1 welcome tax deferred 1031 real property exchanges

TRANSCRIPT

1

Welcome

Tax Deferred 1031 Real Property Exchanges

2

As a courtesy to others. . .

Please turn off phones and pagers

3

Course Goal

Recognize and evaluate when a 1031 tax-deferred exchangecould be advantageous

Explain the tax saving benefits

Work with the client and a team of experts to structure the transaction

4

Objectives

Gain an understanding of how the rules governing 1031 tax-deferred real property exchanges are applied and how transactions are put together

Explain the tax deferral benefits

of a 1031 exchange

5

Objectives

Recognize and evaluate situations in which a 1031 tax deferred exchange could be to the client’s advantage

Involve and work with intermediaries and other experts to structure the transaction

6

Day One

The Fundamentals

• Safe Harbors and Intermediaries

7

Day Two . . .

Practicum – Case Studies

Putting the Deal Together

Completion Exam

8

Two Positive Economic Outcomes . . .

Deferral of capital gain taxes

Preservation of equity

9

When……

Business reasons should always be the driving factor

When the potential tax liability outweighs both taxes and costs

10

Real Estate Professional’s Role . .

Help the client think through the pros and cons

Identify exchangeable properties

Interface with the team of professional advisors

11

Basic Concept . . .

Continue an investment without adverse tax consequences

Solution to the “tax-locked property” dilemma

12

Basic Concept . . .V

alu

e o

f R

eal

Est

ate

Ho

ldi n

gs

Time

Purchase

Exchange

Purchase

Exchange

Sale

13

Eligibility . . .

Property must be held for investment or productive use in trade or business

- AND -

Exchanged for like-kind property

14

Business Objectives . . .

Diversify or consolidate

Business needs

Financial strategy Estate planning

Change of lifestyle Avoid cost recapture

Relocation (depreciation)

15

Advantages . . .

Capital gains tax deferred

Heirs receive a stepped-up basis and tax on accumulated capital gain is forgiven

Tax-locked property is freed up

Money available for reinvestment instead of taxes

16

Disadvantages . . .

Future tax rates could be higher

Carryover of basis to replacement property

Complex and expensive transactions

Losses cannot be recognized

Proceeds must be reinvested in real estate

Time limits must be strictly adhered to

17

Capital Gains & Income Tax Top Rates . . .

18

Four Basic Rules . . .

1. Property must be held for investment

or productive use in trade or business

2. Like kind property must be exchanged for like kind

3. Replacement properties must be identified within 45 days

4. Exchange must be completed within 180 days or tax due date

19

Rule 1 . . . Held for investment or productive use in trade or business

Personal residences cannot be exchanged

Classification:

relinquished property when transferred

replacement property when received

If owner occupies a unit as a personal residence, the rental portion can be an exchange, personal use portion receives

capital gain tax treatment

20

Rule 1 . . . Held for investment or productive use in trade or business

Vacation Properties. . .

Exchanges can be problematic if any personal use of it–hard to document occupancy

Considered personal residence if owner occupied more than (greater of) 14

days, or 10% of the total days rented

21

Rule 1 . . . Held for investment or productive use in trade or business

Dealer property specifically excluded for

1031 exchange

Dealer property: primarily for sale in

ordinary course of business

Real estate brokers/agents are not

automatically dealers

22

Qualified property determined by owner’s intent . . .

Not Qualified Qualified

Home

Sweet

Home Personal Residence

For

Sale Dealer Property

Keep

OutVacant Land

(1221) & Investment

Property

For

Rent

Used in Trade or Business

(1231)

23

Rule 1 . . . Held for investment or productive use in trade or business

Unqualified Property . . . Personal residence

Dealer property

Stock, bonds, notes

Choses in action

Certificates of trust or beneficial interests

Securities or evidences of indebtedness

Interests in a partnership

24

Rule 2 . . . Like kind exchanged for like kind

All real estate held for investment or productive use in trade or business is like-kind

