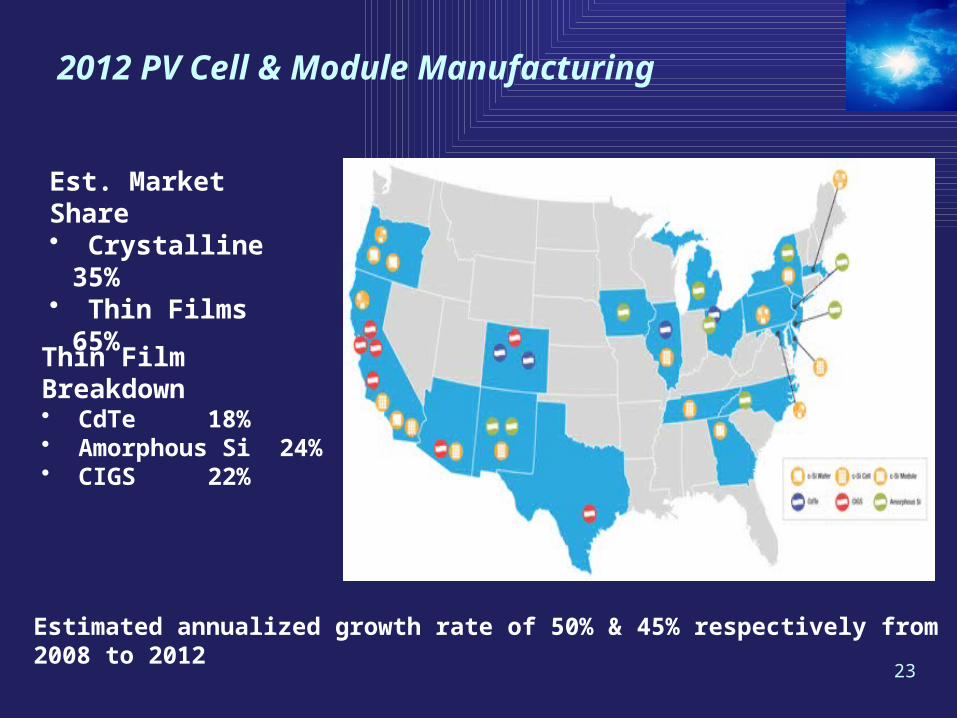

2012 PV Cell & Module Manufacturing

Est. Market Share• Crystalline 35%• Thin Films 65%

Thin Film Breakdown• CdTe 18%• Amorphous Si 24%• CIGS 22%

Estimated annualized growth rate of 50% & 45% respectively from 2008 to 2012

24

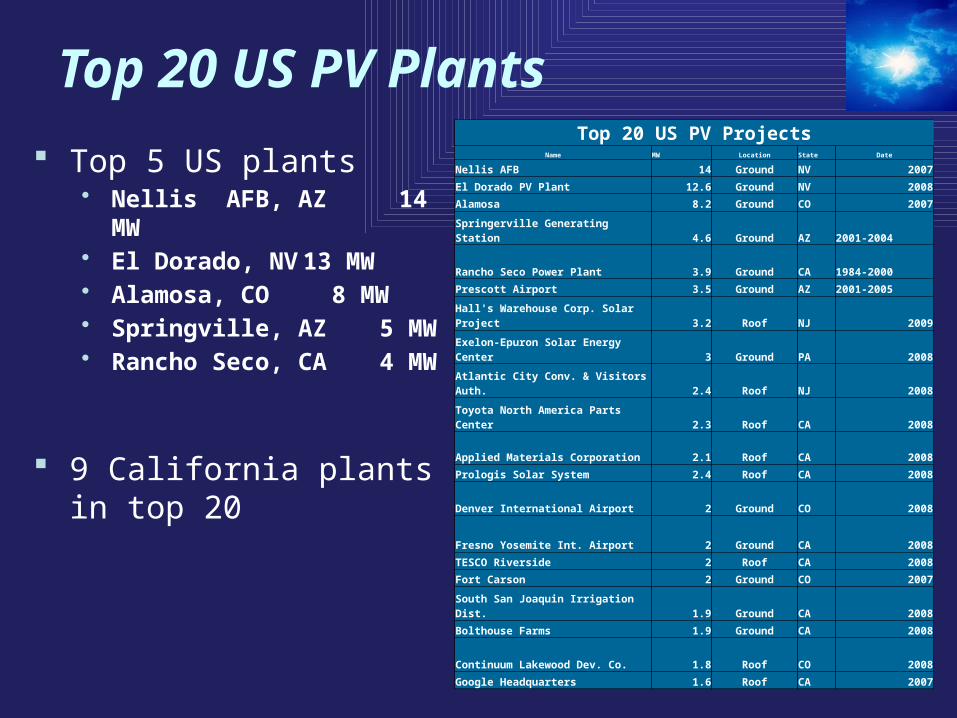

Top 20 US PV ProjectsName MW Location State Date

Nellis AFB 14 Ground NV 2007

El Dorado PV Plant 12.6 Ground NV 2008

Alamosa 8.2 Ground CO 2007

Springerville Generating Station 4.6 Ground AZ 2001-2004

Rancho Seco Power Plant 3.9 Ground CA 1984-2000

Prescott Airport 3.5 Ground AZ 2001-2005

Hall's Warehouse Corp. Solar Project 3.2 Roof NJ 2009

Exelon-Epuron Solar Energy Center 3 Ground PA 2008

Atlantic City Conv. & Visitors Auth. 2.4 Roof NJ 2008

Toyota North America Parts Center 2.3 Roof CA 2008

Applied Materials Corporation 2.1 Roof CA 2008

Prologis Solar System 2.4 Roof CA 2008

Denver International Airport 2 Ground CO 2008

Fresno Yosemite Int. Airport 2 Ground CA 2008

TESCO Riverside 2 Roof CA 2008

Fort Carson 2 Ground CO 2007

South San Joaquin Irrigation Dist. 1.9 Ground CA 2008

Bolthouse Farms 1.9 Ground CA 2008

Continuum Lakewood Dev. Co. 1.8 Roof CO 2008

Google Headquarters 1.6 Roof CA 2007

Top 20 US PV Plants

Top 5 US plants• Nellis AFB, AZ 14 MW • El Dorado, NV 13 MW• Alamosa, CO 8 MW• Springville, AZ 5 MW• Rancho Seco, CA 4

