1 county office fiscal oversight workshop october 25, 2006 presented in partnership with ccsesa,...

TRANSCRIPT

1

COUNTY OFFICE FISCAL OVERSIGHT

WORKSHOPOctober 25, 2006

Presented in partnership with CCSESA, FCMAT and BASC

2

COUNTY OFFICEFISCAL OVERSIGHT RESPONSIBILTIES

Deborah L. SimonsDirector, Division of Business Advisory Services

Los Angeles County Office of Education

Susan Birch Grinsell, CPAAssistant Superintendent of Business Services

Humboldt County Office of Education

3

What we’ll cover

An Overview of County Office Fiscal Oversight Responsibilities

What’s New in Fiscal Oversight

Feedback from the Field on the New Criteria and Standards

4

Overview of County Office Fiscal

Oversight

5

Why County Office Fiscal Oversight?

Increasing Number of State Bailouts

Lack of Authority to Intervene

Keep Local Problems from Becoming State Problems

Inappropriate Use of Long-term Debt

Inordinate Delays in Budget Adoption

6

What is AB 1200?

Legislation Became Law in 1992

Established Fiscal Crisis and Management Assistance Team (FCMAT)

Increased County Office Intervention Authority

7

What is AB 1200? (continued)

Crisis Prevention vs. Crisis Management

Multiyear Fiscal Solvency Analysis

Disclosure of Collective Bargaining and Other Multiyear Obligations

Tighter Deadlines/Increased Penalties

8

What is AB 1200? (continued)

State Criteria and Standards/Milestones for Measurement of Fiscal Health

County Office Fiscal Advisor with Stay or Rescind Authority

State Take-Over in Extreme Situations

9

How Do County Offices Implement Fiscal Oversight?

10

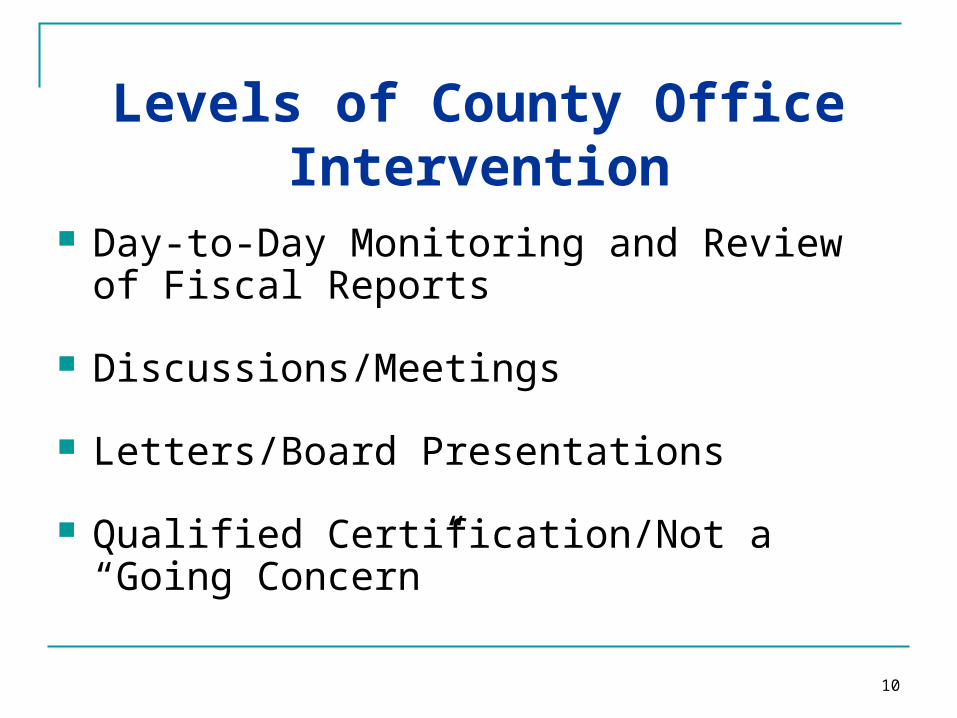

Levels of County Office Intervention

Day-to-Day Monitoring and Review of Fiscal Reports

Discussions/Meetings

Letters/Board Presentations

Qualified Certification/Not a “Going Concern”

