1 learning to live in euroland the role of france and germany conference france and germany in the...

Post on 22-Dec-2015

214 views

TRANSCRIPT

1

Learning to live in EurolandThe role of France and Germany

Conference

France and Germany in the International Division of Labour

Centre Saint-Gobain for Economic Studies

Paris, 9-10 December 2004

Stefan Collignon

Professor of European Political Economy LSE

2

Learning to live in Euroland Professor Stefan Collignon

Franceallemagne as motor of European integration?

“Red lanterns” in Euroland ?

Rigid labour markets ?

An out-dated social model ?

A more complex reality

Fundamental change is the monetary system

from Bretton Woods to EMS to EMU

Adjustment to the new reality takes more than labour market reforms

3

Learning to live in Euroland Professor Stefan Collignon

Economic convergence as a precondition for political union

A remarkable degree of convergence has taken place

Germany suffers from German unification

Fiscal policy suffers from institutional deficiencies and this blocs economic growth and employment in Euroland

Unless political initiative emerges from France and Germany, 50 years of integration will perish

Economic stagnation is systemic

Collective action problem in EU25

bad policy output undermines legitimacy

But France and Germany have ideologically converged

4

Learning to live in Euroland Professor Stefan Collignon

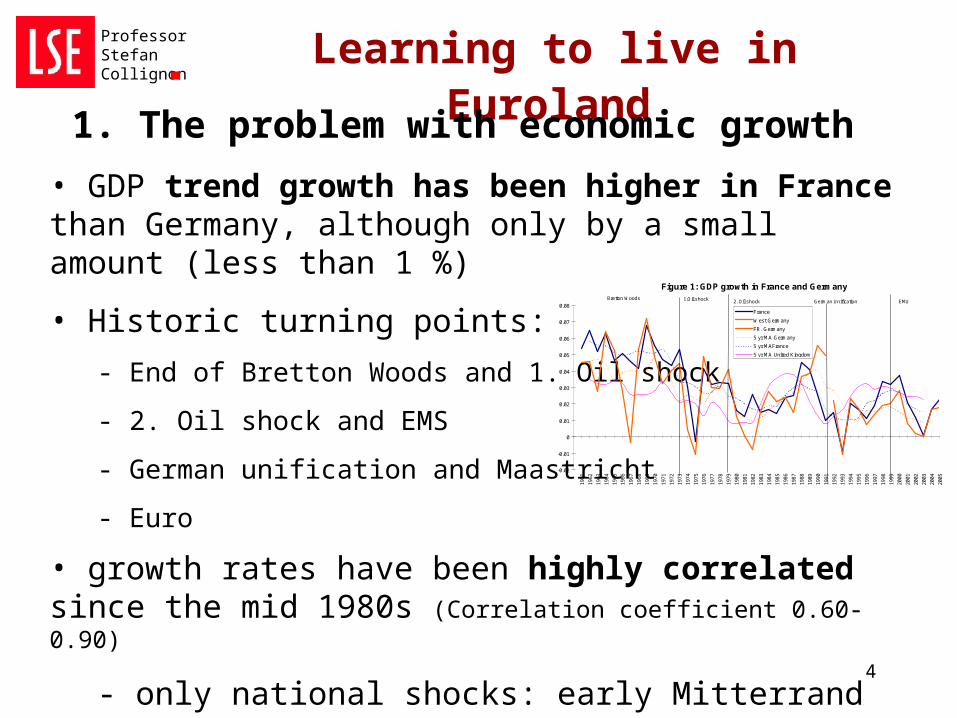

1. The problem with economic growth

• GDP trend growth has been higher in France than Germany, although only by a small amount (less than 1 %)

• Historic turning points:

- End of Bretton Woods and 1. Oil shock

- 2. Oil shock and EMS

- German unification and Maastricht

- Euro

• growth rates have been highly correlated since the mid 1980s (Correlation coefficient 0.60-0.90)

- only national shocks: early Mitterrand years and German unification

Figure 1: GDP growth in France and Germany

-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

France

West Germany

FR. Germany

5 yr MA Germany

5 yr MAFrance

5 yr MA United Kingdom

EMU2. Oil shockBretton Woods 1.Oil shock German Unification

5

Learning to live in Euroland Professor Stefan Collignon

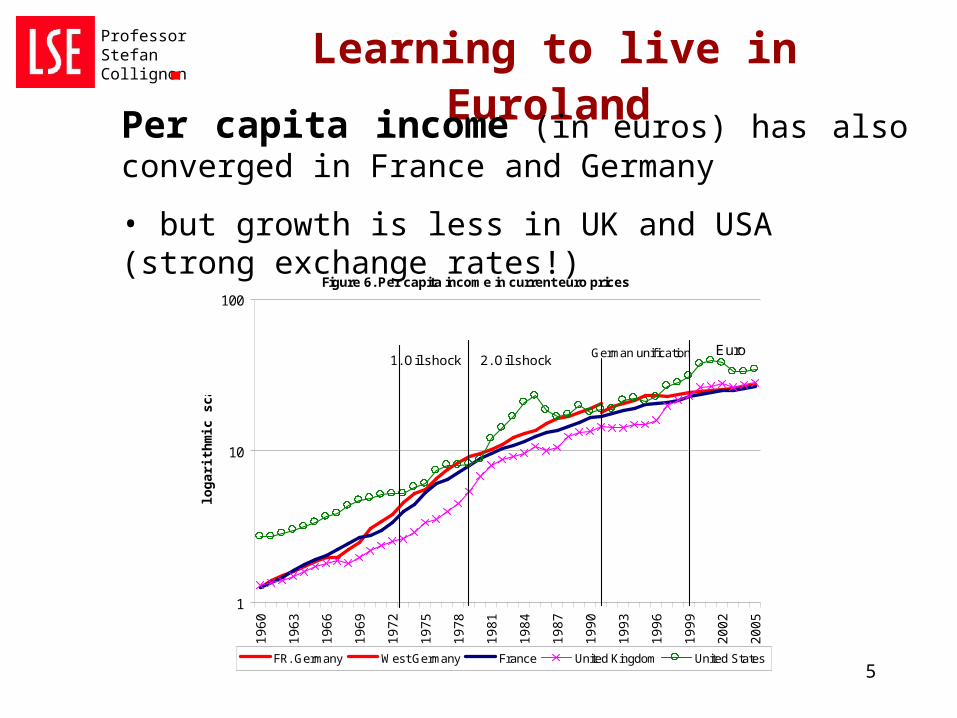

Per capita income (in euros) has also converged in France and Germany

• but growth is less in UK and USA (strong exchange rates!)

