10th cru world aluminium conference june 13, 2005

DESCRIPTION

RUSAL’S GROWTH STRATEGY: FROM RUSSIAN TO GLOBAL ALUMINIUM BUSINESS Pavel Ulianov, Managing Director Corporate Strategy and Development. 10th CRU World Aluminium Conference June 13, 2005. A global leader, from Russia. Formed in 2000: just five years ago! - PowerPoint PPT PresentationTRANSCRIPT

RUSAL’S GROWTH STRATEGY:FROM RUSSIAN TO GLOBAL ALUMINIUM

BUSINESS

Pavel Ulianov, Managing DirectorCorporate Strategy and Development

10th CRU World Aluminium ConferenceJune 13, 2005

2

A global leader, from Russia

Formed in 2000: just five years ago!

Top 3 producer of aluminium and alloys globally

9.9% of global aluminium production

2.7 million tonnes of aluminium produced in 2004

Over US$5.4 billion in annual sales in 2004

Today, 63% of products sold directly to end-users (in 2000, 80% via middlemen traders)

Production development and expansion investments exceeded US$534 million in 2004

Over 50,000 employees

3

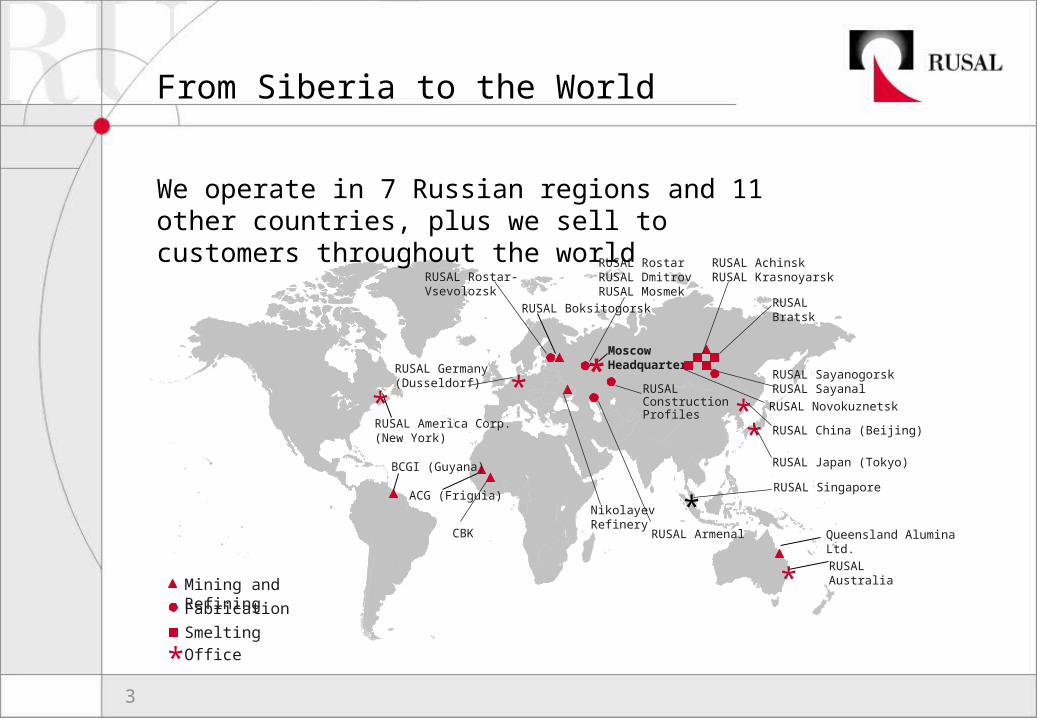

*

Nikolayev Refinery

RUSAL Bratsk

RUSAL Achinsk RUSAL Krasnoyarsk

RUSAL Novokuznetsk

CBK

RUSAL Sayanogorsk RUSAL Sayanal

RUSAL Armenal

RUSAL RostarRUSAL DmitrovRUSAL Mosmek

RUSAL Construction Profiles

RUSAL China (Beijing)RUSAL America Corp. (New York)

RUSAL Germany (Dusseldorf)

Moscow Headquarters

ACG (Friguia)

**

*

Mining and Refining

Office

Smelting

Fabrication

*

RUSAL Rostar-Vsevolozsk

*

*

RUSAL Japan (Tokyo)

RUSAL Singapore

RUSAL Boksitogorsk

*RUSAL Australia

BCGI (Guyana)

Queensland Alumina Ltd.