11

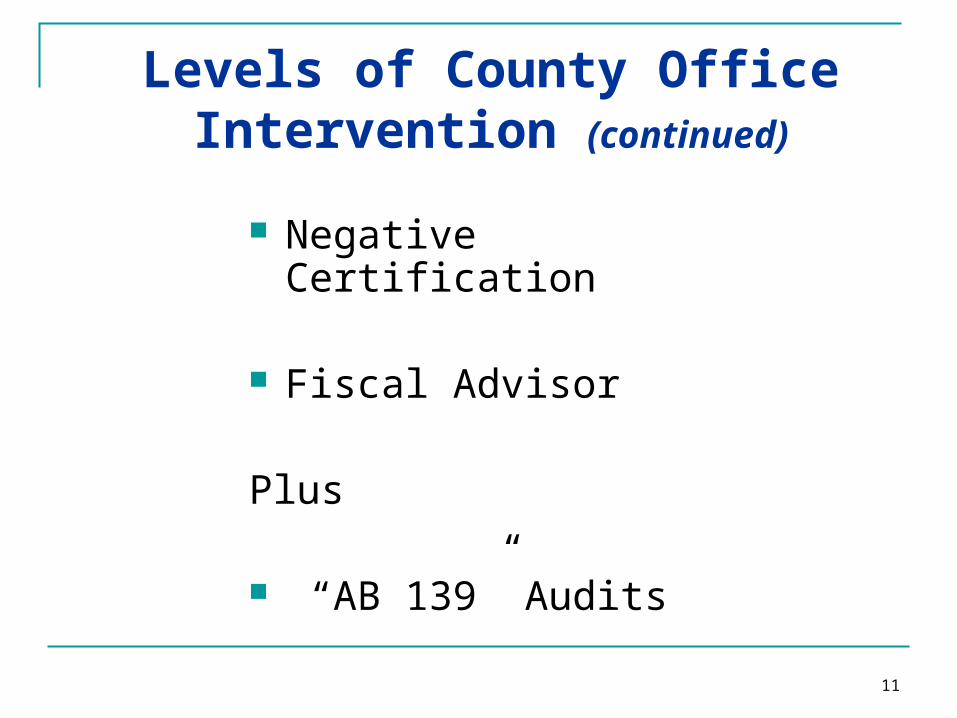

Levels of County Office Intervention (continued)