Figure 6. Per capita income in current euro prices

1

10

100

19

60

19

63

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

log

ari

thm

ic s

ca

le

FR. Germany West Germany France United Kingdom United States

1. Oil shock 2. Oil shockGerman unif ication Euro

6

Learning to live in Euroland Professor Stefan Collignon

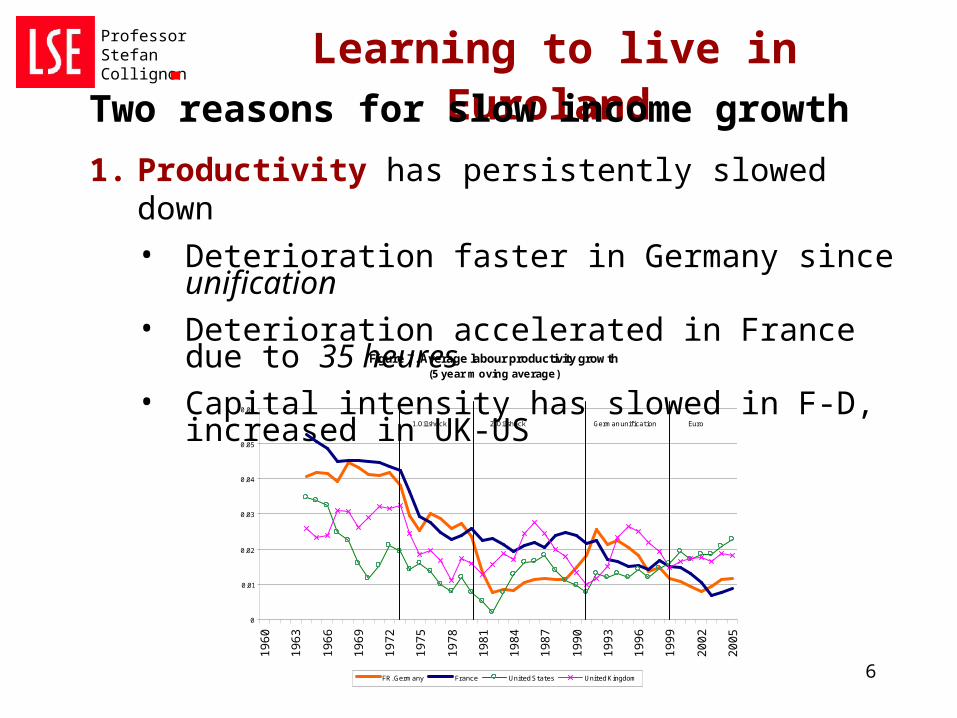

Two reasons for slow income growth

1. Productivity has persistently slowed down

• Deterioration faster in Germany since unification• Deterioration accelerated in France due to 35 heures• Capital intensity has slowed in F-D, increased in UK-US

Figure 7. Average labour productivity growth (5 year moving average)

0

0.01

0.02

0.03

0.04

0.05

0.06

19

60

19

63

19

66

19

69

19

72

19

75

19

78

19

81

19

84

19

87

19

90

19

93

19

96

19

99

20

02

20

05

FR. Germany France United States United Kingdom

1. Oil shock 2. Oil shock German unification Euro

7

Learning to live in Euroland Professor Stefan Collignon

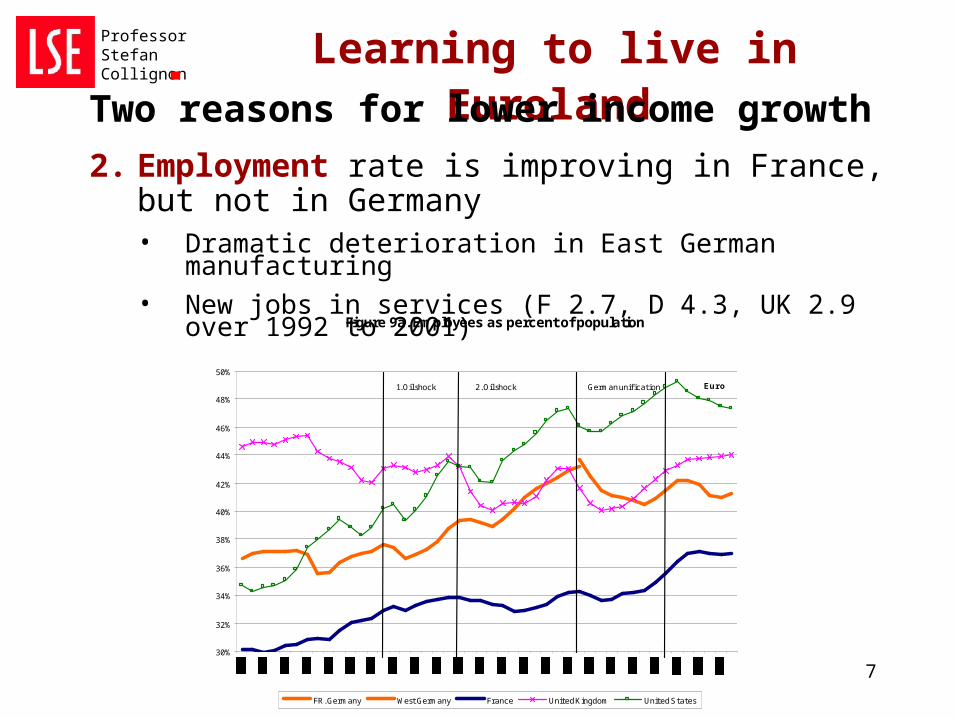

Two reasons for lower income growth

2. Employment rate is improving in France, but not in Germany• Dramatic deterioration in East German manufacturing• New jobs in services (F 2.7, D 4.3, UK 2.9 over 1992 to 2001)