We operate in 7 Russian regions and 11 other countries, plus we sell to customers throughout the world

From Siberia to the World

4

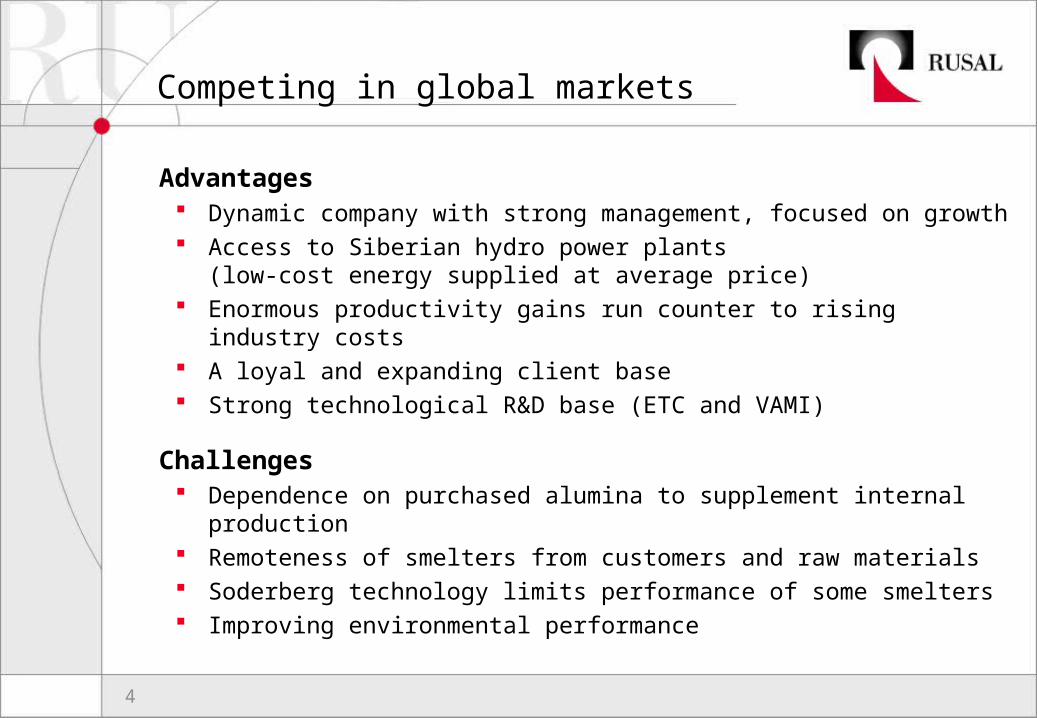

Competing in global markets

Advantages Dynamic company with strong management, focused on growth Access to Siberian hydro power plants

(low-cost energy supplied at average price) Enormous productivity gains run counter to rising industry costs A loyal and expanding client base Strong technological R&D base (ETC and VAMI)

Challenges Dependence on purchased alumina to supplement internal production Remoteness of smelters from customers and raw materials Soderberg technology limits performance of some smelters Improving environmental performance