Negative Certification

Fiscal Advisor

Plus

“AB 139” Audits

12

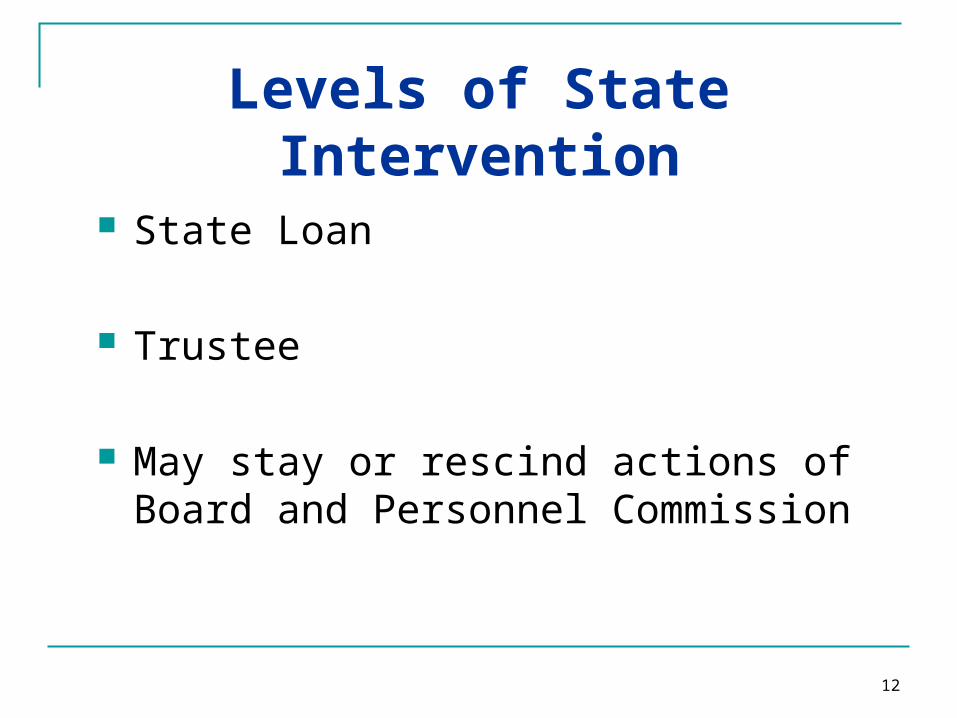

Levels of State Intervention

State Loan

Trustee

May stay or rescind actions of Board and Personnel Commission

13

Levels of State Intervention

(continued) Administrator

Assumes rights and powers of Board

Board becomes advisory only without compensation/benefits

District superintendent automatically leaves

Other high level management can be fired

14

Ongoing Monitoring

Analytic review of:

Budgets

Interim Reports

Unaudited Actuals

15

Ongoing Monitoring (continued)

Collective Bargaining Disclosures

Independent Audits/Audit Exceptions

Expenditures/Cash Flows

Annual Financial and Attendance Reports

16

Ongoing Monitoring (continued)

Analyses Using County Office Data Bases

Contact with District Staff

FCMAT “Predictors of School Agencies Needing Assistance”

Newspaper Articles

Comments from FCMAT, CDE, auditor, other districts, community, etc.

17

Taking Action Based on Financial Analysis

Conditional Approval/Disapproval of Budgets

Change of Interim Certification to Qualified/Negative

Declare District as “Not a Going Concern”

Prepare “AB 139” Reports on Districts with Fiscal Issues

Assign Fiscal Expert/Advisor

Notify Board of Concerns About Proposed Collective Bargaining Agreement

18

Taking Action Based on Financial Analysis (continued)

Notify District of Fiscal Impact of Negative Fund Balances, Declining Enrollment, Audit Findings, Low Cash Balances, etc.

Conduct “AB 139” Audits of Districts with Potential Illegal Fiscal Practices

Conduct a Study of the Financial and Budgetary Conditions of the District

Direct the District to Submit a Plan for Addressing Its Adverse Fiscal Condition

19

Impact of Fiscal Oversight Duties on

County Offices

20

Impact of Fiscal Oversight Duties on County Offices

White Hat of Service

Black Hat of Mandated Solvency

Bankruptcies – Reality vs. Legislative Perception

Until 2004, Penalty of 40 Percent for Failure

Attempt at Uniform Application

Broad Intervention Powers Scaled Back

21

Impact of Fiscal Oversight Duties on County Offices

(continued)

Impact of State Loan on County Office

SPI may review quality of county superintendent fiscal oversight of district

SPI may assume county superintendent’s fiscal oversight duties

22

Common Reactions to County Office

Intervention

23

Common Reactions to County Office Intervention

Denial

Staff Fired or Leave

Distrust of Fiscal Data

Appeals to CDE/Lawsuits

24

Common Reactions to County Office Intervention

(continued)

Media Attention

Political Attention

Chaotic District Board Meetings

Union Pressure

25

Keys to Successful Fiscal Oversight

District

Good financial practices

Ongoing communication with County Office

26

Keys to Successful Fiscal Oversight (continued)