Figure 9a. Employees as percent of population

30%

32%

34%

36%

38%

40%

42%

44%

46%

48%

50%

FR. Germany West Germany France United Kingdom United States

EuroGerman unification2. Oil shock 1. Oil shock

8

Learning to live in Euroland Professor Stefan Collignon

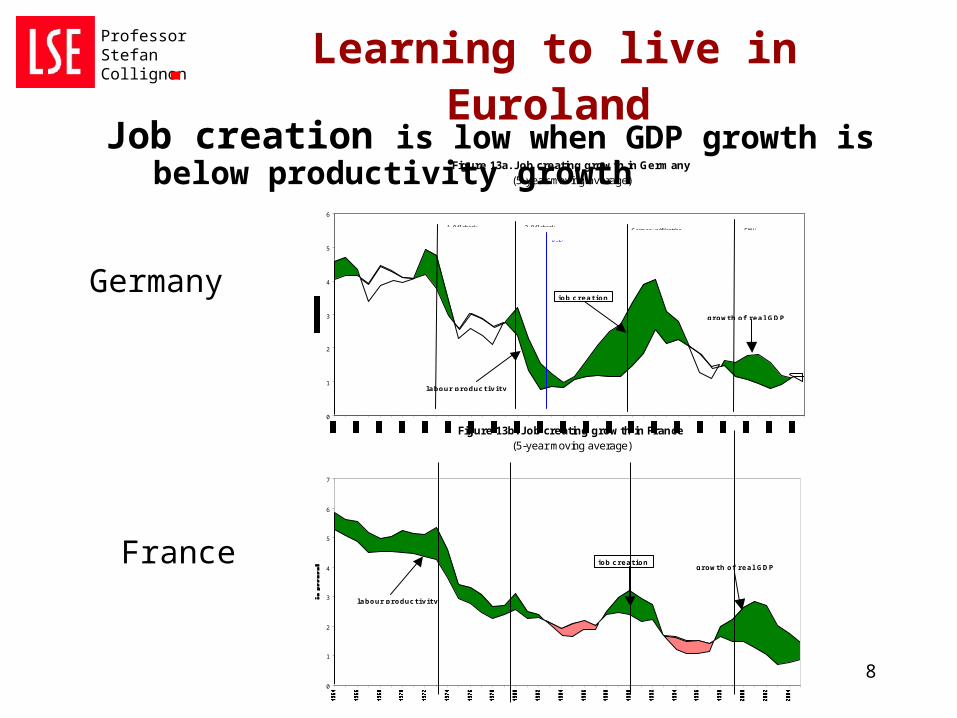

Job creation is low when GDP growth is below productivity growth Figure 13a. J ob creating growth in Germany

(5-year moving average)

0

1

2

3

4

5

6

job creation

growth of real GDP

labour productivity

EMUGerman unifi cation1. Oil shock 2. Oil shock

Kohl

Figure 13b. J ob creating growth in France(5-year moving average)

0

1

2

3

4

5

6

7

job creationgrowth of real GDP

labour productivity

Germany

France

9

Learning to live in Euroland Professor Stefan Collignon

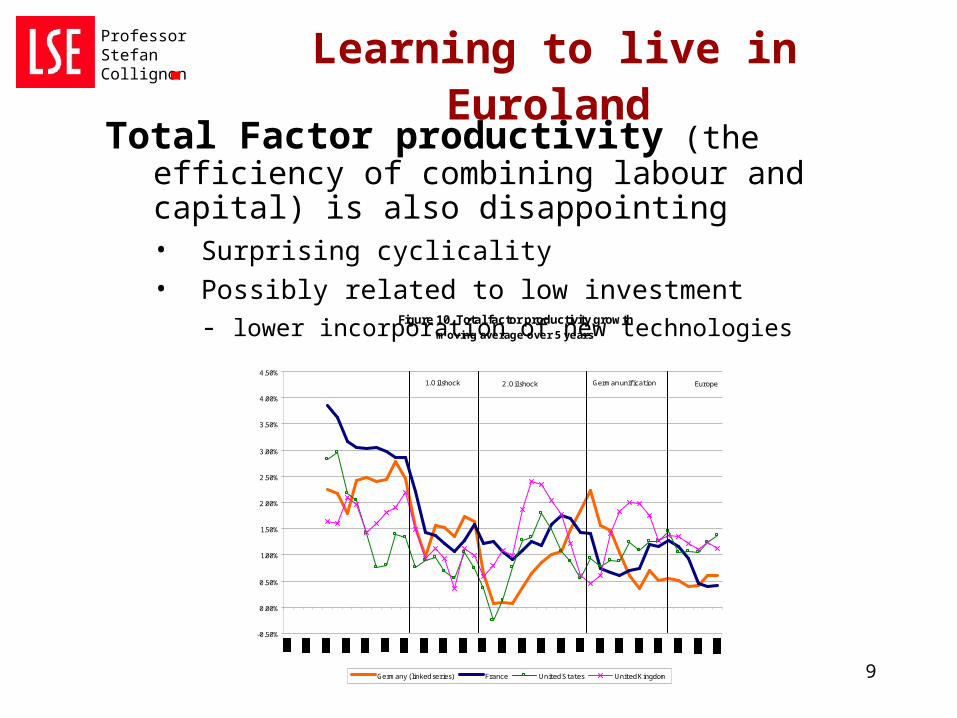

Total Factor productivity (the efficiency of combining labour and capital) is also disappointing • Surprising cyclicality• Possibly related to low investment