Property included in exchange that is not like-kind is taxable boot

Property located outside the U. S. (50 states & DC) not like kind

Exception, U.S. Virgin Islands

25

Rule 2 . . . Like kind exchanged for like kind

Real Estate Trade or Business,

Investment

$ Personal Property

Like Kind Exchange

26

Rule 3 . . . 45 Days to Identify Replacement Property

Identification period starts on the day

that the title to the relinquished property

is transferred

If multiple properties relinquished, date

of first transfer starts 45-day period

27

Rule 4 . . . 180 days or by tax due date to complete exchange

The replacement property must be

transferred before the EARLIER of 180

days after the date of transfer of the

relinquished property, OR the due date,

including extensions, of the tax return for

the tax year of the exchange

28

Rule 4 . . . 180 days or by tax due date to complete exchange .

Count the days

180 days does not equal 6 months

*

* May file for an extension, but exchange

must be completed with 180 days.

29

Foreign Taxpayers

Foreign Investment in Real Property Tax Act

of 1980 (FIRPTA)

Applies when the transferor (seller) is a non-U.S. taxpayer (individual or organization) and the property is a U.S. real property interest (USRPI).

Withholding agent (may be the real estate agent)

must withhold 10% of the amount realized (not gain)

and remit the it to the IRS within 20 days oftransaction.

30

Taxpayer Identification Number (TIN)

For an individual who cannot or does not qualify to receive a Social Security number.

Non-U.S. persons must provide a TIN when they buy or sell U.S. real property.

31

Boot in 1031 Exchanges . . .

Cash or unlike property received in the

exchange

Taxable gain

Fair market value is recognized

32

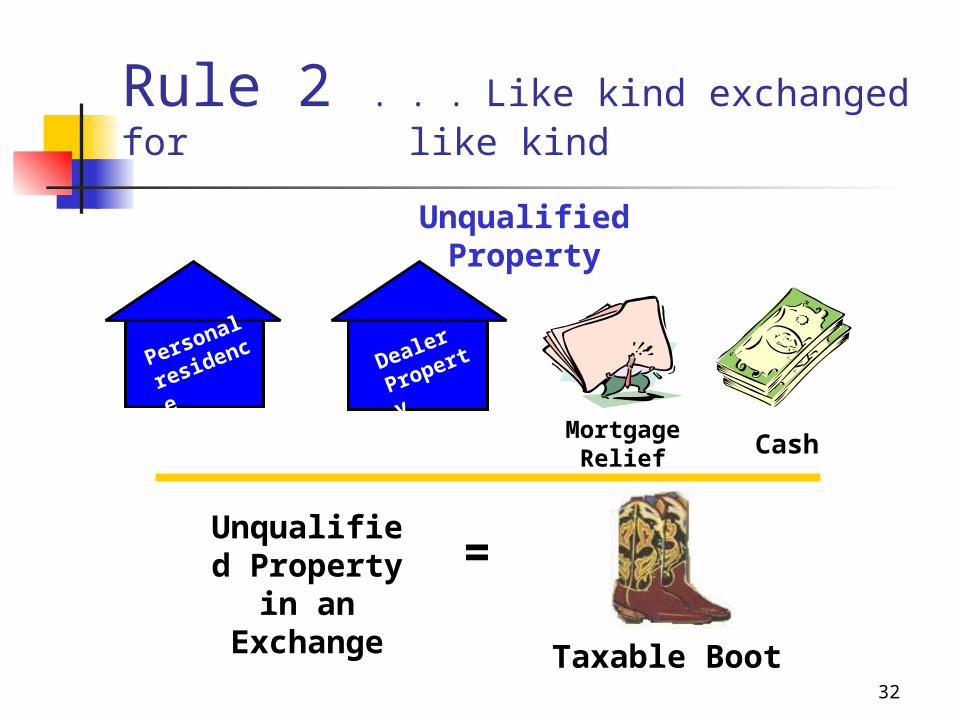

Rule 2 . . . Like kind exchanged for like kind

Unqualified Property

Personal

residenceDealer

Property

Mortgage Relief Cash

Unqualified Property in

an Exchange

=

Taxable Boot

33

Boot in 1031 Exchanges . . .