County Office

Knowledgeable staff with understanding of district operations

Ongoing communication with district

Understand the big picture

Proactive review

27

Feedback from the Field

on the New Criteria and

Standards

28

Background

AB 2756 Purpose: Help identify districts that are

developing financial problems before the problems become severe

29

AB 2756 District health indicators

Specified comparisons and reviews to be included

Clear definitions/guidelines for financial certifications

Comprehensive review and assessment of the financial conditions of districts

FCMAT Predictors of School Agencies Needing Intervention

30

AB 2756 (continued)

SPI Committee to Revise Standards and Criteria

Timeline for the work November 2004 SBE approval – June 2005 Implemented with 2006-07 Budgets

31

AB 2756 (continued)

Committee representatives SBE CDE CCSESA (BASC) CTA ACSA DOF SCO FCMAT

32

Information Gathering

COE CBO List Serve provided by FCMAT

Six questions About 14 COE’s responded Full responses are in your packets

Statistical Data Summary from 7 COE’s is also part of your

materials

33

Information Gathering Results

Overall impressions were similar

North to South

Large to small COE’s

34

What was the feedback from school districts in your county? What was their overall impression and what did they specifically like/dislike? Advantages

Good information District administration and board

Consistent wording of the standards from a positive perspective

Automated features of the software

One-page summary of district health

35

What was the feedback from school districts in your county? What was their overall impression and what did they specifically like/dislike? (continued) Concerns:

Time consuming to prepare

Collect and enter data

Length of the report (23 pages) was intimidating for boards

Information from districts was incomplete

“Not Mets” did not always indicate fiscal instability

36

What was the feedback from school districts in your county? What was their overall impression and what did they specifically like/dislike? (continued) Concerns

Stigma of “Not Mets”

Specific Criteria/Standards or data elements Long – term commitments Base Revenue Limit changes (NSS) Salary and Benefit breakout by 3 groups Total health benefit costs

37

Was the software easy for the districts to use?

Yes (mostly)

Some difficulty in navigating

Difficult to read & distinguish between sections

38

Were the reports easy for the districts to use?

Yes (mostly)

Certification page was a good recap

Some boards questioned “Not Mets” - but not all Presentation styles differed widely

39

Were the reports easy for the districts to use?

Areas of confusion

ADA and enrollment for charter ADA, County ADA, declining enrollment and NSS

Inter-fund transfers to “cover operating deficits” related to other funds DM match Contributions to capital project reserves

Independent position control: good or bad

40

From your particular COE perspective, how useful was it in helping you meet your oversight responsibilities? How did it make your oversight responsibilities more difficult?

Helpful

More information

Validated information that some COE’s already requested

Districts took it more seriously/more thoughtful More reasonable assumptions Provided better information

41

From your particular COE perspective, how useful was it in helping you meet your oversight responsibilities? How did it make your oversight responsibilities more difficult? (continued)

Helpful

Certification page was a useful tool

Quality control $3.3 million error in a revenue projection

42

From your particular COE perspective, how useful was it in helping you meet your oversight responsibilities? How did it make your oversight responsibilities more difficult? (continued) Difficulties