- lower incorporation of new technologiesFigure 10. Total factor productivity growth

moving average over 5 years

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

Germany (linked series) France United States United Kingdom

EuropeGerman unification2. Oil shock1. Oil shock

10

Learning to live in Euroland Professor Stefan Collignon

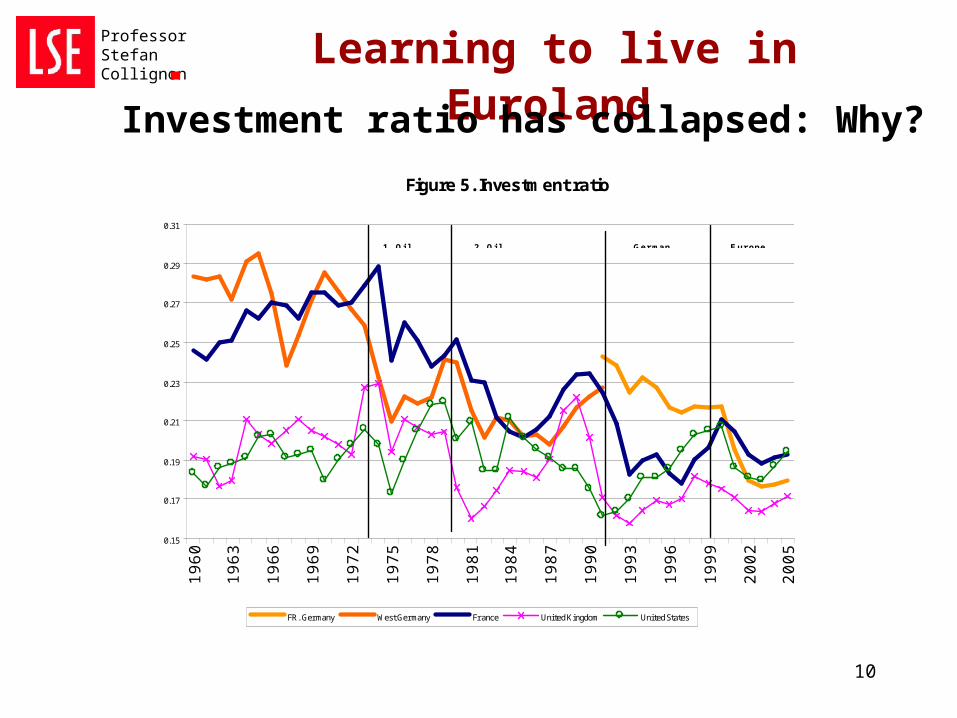

Investment ratio has collapsed: Why?

Figure 5. Investment ratio

0.15

0.17

0.19

0.21

0.23

0.25

0.27

0.29

0.31

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

FR. Germany West Germany France United Kingdom United States

1. Oi l 2. Oi l Ger man Eur ope

11

Learning to live in Euroland Professor Stefan Collignon

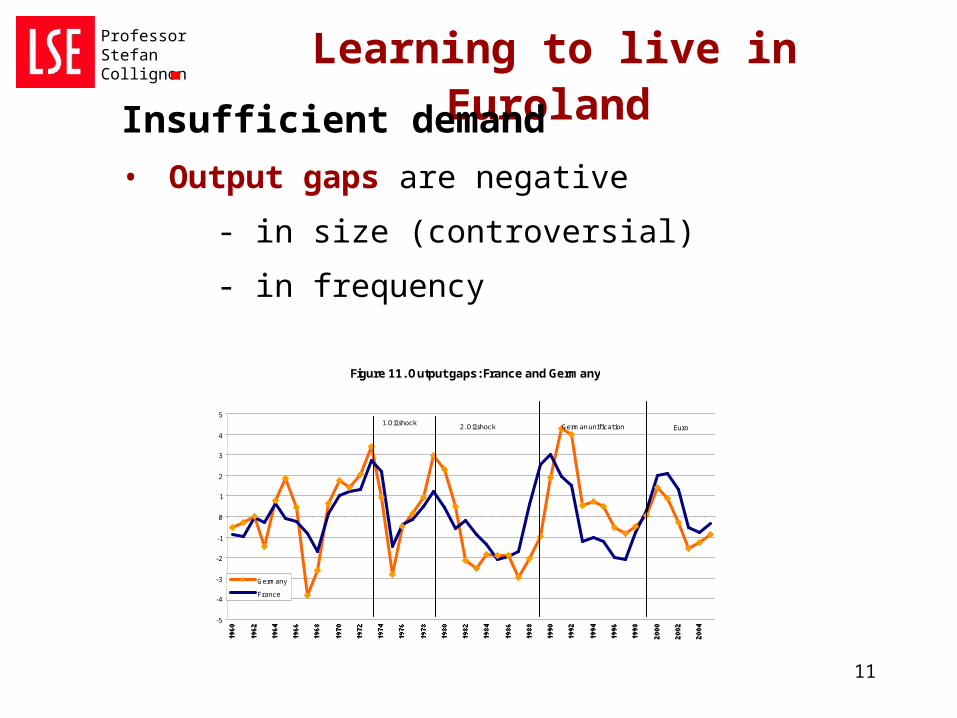

Insufficient demand

• Output gaps are negative

- in size (controversial)