MW

9 California plants in top 20

25

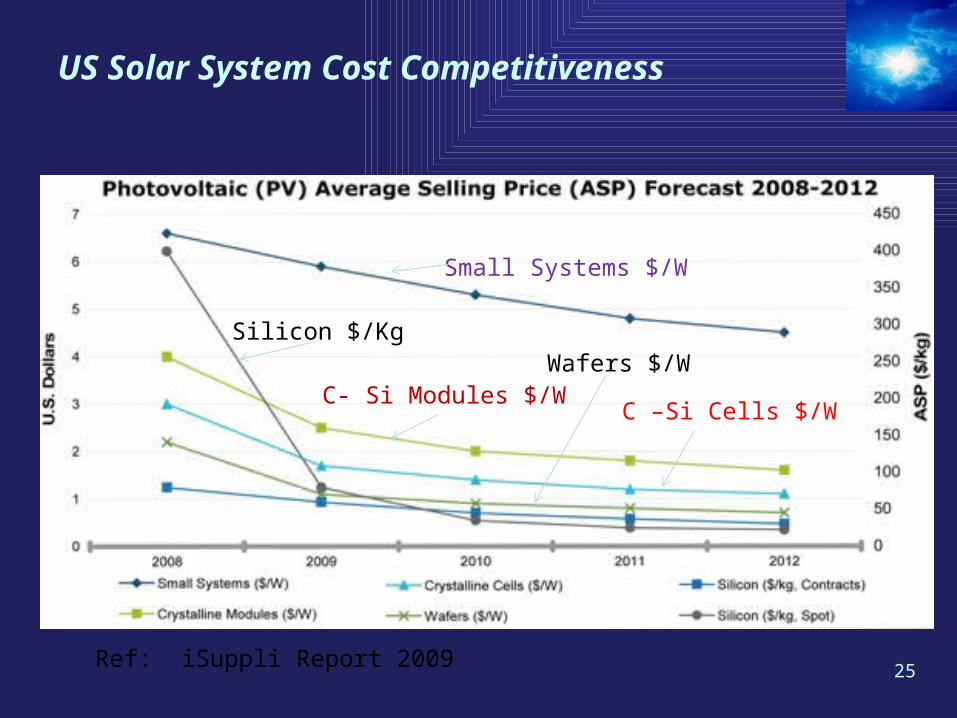

US Solar System Cost Competitiveness

Small Systems $/W

Silicon $/Kg

C- Si Modules $/WC –Si Cells $/W

Wafers $/W

Ref: iSuppli Report 2009

26

The VC’sMost active NEA CMEA Khosla Ventures Kleiner Perkins NGEN Partners DFJ Foundation Capital Quercus Trust

Others Google Ventures, Foundation Capital Northgate Capital Argonaut Private Equity Exxon Sequoia Capital Foundation Capital Fjord Capital Mesirow Capital

2009 Funding trends • Middle stage rounds saw difficulty for less-than-profitable

companies • Increase in early stage (>110 deals) series A & seed rounds

27

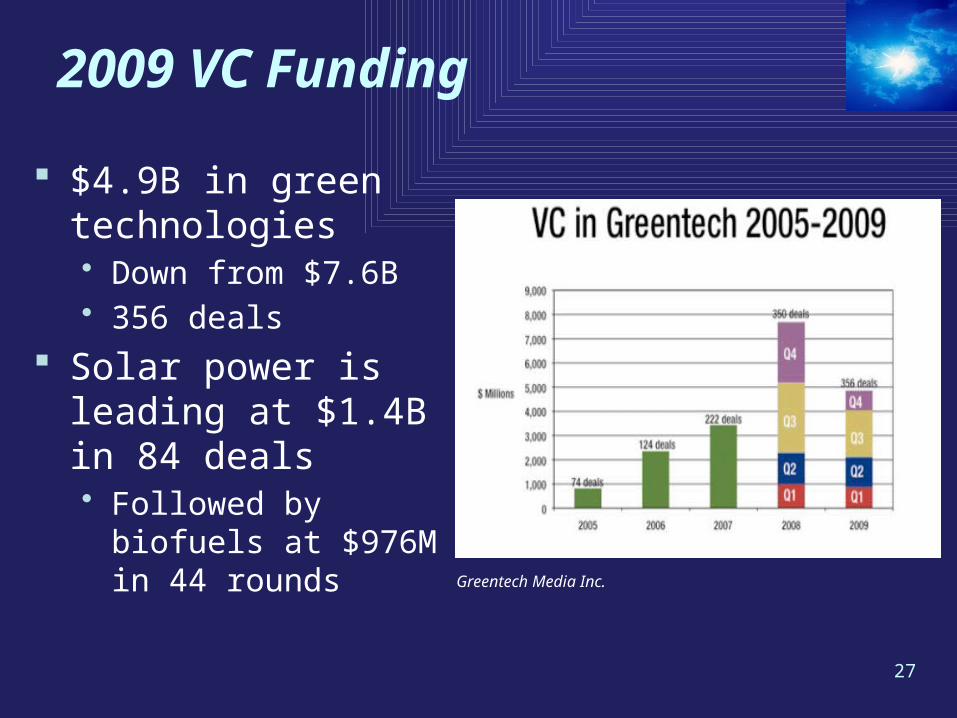

2009 VC Funding

$4.9B in green technologies • Down from $7.6B• 356 deals

Solar power is leading at $1.4B in 84 deals• Followed by biofuels at

$976M in 44 rounds

Greentech Media Inc.