Districts completed the form incorrectly COE staff assistance

Number of “Not Met’s” for NSS

Prior year information needed to be audited for accuracy Prior to trend analysis

43

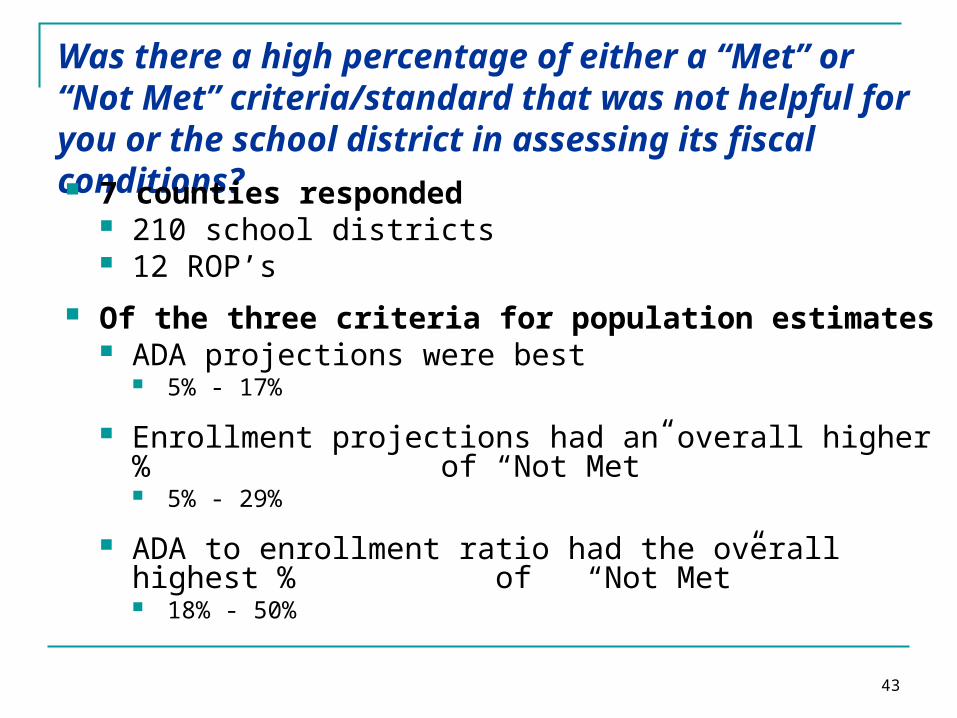

Was there a high percentage of either a “Met” or “Not Met” criteria/standard that was not helpful for you or the school district in assessing its fiscal conditions? 7 counties responded

210 school districts 12 ROP’s

Of the three criteria for population estimates ADA projections were best

5% - 17%

Enrollment projections had an overall higher % of “Not Met” 5% - 29%

ADA to enrollment ratio had the overall highest % of “Not Met” 18% - 50%

44

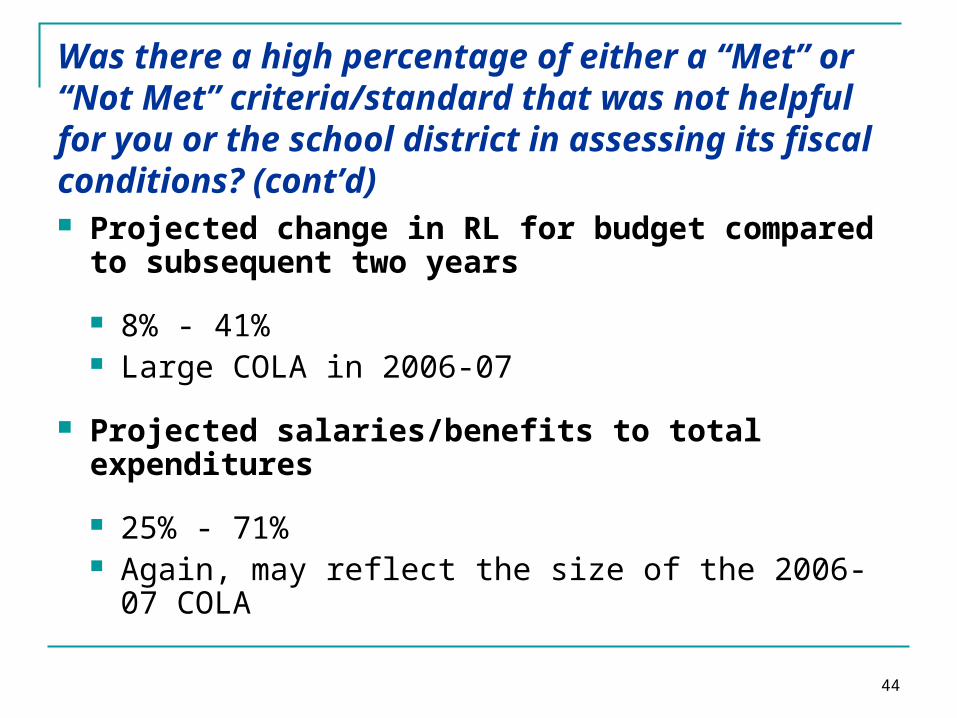

Was there a high percentage of either a “Met” or “Not Met” criteria/standard that was not helpful for you or the school district in assessing its fiscal conditions? (cont’d) Projected change in RL for budget compared to