- in frequency

Figure 11. Output gaps: France and Germany

-5

-4

-3

-2

-1

0

1

2

3

4

5

Germany

France

1. Oil shock 2. Oil shock German unification Euro

12

Learning to live in Euroland Professor Stefan Collignon

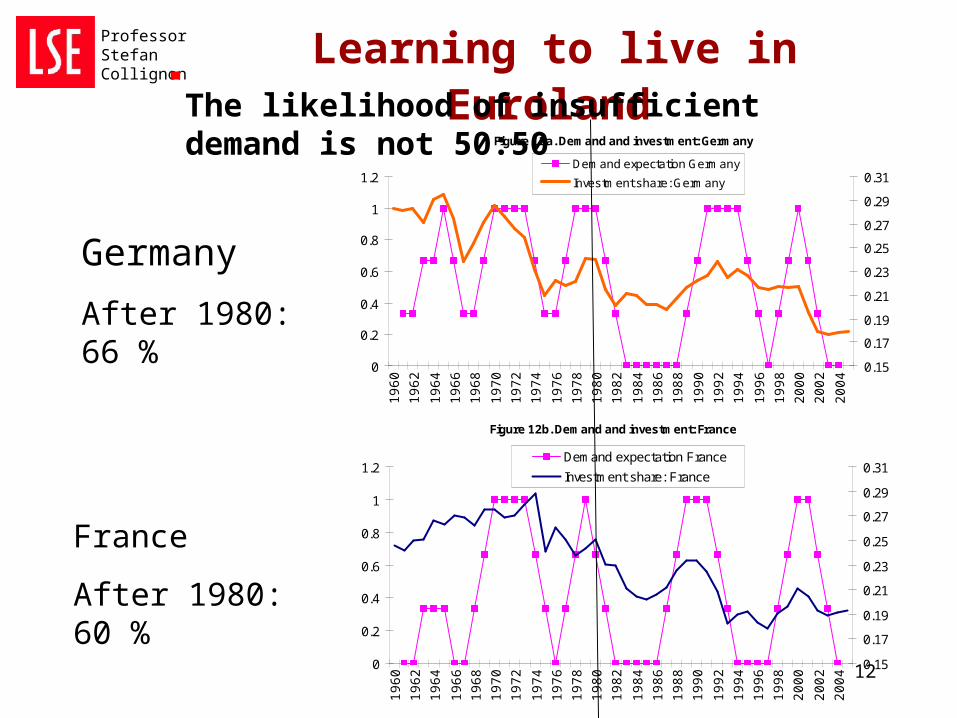

Figure 12a. Demand and investment: Germany

0

0.2

0.4

0.6

0.8

1

1.2

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

0.15

0.17

0.19

0.21

0.23

0.25

0.27

0.29

0.31Demand expectation Germany

Investment share: Germany

Figure 12b. Demand and investment: France

0

0.2

0.4

0.6

0.8

1

1.2

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

0.15

0.17

0.19

0.21

0.23

0.25

0.27

0.29

0.31Demand expectation France

Investment share: France

Germany

After 1980: 66 %

France

After 1980: 60 %

The likelihood of insufficient demand is not 50:50

13

Learning to live in Euroland Professor Stefan Collignon

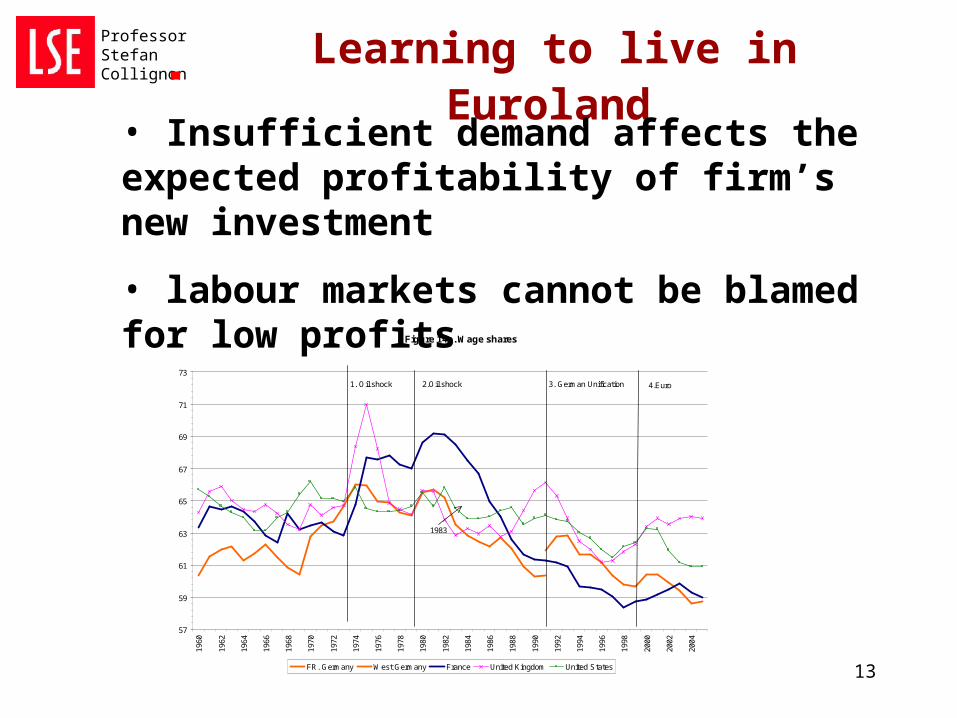

• Insufficient demand affects the expected profitability of firm’s new investment