28

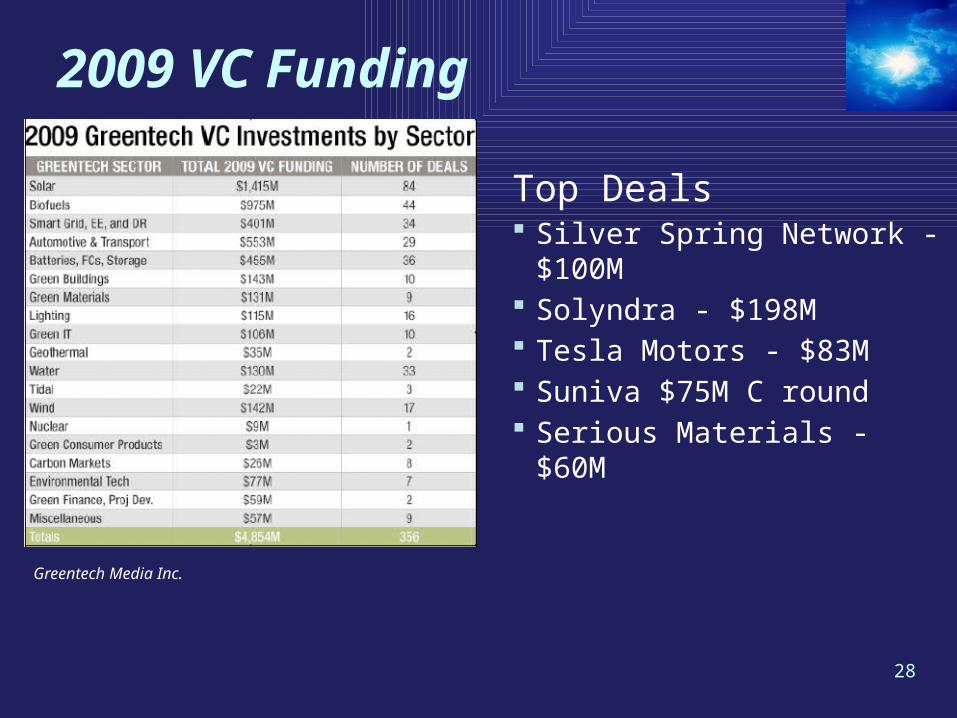

2009 VC Funding

Top Deals Silver Spring Network - $100M Solyndra - $198M Tesla Motors - $83M Suniva $75M C round Serious Materials - $60M

Greentech Media Inc.

29

Key Countries & Careers - Paritosh Government Policies Update

• US Programs Dave Fraser• Copenhagen Dinah Cheng• Global trends Paritosh Rajora

PV Technology & Roadmap Wen-Ben Chou US Market Dynamics

• Status & Trends Ranjeet Pancholy

• VCs & Funding Dinah Cheng Key Countries

• Germany Ravinder Sachdeva

• Spain Ranjeet Pancholy• China Mike Hsieh• India Ranjeet Pancholy

Career Options Steve Campbell• Solar Subgroup landings Keith Imai

Summary & coordinator Keith Imai

30

German Government to Lower Subsidies Subsidies for mature technology likely to decrease by mid

2010 Coalition suggests drastic cut by 30% in Feed-in-tariffs Four different models for subsidy reduction

• BSW (German Solar Business Association) suggests 3-5%• Solar World: Systems >1500MW, 1% reduction every 200mW• Sunpower suggested 1% reduction every 300MW• 15% drop in feed-in tariffs synchronized to production cost at

double of PV production Farmer’s Association pushing for elimination of

undeveloped area subsidies to operators of installations• First Solar uses undeveloped areas for their systems • Will push for rooftops - issue becomes cadmium on roof-tops?