Compare the fair market value of boot

with the gain that would result from selling

the property

Taxable gain is the lesser of these two

amounts

34

Boot in 1031 Exchanges . . .

Example 2.1. . .Real estate with an adjusted basis of $30,000 is exchanged for other real estate with a fair market value of $100,000, plus $35,000 boot.

Total consideration received

$135,000

Less - Adjusted basis $30,000

Total realized gain $105,000 GAIN

Total boot received $35,000

Taxable gain is the smaller of the two

$35,000

35

Boot in 1031 Exchanges . . .

If either party assumes any of

debts or liabilities of the other as part

of the exchange, the amount of

liability is treated as cash boot

36

Boot in 1031 Exchanges . . .

Example 2.2. . . Allen exchanged real

estate with an adjusted basis of $30,000

for other real estate with a fair market

value of $100,000. In addition, he received

$35,000 cash and the other party assumed

a mortgage of $25,000.

37

Boot in 1031 Exchanges . . .

Step 1 - Total Gain Realized

FMV of like-kind property Allen received $100,000

Cash boot received $35,000

Mortgage assumed by other party $25,000

Total consideration Allen received $160,000

Less basis of property given up $30,000

Total gain realized $130,000

Step 2 - Total Boot Received

Mortgage assumed by other party$25,000

Cash received $35,000

Total boot received $60,000

Taxable gain is lesser amount . . . $60,000

38

Boot in 1031 Exchanges . . .

Netting the Liabilities . . .

Mortgage on relinquished property is boot received

Mortgage assumed may be offset against this boot

39

Boot in 1031 Exchanges . . .

Example 2.3 . . .Christine exchanged land with a mortgage of $10,000 for land with a mortgage of $15,000. In addition, she received cash boot of $6,000. After offsetting the mortgages, she has paid $5,000 mortgage boot, but is not allowed to deduct this boot paid from the cash boot received.

Her taxable boot received is $6,000.

40

Boot in 1031 Exchanges . . .

Transaction costs reduce both recognized and realized gain on the sale side and increase basis on the purchase side

Includes: brokerage commissions and closing costs such as title policy,

escrow, and recording fees

41

Boot in 1031 Exchanges . . .

Example 2.4 . . . Dave owned property with an adjusted basis of $30,000 and exchanged it for like-kind property with a fair market value of $100,000 plus $35,000 cash. He paid a $9,000 commission to his real estate broker. Dave’s taxable gain is limited to the net boot he received—$26,000.

A "loss" is not deductible.

42

Boot in 1031 Exchanges . . .

Cash boot paid offsets boot received

Mortgage boot paid offsets mortgage boot received

Mortgage paid, if more than mortgage assumed, may not offset cash or unlike property

Other boot paid may be treated as the purchase price for non-like kind property received

Selling expenses may offset boot received or net mortgage relief if no cash or unlike property is received