• labour markets cannot be blamed for low profits

Figure 14a. Wage shares

57

59

61

63

65

67

69

71

73

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

FR. Germany West Germany France United Kingdom United States

1. Oil shock 2.Oil shock 3. German Unification 4.Euro

1983

14

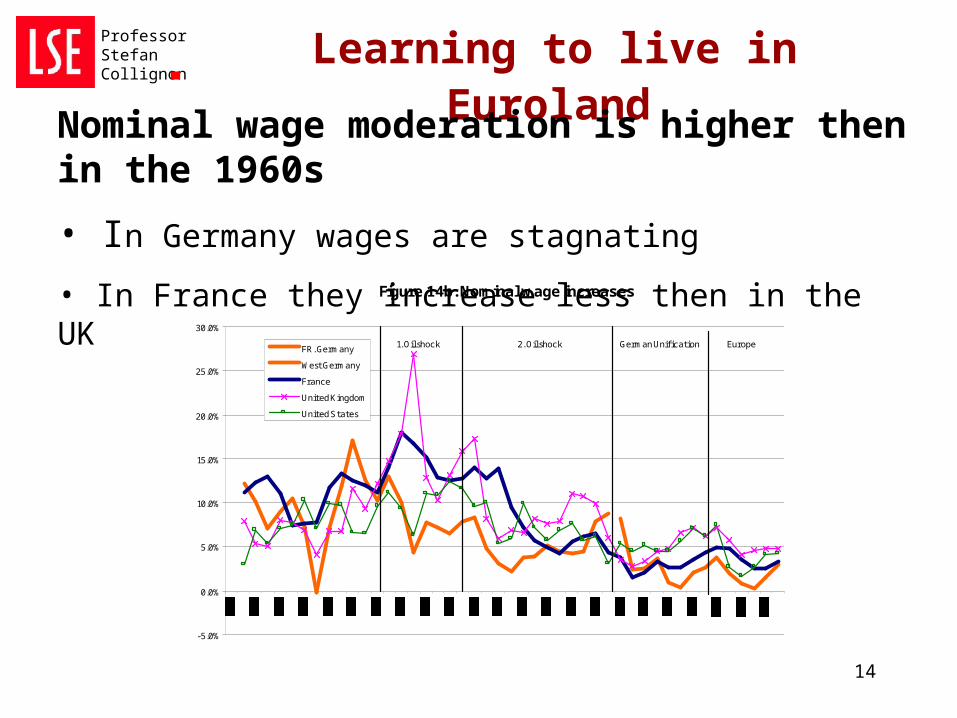

Learning to live in Euroland Professor Stefan Collignon

Nominal wage moderation is higher then in the 1960s

• In Germany wages are stagnating

• In France they increase less then in the UKFigure 14b. Nominal wage increases

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

FR. Germany

West Germany

France

United Kingdom

United States

Europe2. Oil shock1. Oil shock German Unification

15

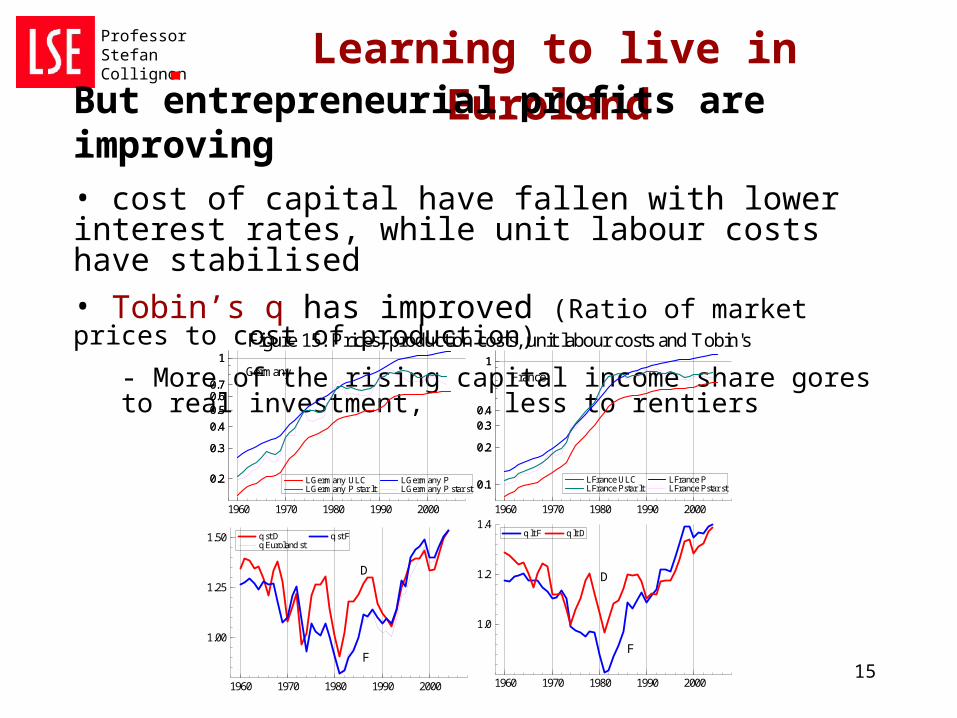

Learning to live in Euroland Professor Stefan Collignon

But entrepreneurial profits are improving• cost of capital have fallen with lower interest rates, while unit labour costs have stabilised

• Tobin’s q has improved (Ratio of market prices to cost of production)

- More of the rising capital income share gores to real investment, less to rentiers

0.2

0.3

0.4

0.50.60.7

1

0.2

0.3

0.4

0.50.60.7

1

1960 1970 1980 1990 2000

Figure 15. Prices, production costs, unit labour costs and Tobin's q

Germany

LGermany ULC LGermany P star lt

LGermany P LGermany P star st 0.1

0.2

0.30.4

1

0.1

0.2

0.30.4

1

1960 1970 1980 1990 2000

France

LFrance ULC LFrance Pstar lt

LFrance P LFrance Pstar st

1960 1970 1980 1990 2000

1.00

1.25

1.50

F

D

q st D q Euroland st

q st F

1960 1970 1980 1990 2000

1.0

1.2

1.4

F

D

q lt F q lt D

16

Learning to live in Euroland Professor Stefan Collignon

The public sector

• Expenditure in France and Germany larger than in UK or US

• But no change over recent years

- no evidence for lower growth

• in Scandinavia it is even higher

-no stifling of lower growth

• Public investment

- is stable at 3 % of GDP in France

- has fallen to historic low of 1.7 % in Germany

17

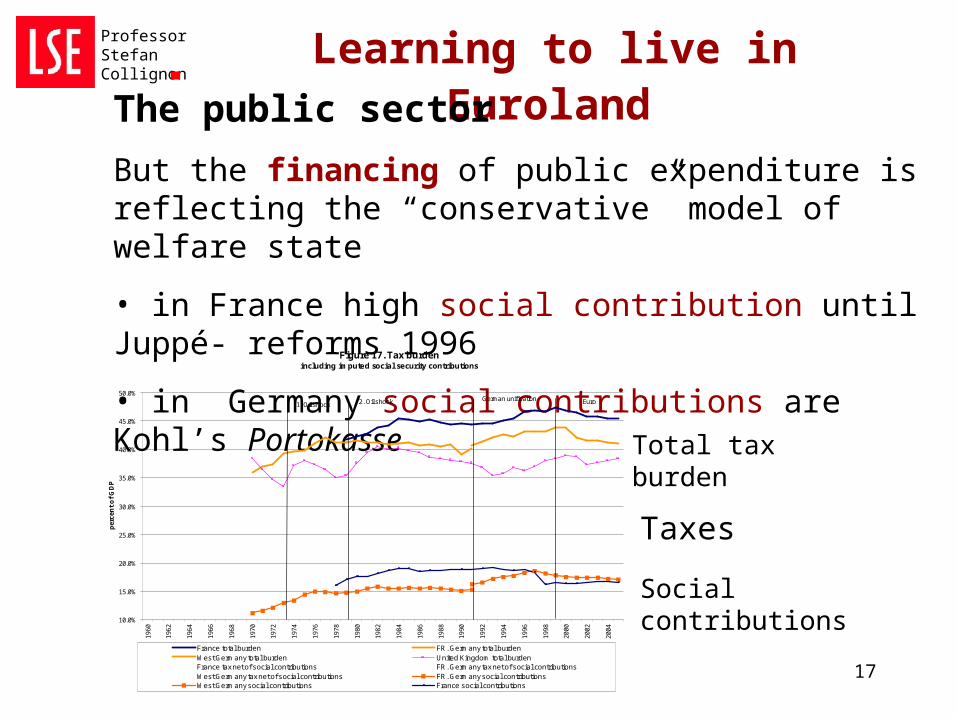

Learning to live in Euroland Professor Stefan Collignon

The public sector

But the financing of public expenditure is reflecting the “conservative” model of welfare state