31

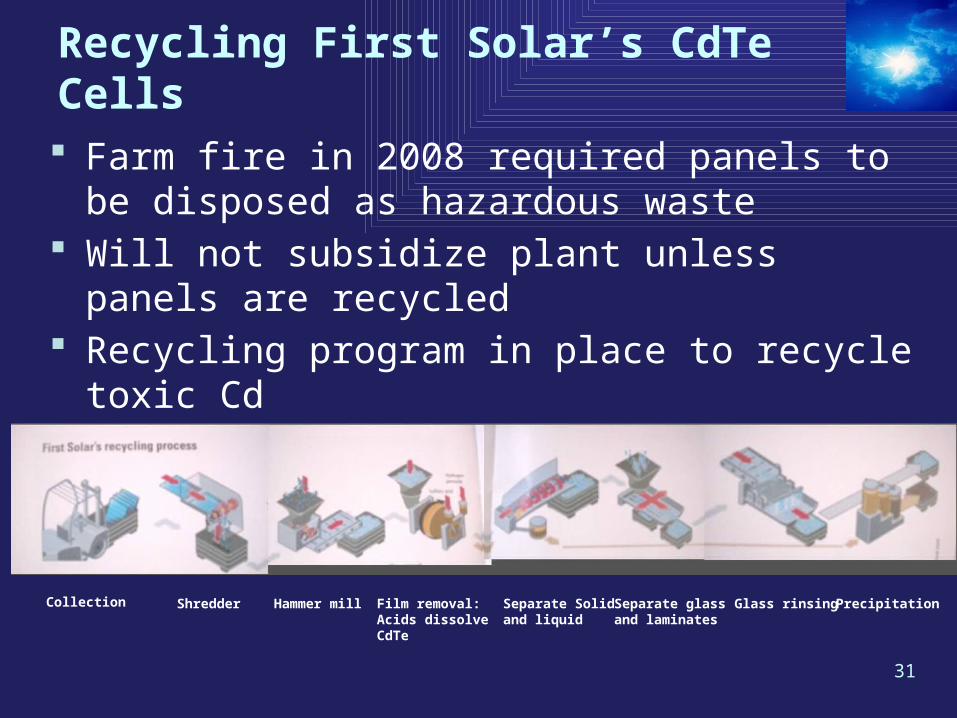

Recycling First Solar’s CdTe Cells

Farm fire in 2008 required panels to be disposed as hazardous waste

Will not subsidize plant unless panels are recycled Recycling program in place to recycle toxic Cd Recycling cost is part of production costs

Collection Shredder Hammer mill Film removal:Acids dissolveCdTe

Separate Solidand liquid

Separate glassand laminates

Glass rinsing Precipitation

32

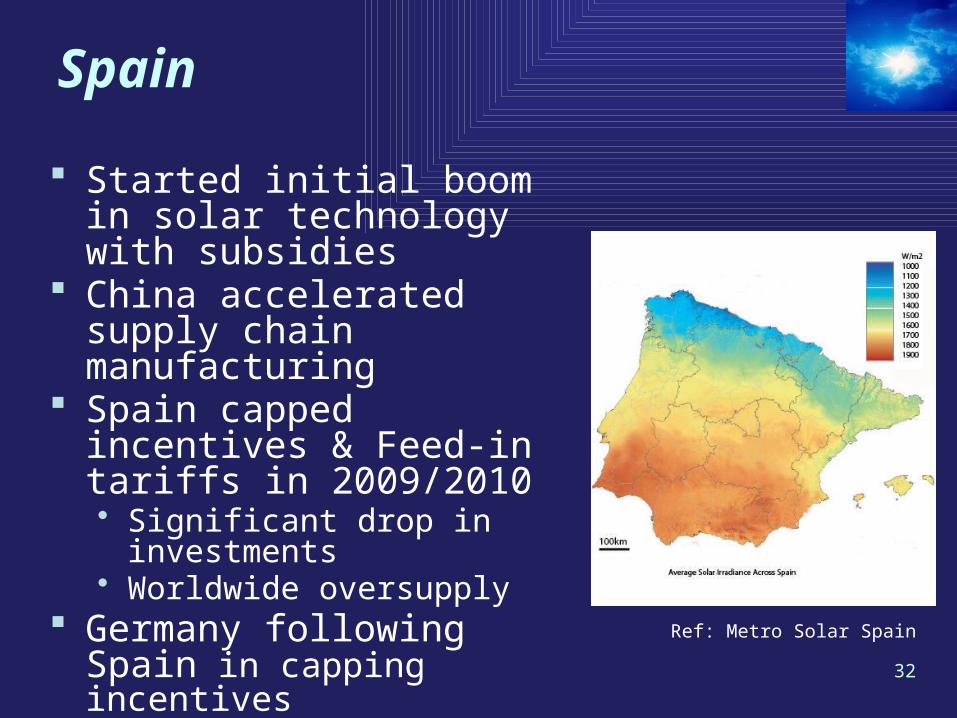

Spain

Started initial boom in solar technology with subsidies

China accelerated supply chain manufacturing

Spain capped incentives & Feed-in tariffs in 2009/2010• Significant drop in investments• Worldwide oversupply

Germany following Spain in capping incentives

Ref: Metro Solar Spain

33

China: Industry Landscape GDP growing ~10%/year Critical pollution problems 8 IPO’s since 2005 100+ solar fabs built ~49% of worldwide polysilicon volume in 2009 ~30% worldwide solar cell volume Vertical integration of solar industry