Recognized gain may be offset by suspended losses

43

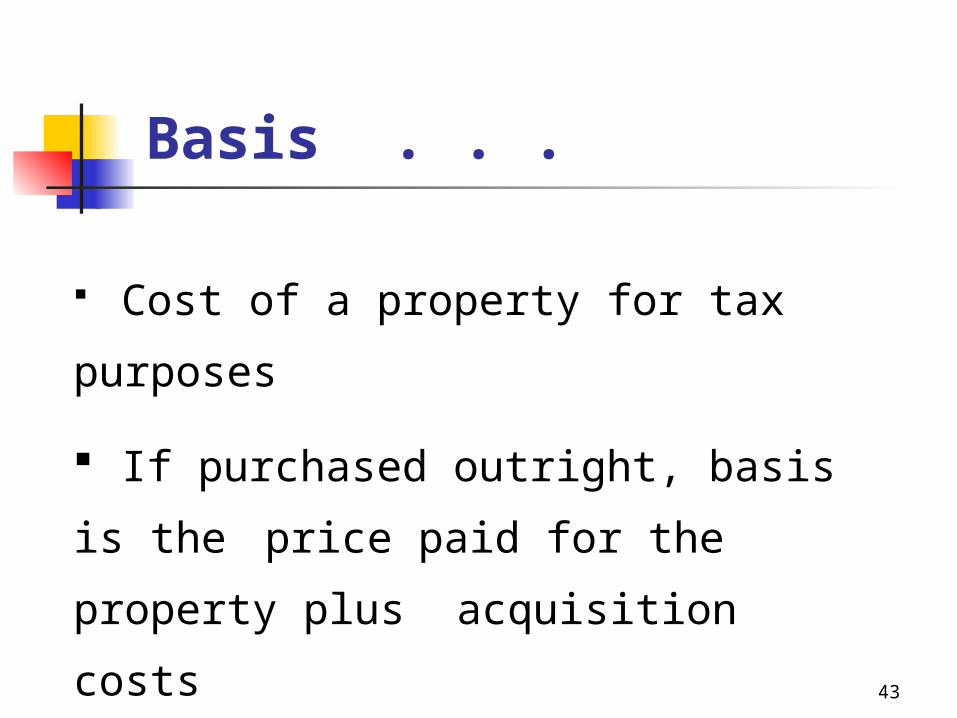

Basis . . .

Cost of a property for tax

purposes

If purchased outright, basis is

the price paid for the property plus

acquisition costs

44

Basis . . .

Capital improvements increase basis

Items that provide a tax benefit

decrease basis, e.g. cost

recovery (depreciation)

45

Basis . . .

Time 39 Years

Property Sold

Property Purchased

Market

Value

Cost Recovery

Original Basis

Capital Gain

Cost Recovery Recapture

15% tax

25% tax

Cost recovery decreases basis; recaptured at sale,

taxed at 25%. No cost recovery on land.

46

Basis . . .

Very Important . . . Basis in the relinquished property is carried over to the replacement property, regardless of the cost of either of the properties

47

Increases in Basis . . .

Cash paid in to balance equities

Liabilities/debts assumed on the replacement property

Improvements to the property

Acquisition costs

48

Decreases in Basis . . .

Depreciation

Cash or nonqualified property received

Debt relief on the relinquished property

Reimbursement from an insurance policy for casualty or theft loss

49

Equity . . .

$400,000

Mortgage

Balance

$550,000

Equity

$50,000 selling costs

Property A$1 Million

$1,450,000 New

Mortgage*

$550,000 Equity

Property B$2 Million

Transfe

r of

Equity

* Could finance $1.5 Million and take out $50,000 cash (taxable).

Relinquished Property

Replacement Property

50

Basis . . .

$500,000

adjusted basis

$450,000

deferred gain

$50,000 selling costs

Property A$1 Million

$1,550,000

substitute basis

$450,000

deferred gain

Property B$2 Million

Transfe

r of

Basis

Relinquished Property

Replacement Property

51

Exchange with Installment . . .

The installment sale gross profit

(recognized gain) is reduced by

gain not recognized in the

exchange

52

Exchange with Installment . . .

Example 2.5 . . . Frank owned, free and clear, an

investment property with a FMV of $100,000 and a basis

of $30,000. If he made a cash sale, he would be taxed on

$70,000. Frank decided to make a like-kind exchange for

an investment property owned by George. The FMV of

George’s property is $75,000. Frank receives George’s

property in the exchange and agrees to accept an

installment note for $25,000 to balance the equities.

Frank receives no payments of principal in the year of

sale.

53

Exchange with Installment . . .

Example . . . Frank’s gross profit percentage is 100%—

the gross profit of $25,000 divided by contract price of

$25,000. Since he did not collect any payments in the

year of sale, he has no recognized gain in the year of the

exchange.