• in France high social contribution until Juppé- reforms 1996

• in Germany social contributions are Kohl’s PortokasseFigure 17. Tax burden

including imputed social security contributions

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

per

cen

t o

f G

DP

France total burden FR. Germany total burdenWest Germany total burden United Kingdom total burdenFrance tax net of social contributions FR. Germany tax net of social contributionsWest Germany tax net of social contributions FR. Germany social contributionsWest Germany social contributions France social contributions

EuroGerman unif ication2. Oil shock1. Oil shock

Total tax burden

Taxes

Social contributions

18

Learning to live in Euroland Professor Stefan Collignon

To summarise:

• Economic structures in France and Germany have converged

- they are more alike than anglo-saxon economies

• The handicap is macroeconomic policy

- in EMU this is a matter of the policy mix

- monetary policy interacts with fiscal and wage policies

• Can Francallemagne improve their situation by “economic reforms”?

19

Learning to live in Euroland Professor Stefan Collignon

1. Is the labour market too rigid?

• Mobility: high in Germany led to same wage levels in East and West

• Are wages too high?

- Unskilled workers: reforms have happened

- Average wages reflect productivity: unit labour costs

20

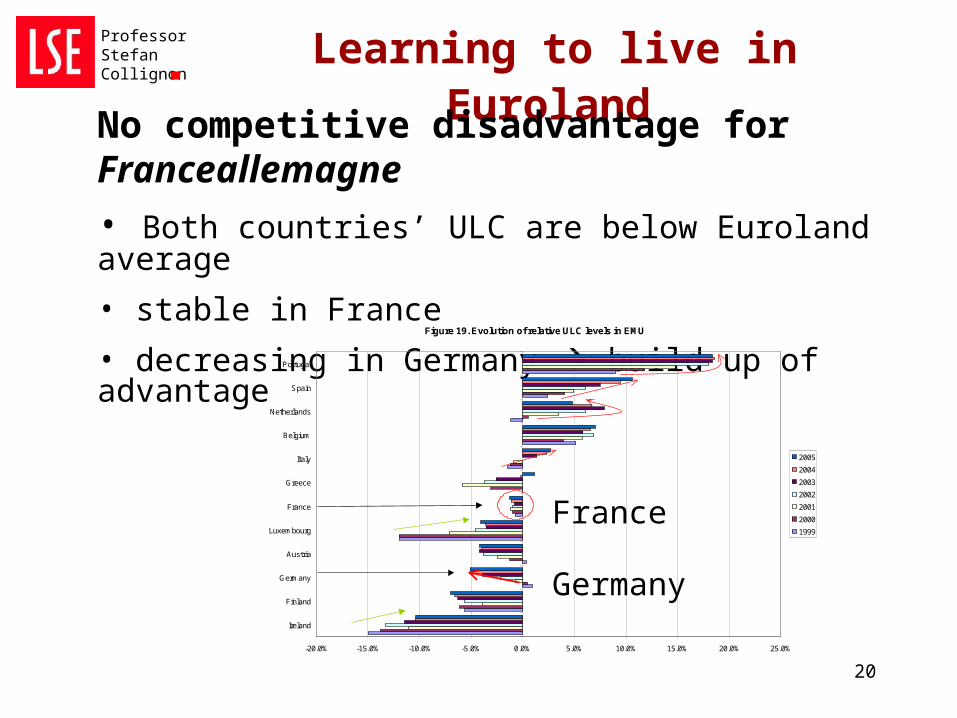

Learning to live in Euroland Professor Stefan Collignon

No competitive disadvantage for Franceallemagne

• Both countries’ ULC are below Euroland average

• stable in France

• decreasing in Germany build up of advantageFigure 19. Evolution of relative ULC levels in EMU

-20.0% -15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Ireland

Finland

Germany

Austria

Luxembourg

France

Greece

Italy

Belgium

Netherlands

Spain

Portugal

2005

2004

2003

2002

2001

2000

1999France

Germany

21

Learning to live in Euroland Professor Stefan Collignon

• This adjustment is justified, because Germany has lost the DM-advantage of low interest rates

• it translates into renewed competitiveness

-exports are increasing: from 25.7 % of GDP in 1999 to 32 % in 2004

• But France gained from losing FFr, hence more stable ULC

• But does not solve the problem, when lower ULC simply lead to falling prices rather than higher profits