• Value chain covers polysilicon, wafers, solar cells, and solar PV modules

• Infrastructure includes solar production equipment and materials

Polysilicon production investments slowing down• Worldwide oversupply in 2009

3434

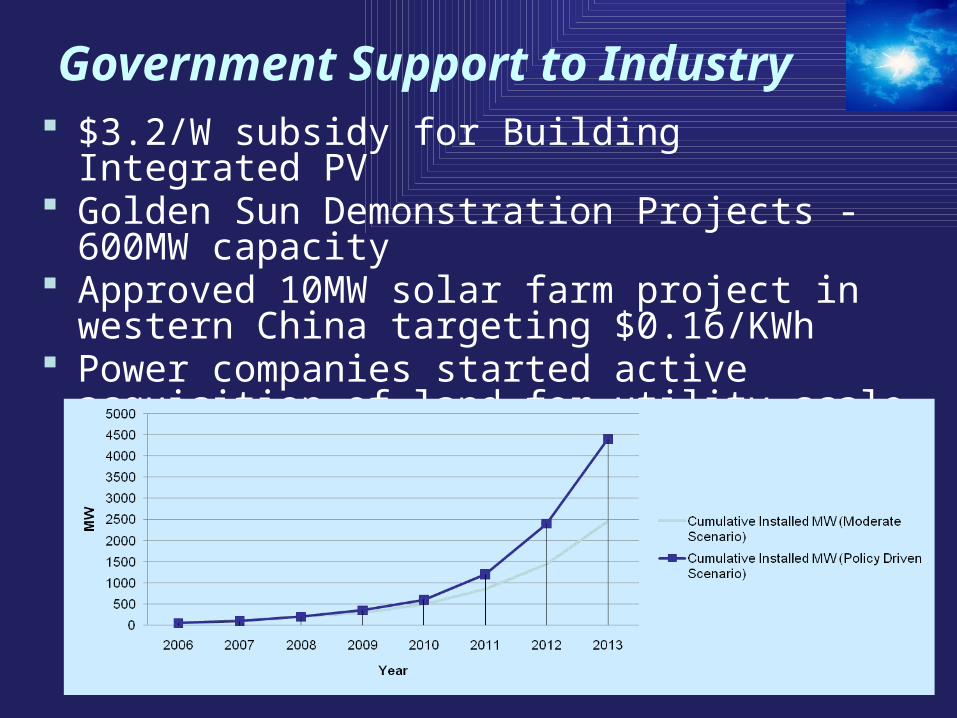

Government Support to Industry $3.2/W subsidy for Building Integrated PV Golden Sun Demonstration Projects - 600MW

capacity Approved 10MW solar farm project in western

China targeting $0.16/KWh Power companies started active acquisition of land

for utility scale solar farms in 2009

35

China: New Energy Stimulus Plan

Establish 15% renewable energy by 2020 Reduce carbon emission 40-45% per GDP from 2005

level by 2020 Increase installed solar power capacity from 100MW in

2009 to 20GW by 2020 • ~62% compound annual growth rate (CAGR)

Government to invest ~$450B in New Energy Industry• Nuclear, wind and solar

Experts estimated government to ultimately invest $700B • Will attract ~$1.5T investments from public & private

sectors

36

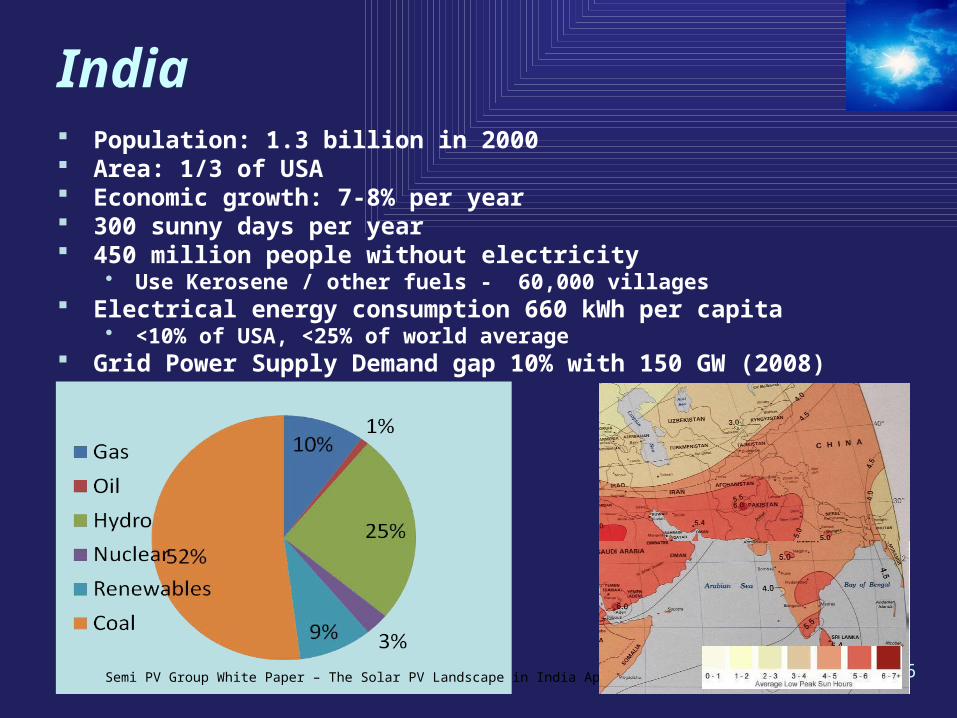

India Population: 1.3 billion in 2000 Area: 1/3 of USA Economic growth: 7-8% per year 300 sunny days per year 450 million people without electricity

• Use Kerosene / other fuels - 60,000 villages Electrical energy consumption 660 kWh per capita

• <10% of USA, <25% of world average Grid Power Supply Demand gap 10% with 150 GW (2008)