Each year following, 100% of the principal collected that

year will be recognized as taxable capital gain

54

Identifying Properties . . .

No limit on the number/value of

properties to be relinquished

Limits on number/value of

replacement properties identified

55

Identifying Properties . . .

Three Property Rule . . .

Maximum number of replacement properties that may be identified is three without regard to the FMV of the properties

56

Identifying Properties . . .

200 Percent Rule . . .

Any number of properties if

aggregate FMV is not more than

200% of the aggregate FMV of all the

relinquished properties

57

Identifying Properties . . .

95 Percent Rule . . .

Any number of properties if by end of exchange period (180 days) aggregate value of replacement property acquired is minimum 95% of aggregate FMV of all identified property.

58

Incidental Property . . .

Not separate from larger item of property

Typically transferred together

Aggregate FMV is not more than 15% of FMV of the larger item of property

59

Identifying Properties . . .

In Writing. . .

Delivered, mailed, or telecopied (faxed), on/before end 45-day identification period to the other person involved in the exchange

Or part of written agreement signed by all parties–includes the real estate agent

60

Revoking Identification . . .

May be made at any time before

the end of the 45-day identification

period

Written document signed by

taxpayer

61

Property to be Produced . . .

Property to be Produced /Built to Suit

Qualifies as replacement property

Estimated at FMV as of the date it is expected to be received or would have if construction had been completed

62

Property to be Produced . . .

Additional production on replacement property after received does not qualify for like-kind exchange

Caution: exchange for services

63

Holding Period . . .

The holding period of the

relinquished property for capital gain

tax treatment is carried over to the

replacement property

64

Holding Period . . . Related Parties

Minimum two-year holding period . . .

If related parties involved in exchange – relinquished or replacement property

Additional reporting – Form 8824 for two more years

65

Related Parties . . .

Family members (siblings, spouse, ancestors, and lineal descendants) Corporate relationships Partnerships Trusts Estates Organizational relationships

66

Holding Period . . . Residence Received in Exchange

Minimum five-year ownership period . . .

Property received in exchange and converted to personal residence must be held 5 years in order to qualify for $250,000 exclusion of gain on sale of personal residence.

67

State Laws . . .

Examine for both the state of

the relinquished property and

replacement property

68

Documenting Intent to Exchange . . .

Listing Agreement . . . 1031

exchange

contingency if dependent on completion

of a tax-deferred exchange

Exchange Agreement . . .

Document

relationship between taxpayer &

safe

harbor

69

Documenting Intent to Exchange . . .

Sales Contract . . .notice of assignment of rights if a

qualified intermediary involved

Purchase Agreement . . . 1031 exchange contingency

establishes intent

70

Documenting Intent to Exchange . . .

Escrow Instructions . . direct how the proceeds should be received and disbursed

These documents . . . not required to be included with

filing, should be in place to prove intent

71

Reporting the Exchange . . .

IRS Forms . . .

1099-S Proceeds From Real Estate Transactions

Form 8824 Like-Kind Exchanges

Form 4797 Sales of Business Property

72

Types of Exchanges . . .

Simultaneous Exchange . . .

On the agreed day, the parties meet at the closing table to swap deeds for the properties

73

Types of Exchanges . . .

Deferred “Starker” Exchange

T.J. Starker v. United States . . . Exchanges do not have to be simultaneous to qualify

Landmark 1979 Federal Court case

74

Types of Exchanges . . .

Deferred “Starker”: Relinquished property transferred before

replacement property acquired

Reverse “Starker”: Replacement property acquired before

relinquished property transferred

75

Types of Exchanges . . .

Actual receipt . . . cash proceeds or property are in the taxpayer’s possession

Constructive receipt . . . cash proceeds or property can be

drawn or are in taxpayer’s control

76

Types of Exchanges . . .

Deferred “Starker” Exchanges . . .

Key to successful transaction – avoiding actual or constructive

receipt

Actual or constructive receipt by an agent is actual or constructive receipt by the taxpayer

77

Types of Exchanges . . .