5

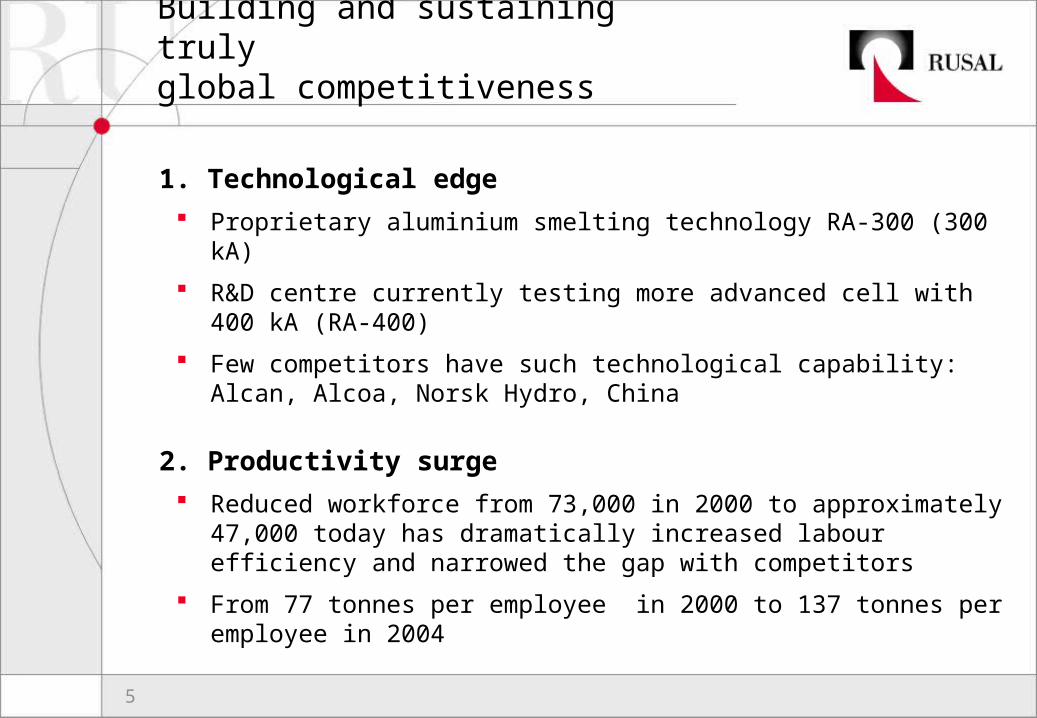

Building and sustaining truly global competitiveness

1. Technological edge

Proprietary aluminium smelting technology RA-300 (300 kA)

R&D centre currently testing more advanced cell with 400 kA (RA-400)

Few competitors have such technological capability: Alcan, Alcoa, Norsk Hydro, China

2. Productivity surge

Reduced workforce from 73,000 in 2000 to approximately 47,000 today has dramatically increased labour efficiency and narrowed the gap with competitors

From 77 tonnes per employee in 2000 to 137 tonnes per employee in 2004

6

Building and sustaining truly global competitiveness

3. Adding value

Value added product sales (alloys, billets etc) grown from around 15% in 2000 to roughly 40% today

Ambitious but realistic target to raise this share to 50% by 2013

Agreement with Alcoa allows RUSAL to focus on key businesses

4. Customer focus

Sales to global traders dropped from 80% to just 15% of total volume

Since 2000 new sales offices established in US, Germany, Japan and Singapore

Smelter distance not a barrier to improved customer service

7

Dynamic growth in aluminium smelting

Production grown by 49% (from 1.8 to 2.7 million tonnes)

Of which Creep/efficiency: ~200 ktM&A: ~700 kt Bratsk: ~150 kt Krasnoyarsk ~240 kt Novokuznetsk ~310 kt

8

Dynamic growth in alumina refining

Increased by 2.6 million tonnes or 217% to 3.8 million tonnes

From 7th to 5th position in global league table

Self sufficiency grown from 35% to over 70%Of which Creep/efficiency: 200 ktM&A: 2,400 kt Nikolaev 460 kt Achinsk 350 kt Friguia 770 kt Boxitogorsk 50 kt 20% of QAL 770 kt

9

Achieving our vision

To become the world’s largest and most profitable aluminium producer by 2013, RUSAL will:

Grow aluminium production to 5 million tonnes per year

Grow alumina production to 8 million tonnes per year

Raise alloy production to 50% of overall out-put

Position RUSAL as one of the world’s lowest-cost capex-per-tonne producers

Double current labour productivity

Enhance our employer of choice status(quality work environment and competitive salary)