Semi PV Group White Paper – The Solar PV Landscape in India April 2009

37

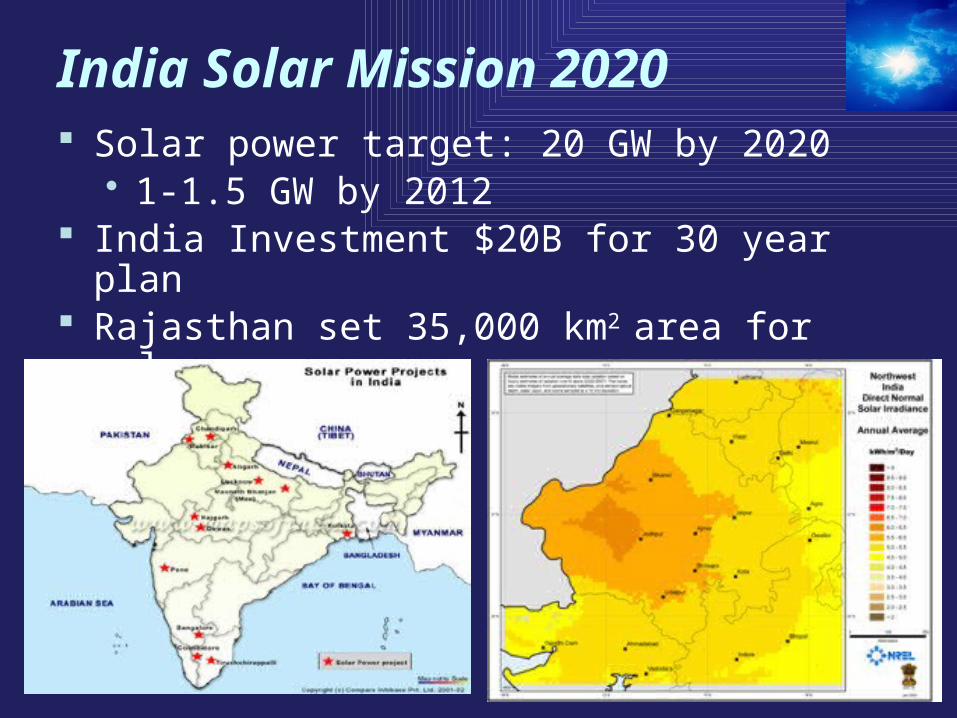

India Solar Mission 2020 Solar power target: 20 GW by 2020

• 1-1.5 GW by 2012 India Investment $20B for 30 year plan Rajasthan set 35,000 km2 area for solar

38

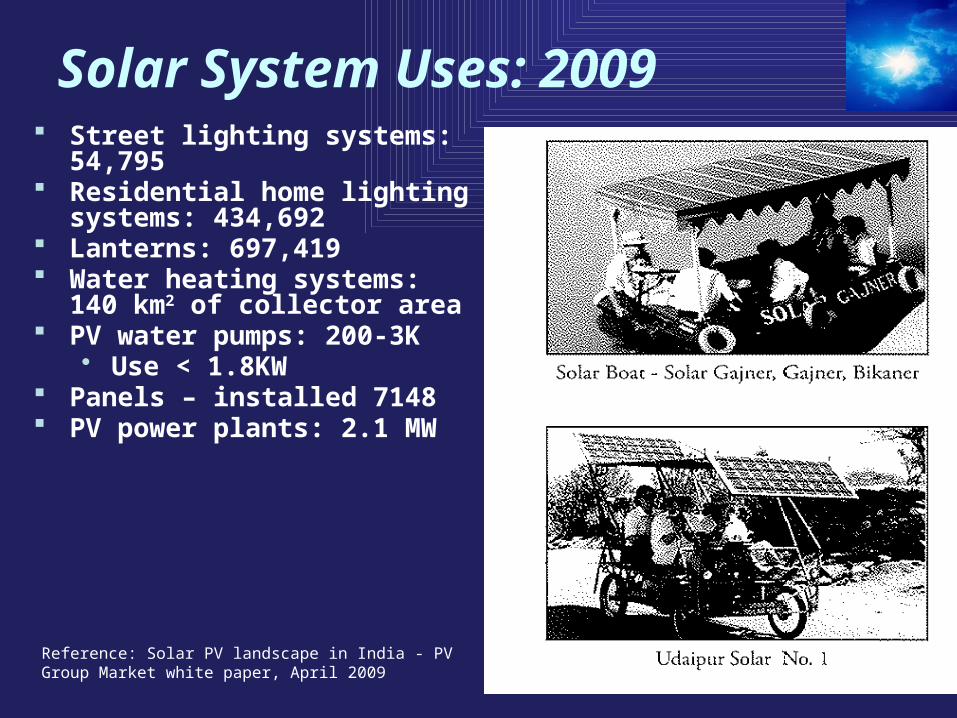

Solar System Uses: 2009 Street lighting systems: 54,795 Residential home lighting