Qualified Exchange Accommodation Arrangement (QEAA)

Qualified Exchange Accommodations Titleholder (QEAT) takes and holds title to the replacement property

“Parks” title with QEAT until replacement property identified & exchange

completed

78

Types of Exchanges . . .

Reverse Exchange . . .

Taxpayer must complete

agreement with QEAT within 5

days of accommodator acquiring

replacement property

79

Reverse Exchange Safe-Harbor Guidelines . . .

Complete within 180-days or the property held by the QEAT is deeded to the taxpayer

Identify relinquished property within 45 days

Intermediary can hold title to replacement or relinquished property

Qualified Exchange Accommodations Agreement (QEAA) completed within 5 days

80

Types of Exchanges . . .

Reverse Exchange . . .

Replacement property held in a QEAA

may not be owned by the taxpayer within

the 180-day period preceding the date of

transfer of the property to the Exchange

Accommodation Titleholder.

Rev. Proc. 2004-51

81

Types of Exchanges . . .

Delayed Closing or Deferred Exchange?

Don’t confuse

Delayed closing: relinquished property "sale" does not close until an agreed date

82

Types of Exchanges . . .

Edward(exchanger)

Susan(seller)

Central Court

Silver City

Example 2.6: Two Way Exchange

83

Types of Exchanges . . .

Three Way Exchange. . .

Solves the dilemma of a two-way swap

Why? Other owner seldom wants the offered property, but would accept another one, or prefers to sell the property and take the cash proceeds

84

Types of Exchanges . . .

Edward(exchanger)

Susan(seller)

Example 2.7Three Individual Transfers

Bob(buyer)

85

Types of Exchanges . . .

Edward(exchanger)

Susan(seller)

Example 2.8 Exchange with Purchaser

Bob(buyer)

1

2

86

Types of Exchanges . . .

Edward(exchanger)

Susan(seller)

Example 2.9Exchange with Seller

Bob(buyer)

2.1.

87

Types of Exchanges . . .

Edward(exchanger)

Susan(seller)

Example 2.10Escrow Holder as Accommodator

Bob(buyer)

Escrow

88

Types of Exchanges . . .

Edward(exchanger)

Susan(seller)

Bob(buyer)

Intermediary

Example 2.11Exchange with an

Intermediary

89

Tenants in Common . . .

Enables small investor ownership participation in premium commercial & investment property

Like-kind property for 1031 exchange

90

Tenants in Common . . .

What it is not . . . a joint venture, partnership, or limited partnership

What it is . . . each investor owns an undivided, fractional, interest

91

Tenants in Common . . .

Advantages . . .

Avoid involvement in day-to-management

Investment in high quality properties

Comply quickly with 45-day identification time limit

Exchange a specific amount of value

Upgrade and diversity a portfolio

92

Tenants in Common . . .

Advantages . . .

Sponsors (specialized firms)

research properties, package

investments, and monitor

performance

Large, institutional-grade

properties

93

Tenants in Common . . .

Caution . . .

SEC regulations bar a commission or referral fee unless the real estate professional is a licensed security dealer

Agent may be compensated for counseling services

Can be paid from funds held by the QI, not the sponsor

94

Four Safe Harbors . . .

Purpose . . . avoid actual or constructive receipt of proceeds

1. Security or guarantee arrangements

2. Qualified escrow accounts and trusts

3. Interest and growth factors

4. Qualified intermediaries

95

Four Safe Harbors . . .

Security or Guarantee Arrangements

Mortgage, deed of trust, or other security interest in property (other than cash or a cash equivalent)

Standby letter of credit

Guarantee of a third party

96

Four Safe Harbors . . .

Qualified Escrow Accounts & Trusts . . .

Escrow may not be held by the exchanger or a

related party, and the exchanger’s rights to

receive, pledge, borrow, or otherwise obtain the

benefits of the escrow account must be limited

97

Four Safe Harbors . . .