subsequent two years

8% - 41% Large COLA in 2006-07

Projected salaries/benefits to total expenditures

25% - 71% Again, may reflect the size of the 2006-07 COLA

45

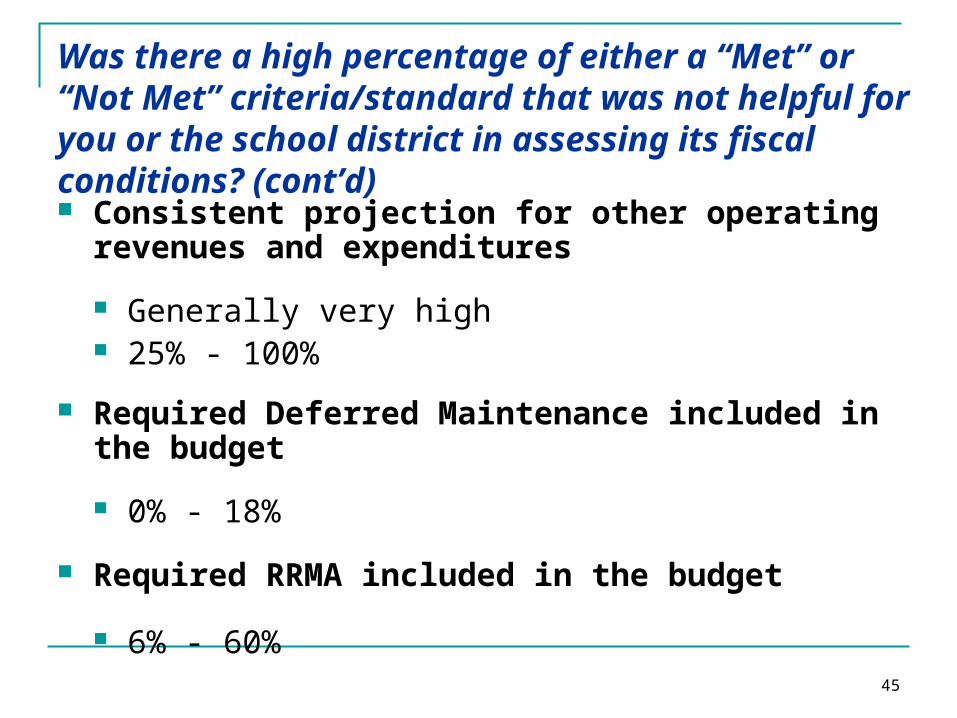

Was there a high percentage of either a “Met” or “Not Met” criteria/standard that was not helpful for you or the school district in assessing its fiscal conditions? (cont’d) Consistent projection for other operating revenues and