systems: 434,692 Lanterns: 697,419 Water heating systems: 140 km2

of collector area PV water pumps: 200-3K

• Use < 1.8KW Panels – installed 7148 PV power plants: 2.1 MW

Reference: Solar PV landscape in India - PV Group Market white paper, April 2009

39

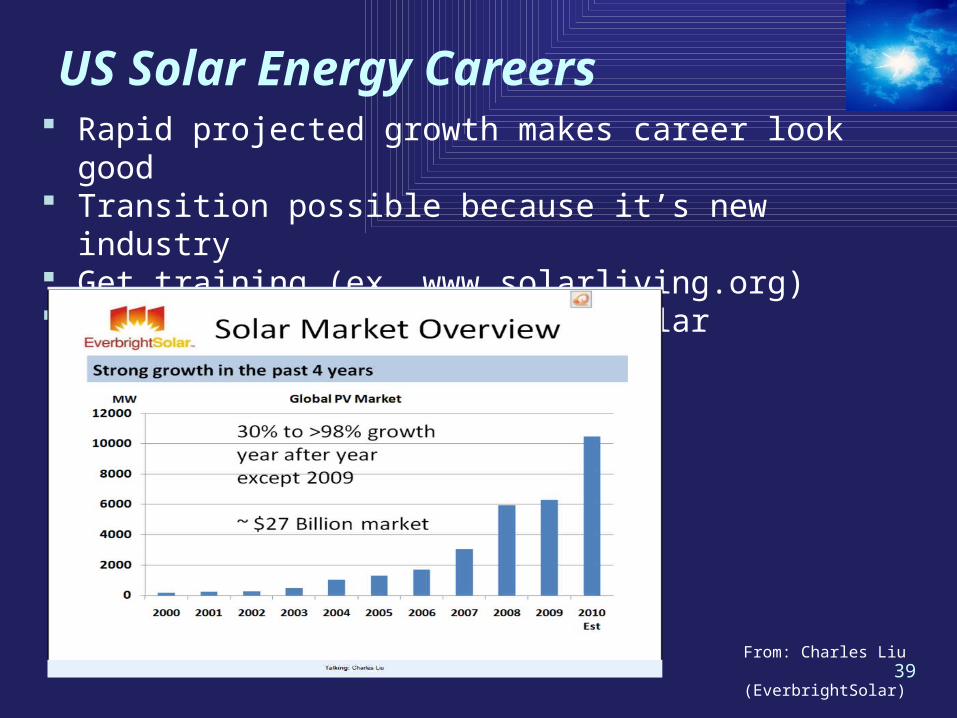

US Solar Energy Careers Rapid projected growth makes career look good Transition possible because it’s new industry Get training (ex. www.solarliving.org) Understand cost/benefits of solar (especially Sales people)

From: Charles Liu (EverbrightSolar)

40

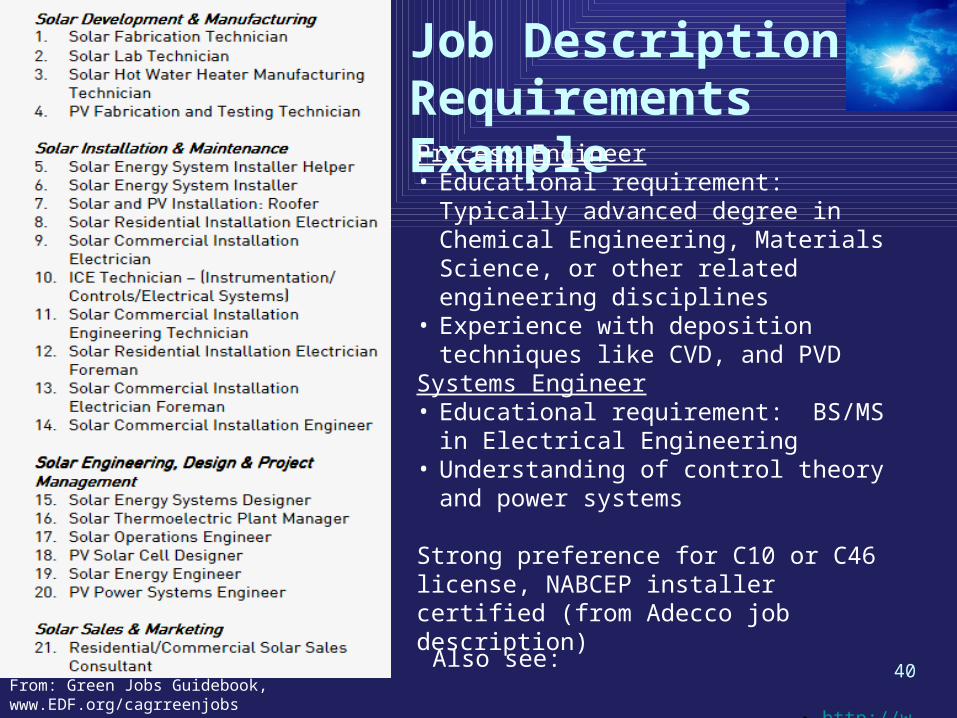

Job Description Requirements Example

From: Green Jobs Guidebook, www.EDF.org/cagrreenjobs

Process Engineer• Educational requirement: Typically advanced

degree in Chemical Engineering, Materials Science, or other related engineering disciplines

• Experience with deposition techniques like CVD, and PVD

Systems Engineer• Educational requirement: BS/MS in

Electrical Engineering• Understanding of control theory and power

systems

Strong preference for C10 or C46 license, NABCEP installer certified (from Adecco job description)

• http://www.greenforall.org/resources/green-jobs-guidebook

Also see:

41

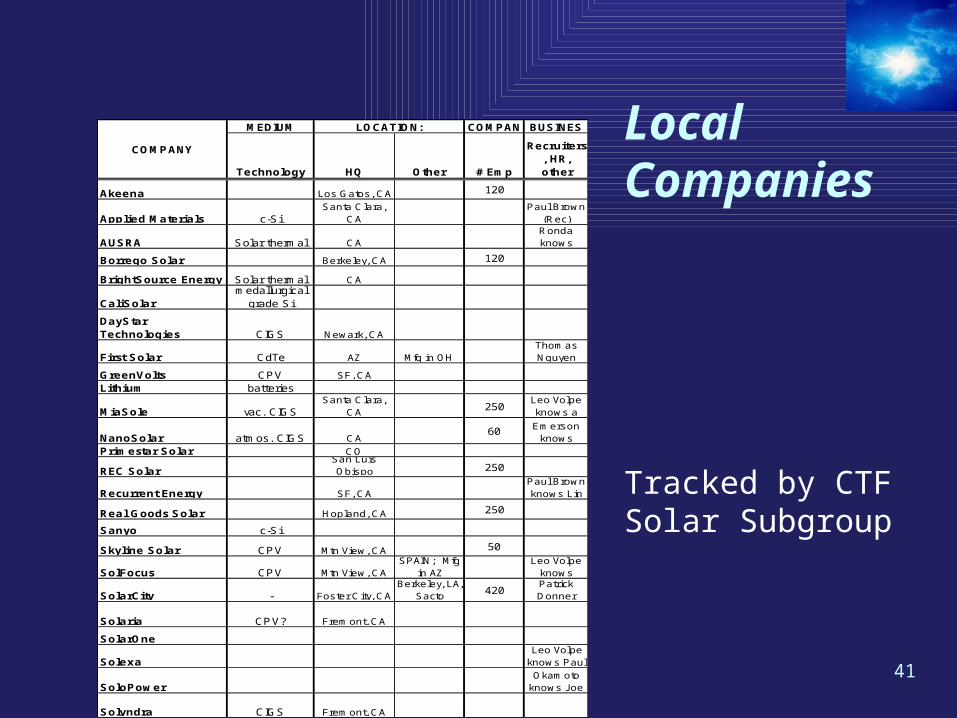

Local Companies

Tracked by CTF Solar Subgroup

MEDIUM

Technology HQ Other # Emp

Recruiters, HR, other

Akeena Los Gatos , CA 120

Applied Materials c-SiSanta Clara,

CAPaul Brown

(Rec)

AUSRA Solar thermal CARonda knows

Borrego Solar Berkeley, CA 120

BrightSource Energy Solar thermal CA

CaliSolarmedallurgical

grade Si

DayStar Technologies CIGS Newark, CA

First Solar CdTe AZ Mfg in OHThom as Nguyen

GreenVolts CPV SF, CA

Lithium batteries

MiaSole vac. CIGSSanta Clara,

CA250

Leo Volpe knows a

NanoSolar atmos. CIGS CA60

Carol Em erson

knows

Primestar Solar CO

REC SolarSan Luis Obispo 250

Recurrent Energy SF, CAPaul Brown knows Lin

Real Goods Solar Hopland, CA 250

Sanyo c-Si

Skyline Solar CPV Mtn View, CA 50

SolFocus CPV Mtn View, CASPAIN; Mfg

in AZLeo Volpe

knows

SolarCity - Fos ter City, CABerkeley, LA,

Sacto420

Patrick Donner

Solaria CPV? Frem ont, CA

SolarOne

SolexaLeo Volpe

knows Paul

SoloPower

Brian Okam oto

knows Joe

Solyndra CIGS Frem ont, CA

COMPANY

LOCATION: COMPAN BUSINES

42

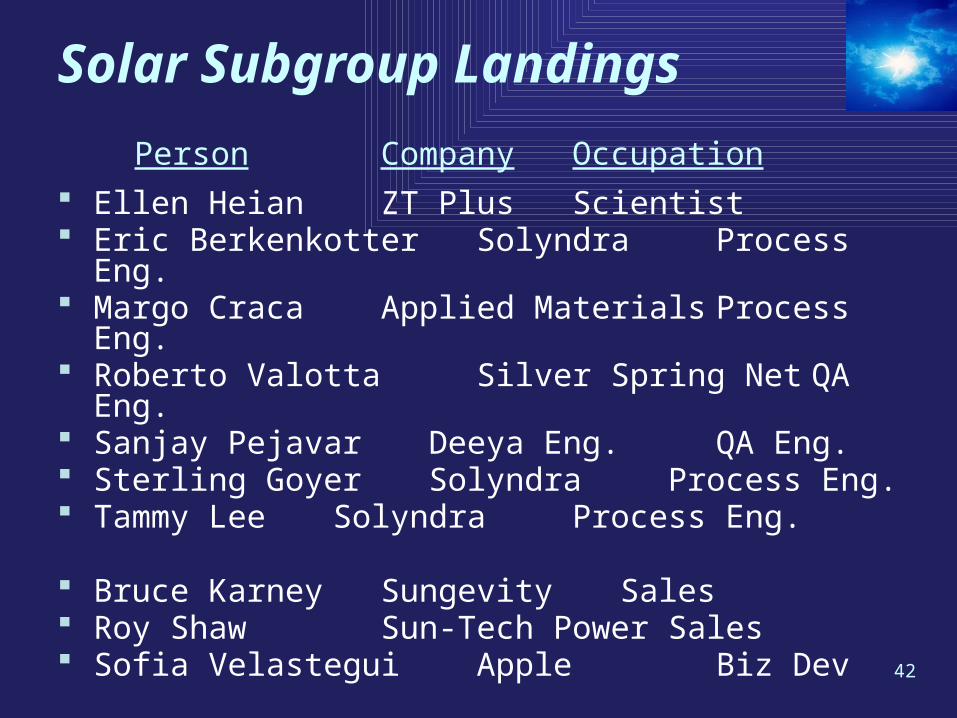

Solar Subgroup Landings

Person CompanyOccupation

Ellen Heian ZT Plus Scientist Eric Berkenkotter Solyndra Process

Eng. Margo Craca Applied Materials Process Eng. Roberto Valotta Silver Spring Net QA Eng. Sanjay Pejavar Deeya Eng. QA Eng. Sterling Goyer Solyndra Process

Eng. Tammy Lee Solyndra Process Eng.

Bruce Karney Sungevity Sales Roy Shaw Sun-Tech Power Sales Sofia Velastegui Apple Biz Dev

43

Summary

Solar industry has been & will continue to be driven by government policies

Global grid parity severely constrained by fossil fuel subsidies

USA solar VC funding of $1.4B, is largest green sector (30%)

Industry growth will continue to create jobs

44

CTF Solar Subgroup

New members always welcomed

Meets every Friday: 1:30 – 3:30pm• At Right Management

For questions, contact Co-leaders • Dinah Cheng – [email protected]• John Foggiato - [email protected]• Keith Imai – [email protected]