Escrow Account or trust funds may pay transactional items if. . .

Related to disposition or acquisition of property, and

Typically listed as the responsibility of a buyer or seller on the closing statement

98

Four Safe Harbors . . .

Exchanger may receive money or other property directly from another party to the transaction – not from a qualified escrow, trust, or intermediary

Why? Disqualifies safe harbor

99

Four Safe Harbors . . .

Interest and Growth Factors. . .

Interest earned while the sale proceeds are held by the QI may be paid into escrow

Received by the exchanger as earned income upon completion of transaction

100

Four Safe Harbors . . .

Qualified Intermediary. . .

A person (or company) who

facilitates the exchange by making

an agreement for the exchange of

properties

101

Four Safe Harbors . . .

Qualified Intermediary

Transfers titles to properties

Agreement with a person (other than the exchanger) to transfer relinquished property

Agreement with the replacement property owner to transfer that

property

102

Four Safe Harbors . . .

Direct deeding: intermediary acquires rights to transfer deeds to the properties

Sequential deeding: intermediary acquires deed to relinquished and replacement properties and

transfers deeds

103

Four Safe Harbors . . .

Edward(exchange

r)

Susan(seller)

Example 3.1A Direct deeding by a Qualified Intermediary

Bob(buyer)

Qualified Intermediary

104

Four Safe Harbors . . .

Example 3.1B Direct deeding by Exchanger and Seller

Edward(exchanger)

Susan(seller)

Bob(buyer)

Qualified Intermediary

$1 million$1 million property

$1 million cash

$900,000 property

$100,000$1,000,000

$900,000

105

Before After

Edward owns Central Court Apartments valued at $1,000,000

Edward owns Silver City Apartments valued at $900,000 and has $100,000 cash

Bob has $1,000,000 Cash Bob owns Central Court Apartments valued at $1,000,000

Susan owns Silver City Apartments valued at $900,000

Susan has $900,000 cash

106

Four Safe Harbors . . .

Disqualification . . .

Intermediary may not be:

Taxpayer

Related person

Agent of the taxpayer

Person related to agent of taxpayer

“Person” also means corporate

entities

107

Four Safe Harbors . . .

Disqualification . . .

Agent of the exchanger:

Employee

Attorney

Accountant

Investment banker or broker

Real estate agent or broker

Within two-year period ending on the date of the transfer of the first of the relinquished properties

108

Four Safe Harbors . . .

Disqualification . . .

Exceptions

Performance of services that are solely with respect to exchanges of real estate

Performance of routine financial, title insurance, escrow, trust services by a financial institution, title insurance company, or escrow company

109

How Are Real Estate Agents Paid? . . .

Safe harbor arrangements allow the real estate professional’s commission to be paid on behalf of the taxpayer as a “transactional item”

110

How Are Real Estate Agents Paid? . . .

Caution: When tenants-in-common ownership interest in involved in the exchange

SEC views the ownership interest as a security, bars payment of a commission or referral fee unless the real estate professional is a licensed security representative

Exchanger may compensate a real estate agent for counseling services

111

Putting It All Together . . .

Evaluating exchange situations

Assess the overall situation

Experience and comfort level

Change of mindset

Even swap or value gain?

112

Putting It All Together . . .

Finding a qualified intermediary

Member of the Federation of Exchange Accommodators

CES designation

Bonded by insurance company

Professional background, CPA? Attorney?

113

Putting It All Together . . .

Finding a qualified intermediary

Responsibility for losses

Interest on the escrow account

Accessible to your client and you

114

Putting It All Together . . .

Finding a qualified intermediary

Other experts involved

Adequate paper trail

Accustomed to type/size of transaction

Specialty

Licensed securities representative

115

Putting It All Together . . .

Watch out for…..

Complying with time limits

Lack of preparation

Negotiating for only “Plan A” property

Other obstacles that intervene

Unscrupulous parties

116

Thank You . . .

Tax Deferred 1031 Real Property Exchanges