10

A clear strategy for delivery: alumina

Development plan for alumina capacity to 2013

11

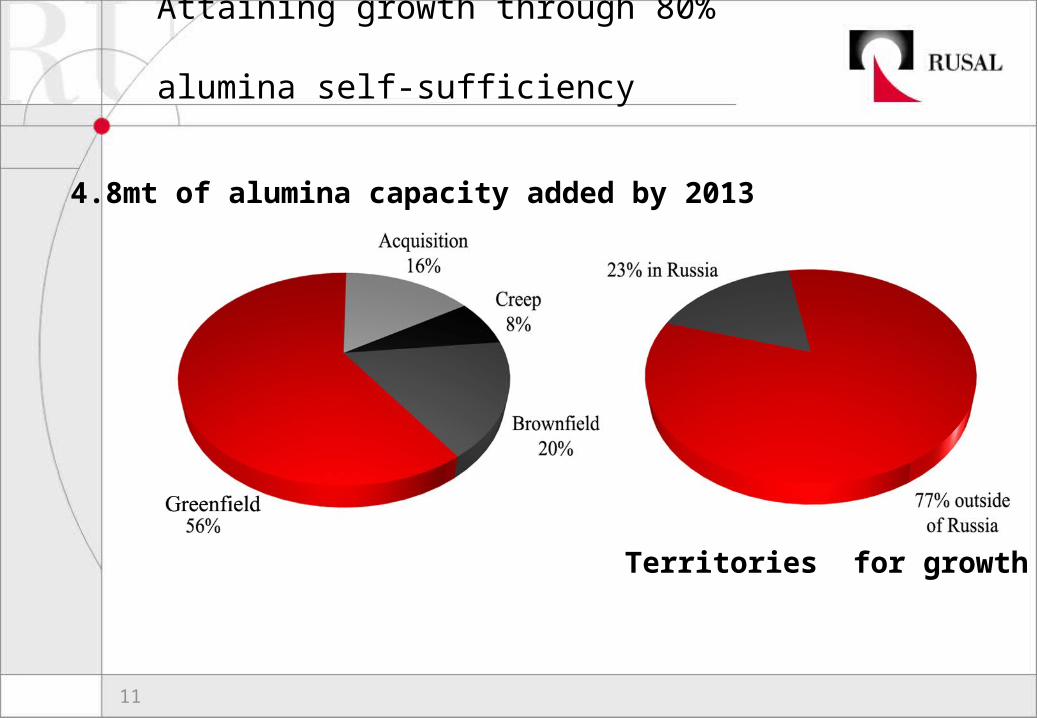

Attaining growth through 80% alumina self-sufficiency

4.8mt of alumina capacity added by 2013

Territories for growth

12

A clear strategy for delivery:aluminium

Development plan for aluminium capacity to 2013

13

Attaining aluminium growth

Greenfield projects should account for 81% of the growth

Khakassky shown as the only brownfield – 13% of growth

All smelters should add 4% to capacity through creep

Current plan assumes only 9% of growth outside Russian Federation

2.3 mt of aluminium capacity added by 2013

14

Power projects to bolster growth

Security of power supply and pricing is an issue for the industry

Rusal’s power advantage lies in Russia and former republics

Rusal is involved in power projects for 44% of its greenfield smelter capacity

Smelter fuel sources

15

Leveraging opportunitiesin Russia: Komi Project

Highlights Komi region start-up planned by 2008 Bauxite reserves JORC 190 mt. Annual volume 1,400 kt RUSAL equity share 700kt RUSAL acquired 50% in the project from its current promoter, SUAL SUAL and RUSAL will jointly manage the construction and the new

assets under a shareholder agreement SUAL will also sell 500 to 700 kt of alumina to RUSAL

Rationale Reduces alumina transport cost for RUSAL Reduces dependence on the spot alumina market for RUSAL IFC/EBRD involvement – provides international recognition Government support – positive for both companies

16

Investing in World Class assets

largest alumina refinery in the world

producing 3.85 million tonnes p.a.

a joint venture between RUSAL (20%), Comalco (38.6%) and Alcan (41.4%)

largest ever Russian investment into Australia

On 1 April 2005, RUSAL acquired 20% shareholding in Queensland Alumina Limited (QAL)

17

QAL: a bridge to the future

Increases RUSAL’s alumina supply:

RUSAL’s equity alumina production increases from 3.3 Mt to approximately 4.1Mt (+24%)

RUSAL’s share of QAL production (770Kt) currently meets 15% of RUSAL’s Siberian smelter needs

QAL has significant expansion potential to over 5Mt p.a.

QAL owners will continue to evaluate expansion options for the refinery

18

Priority issues for next 10 years

Efficient greenfield construction• lower capex, capital control, deliver on time and to budget

Development of improved (operationally and capex wise) technologies, for example RA 400

Raise capacity creep • increase current efficiency at current smelters

Active value adding M&A activity with prudent assumptions

Continue to monitor and control costs (especially in alumina)

Improve internal processes and risk management procedures to enable controlled and orderly growth

19

Instinct for Growth

www.rusal.com

Phone: +7095-720-5170

Fax: +7095-728-4912