expenditures

Generally very high 25% - 100%

Required Deferred Maintenance included in the budget

0% - 18%

Required RRMA included in the budget

6% - 60%

46

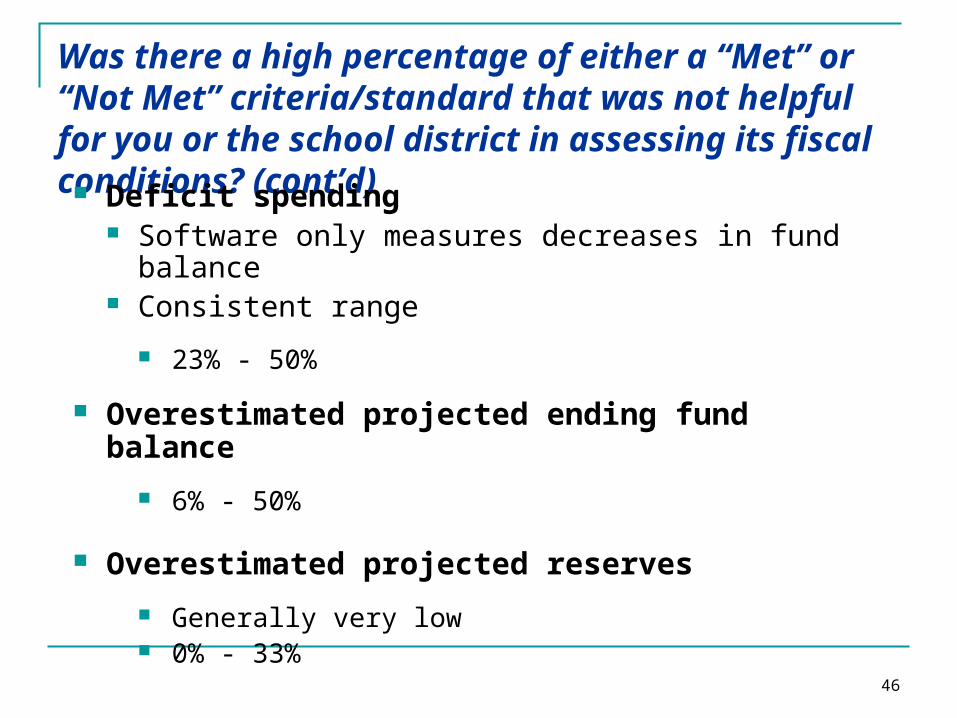

Was there a high percentage of either a “Met” or “Not Met” criteria/standard that was not helpful for you or the school district in assessing its fiscal conditions? (cont’d)

Deficit spending Software only measures decreases in fund balance Consistent range

23% - 50%

Overestimated projected ending fund balance

6% - 50%

Overestimated projected reserves

Generally very low 0% - 33%

47

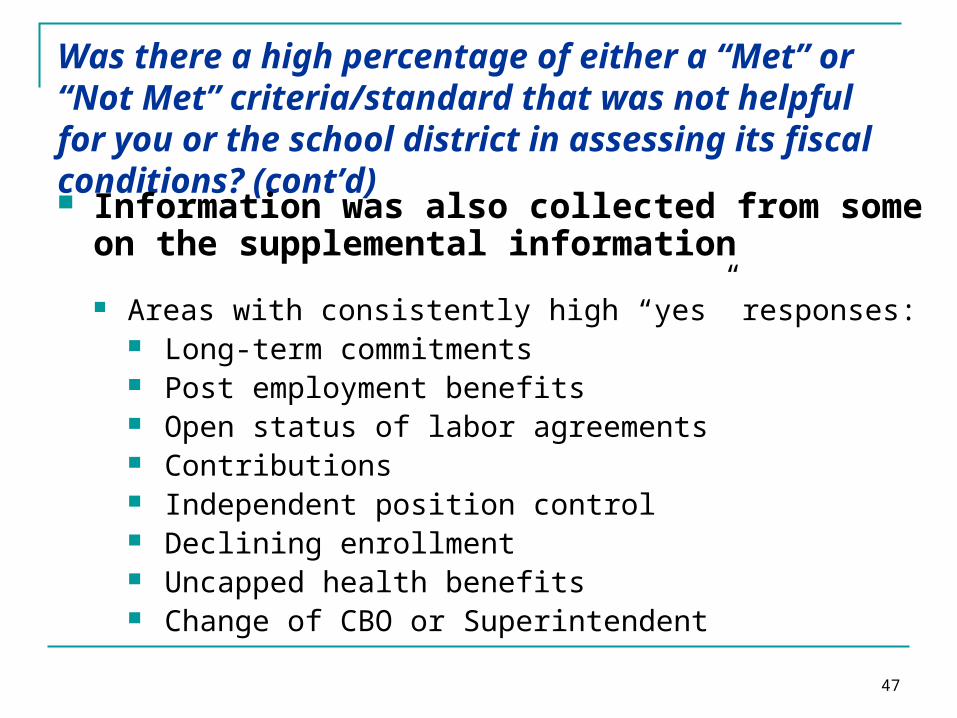

Was there a high percentage of either a “Met” or “Not Met” criteria/standard that was not helpful for you or the school district in assessing its fiscal conditions? (cont’d) Information was also collected from some on the

supplemental information

Areas with consistently high “yes” responses: Long-term commitments Post employment benefits Open status of labor agreements Contributions Independent position control Declining enrollment Uncapped health benefits Change of CBO or Superintendent