- problem of large countries

22

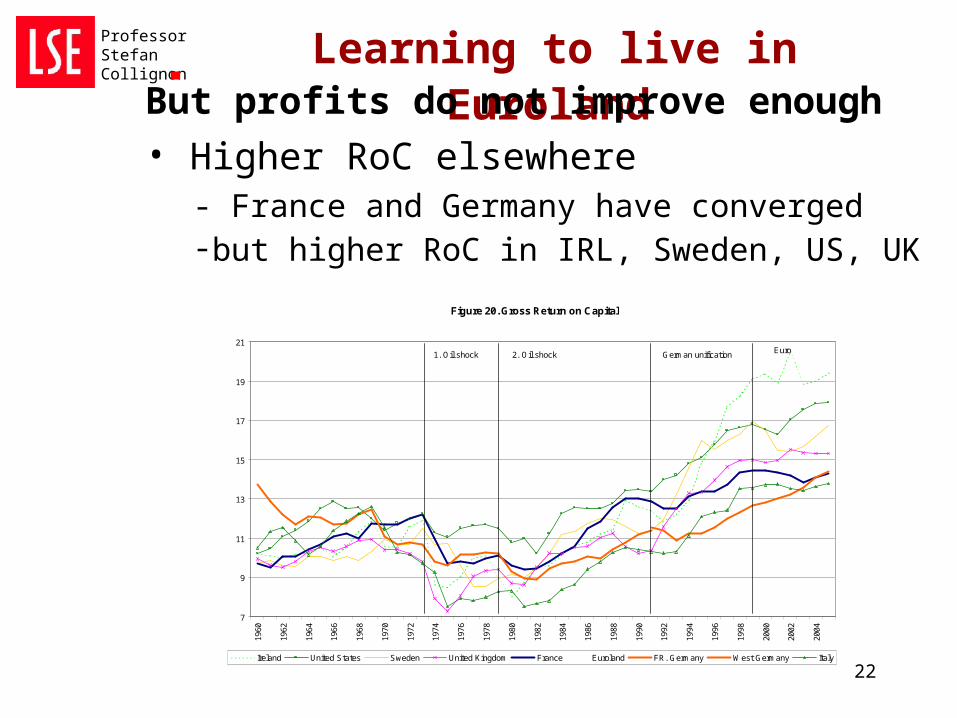

Learning to live in Euroland Professor Stefan Collignon

But profits do not improve enough

• Higher RoC elsewhere- France and Germany have converged-but higher RoC in IRL, Sweden, US, UK

Figure 20. Gross Return on Capital

7

9

11

13

15

17

19

21

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

Ireland United States Sweden United Kingdom France Euroland FR. Germany West Germany Italy

EuroGerman unification2. Oil shock1. Oil shock

23

Learning to live in Euroland Professor Stefan Collignon

1. Average productivity of capital stock is higher in anglosaxon and Scandinavian countries

• job protection versus income protection?

• low investment rate slows modernisation of capital stock

2. Investment reponds to Tobin’s q

• q responds to monetary policy

• In Franceallemagne still below Euroland average

• although ULC are falling, prices are also falling relative to Euroland price level: why?

24

Learning to live in Euroland Professor Stefan Collignon

The policy mix

• Overriding priority of price stability

• ECB must respond to ULC-developments (supply side)

• ECB must respond to fiscal policy (demand side)

- Aggregate fiscal stance for Euroland

- National responsibility

- Coordination only by SGP

25

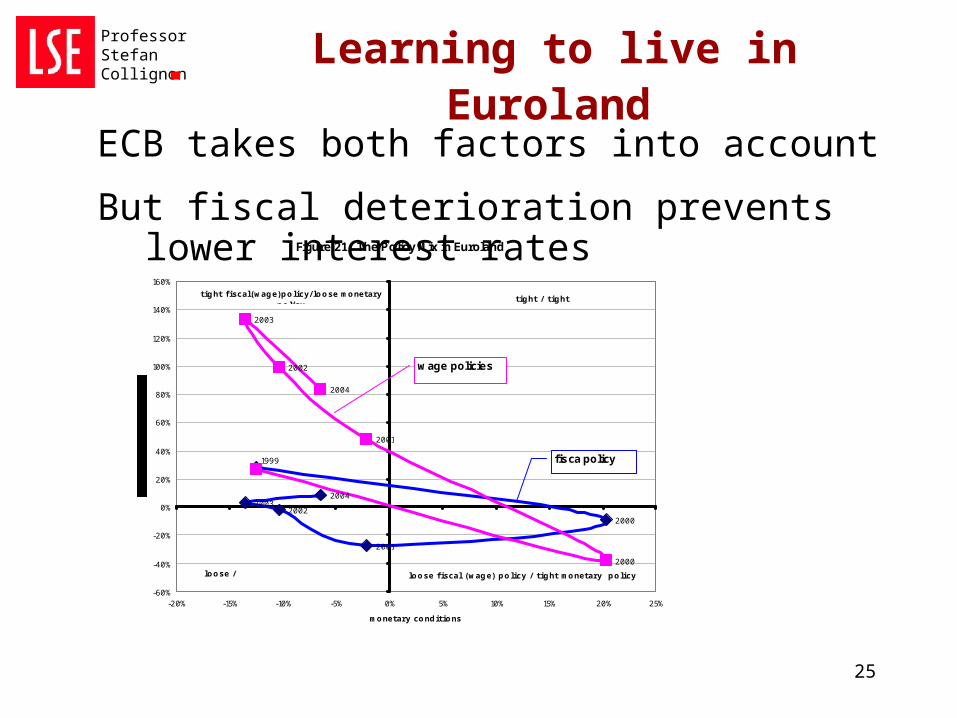

Learning to live in Euroland Professor Stefan Collignon

ECB takes both factors into account

But fiscal deterioration prevents lower interest ratesFigure 21. The Policy Mix in Euroland

1999

2000

2001

20022003

2004

2000

2001

2002

2003

2004

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

-20% -15% -10% -5% 0% 5% 10% 15% 20% 25%

monetary conditions

loose / loose

tight fiscal(wage)policy/ loose monetary policy

tight / tight

loose fiscal (wage) policy / tight monetary policy

fisca policy

wage policies

26

Learning to live in Euroland Professor Stefan Collignon

• ECB is more concerned about fiscal than wage policy

• SGP is not implemented

• Commission has no ultimate power

• Therefore: there exists no European fiscal policy and policy mix is sub-optimal

27

Learning to live in Euroland Professor Stefan Collignon

The solution

• Define aggregate fiscal stance for Euroland at EU-level

• Allocate deficit permits to member states for implementation

• But: binding obligation is only possible with full democratic backing

- vote by European parliament

- create European political Union with full democracy

28

Learning to live in Euroland Professor Stefan Collignon

This is where France and Germany have a role to play

But ultimately it is up to European citizens to charge the institutions with the proper management of their common affairs

European democracy is the next step!

29

Learning to live in Euroland Professor Stefan Collignon

Ceterum censeo: pactum stabilitatis esse delendum

Et rem publicam europaeam esse errigendam