48

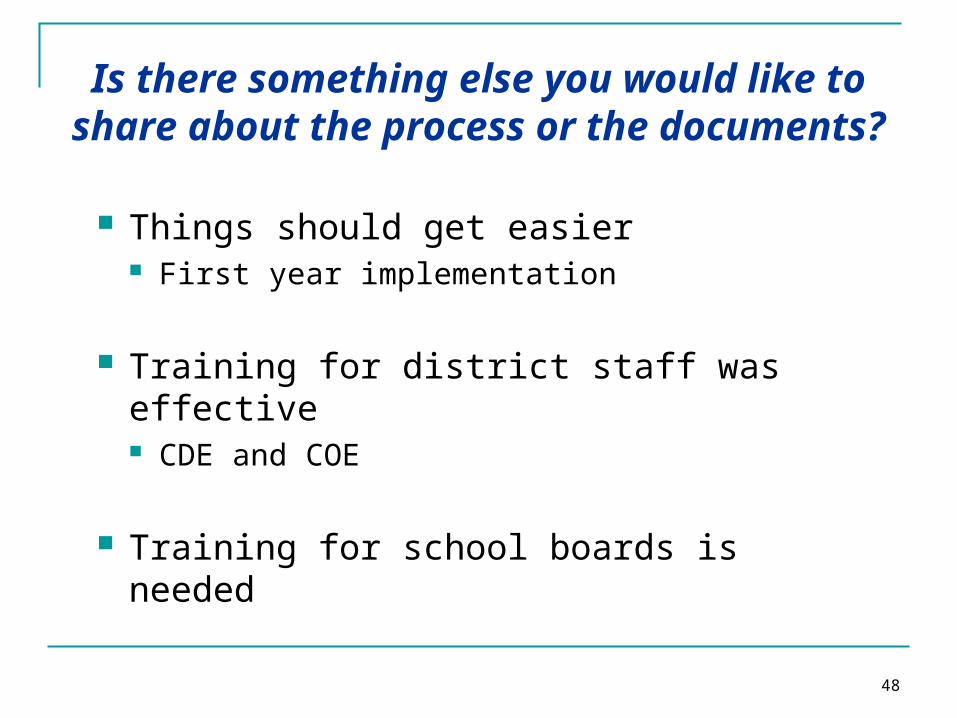

Is there something else you would like to share about the process or the

documents? Things should get easier

First year implementation

Training for district staff was effective CDE and COE

Training for school boards is needed

49

Is there something else you would like to share about the process or the

documents? (continued)

Software could be more user friendly

Yes/no buttons once pushed couldn’t be cleared w/o deleting the document, etc.

Hitting the “Enter” key relocated the cursor somewhere other than the next data field

50

Is there something else you would like to share about the process or the

documents? (continued) Long – term commitment test related to

General Fund revenues

Not always correlative

COP’s, GO bonds and CFD’s

51

Next Steps

Coordination with CDE

Did non-compliance mean districts were facing fiscal problems?

Technical software User friendly formatting Technical software cleanup

Electronic linkage of current year budget and multi-year projections

Coordination of RRMA and Deferred Maintenance

52

Next Steps (continued)

Coordination with CDE Clarifying language/explanations necessary to be

sure interpretation is consistent throughout the state Total Health Benefit Costs Includable ADA

Next round - Interim Reports!

Collect the same type of data

53

Any Questions?

Thank you