1 1 june, 2014. aeromexico: mexico’s premium revenue carrier business loungesbusiness class...

TRANSCRIPT

11

June, 2014

AEROMEXICO: MEXICO’S PREMIUM REVENUE CARRIER

Business LoungesBusiness Class

Leading airline in Mexico

Only Full Service Carrier / Two-class Service and Hub and Spoke Model

Enhanced strategic alliances with Delta Air Lines and AIMIA

Strongest position in slot constrained Mexico City airport

80 destinations in 20 countries, over 600 daily flights

Only Latin American carrier with flights to Asia

GRUPO AEROMEXICO: INVESTMENT HIGHLIGHTS

3

Strengthening Mexican Economy & Attractive Long Term Growth

Strong Brand with Strategic Alliances

Strong pipeline of cost reduction initiatives, with a Flexible and Modern Fleet

Solid Financial and Risk Profile with Focus on Profitability

Only Full Service Premium Revenue Carrier in Mexico with highest domestic and international Market share among national carriers

Strong Growth Potential in Mexico City Despite Slot Constraints

STRENGTHENING MEXICAN ECONOMY

Growth Opportunities for Mexican Economy(1) Air Traffic Penetration

Mexico China Brazil Europe US

0.6 0.60.8

1.4

2.4

Flights Per Capita for Middle & Upper Class Population (>$15K)+0.8%-1.7% GDP growth

2014 2017 2018 2019

6.0%

2015 2016E E E E E E

5.0%

4.0%

3.0%

2.0%

1.0%

Millions

(1) Boeing Current Market Outlook as of June 2013.Source: : CONAPO, INEGI, SHCP, Criterios generales de Política Económica 2014. IMF World Economic Outlook – October 2012; Company filings.

2010 2025E

0%

20%

40%

60%

80%

100%

26% 20%

35%

25%

17%30%

14% 17%

7% 8%

D/E D+ C C+ AB

Percent

Favorable Demographics

Growing Middle Class Favorable Demographic Trends

Middle Class

6 4 2 0 2 4 6

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-95

6 4 2 0 2 4 6

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90-95

WomenMen

49mm 70 mm

(2010 – Demographics in Million) (2050 – Demographics in Million)

4

OUR FLIGHT PLAN

PRODUCTIVITY & COST CONTROL

STRATEGIC PARTNERSHIPS

OPERATIONALEXCELLENCE

COMMERCIALVALUE CREATION

PROFITABLE AND SUSTAINABLE GROWTH

Uniquely Positioned to Deliver Profitable and Sustainable Growth5

FINANCIAL STRENGTH AND RISK PROFILE

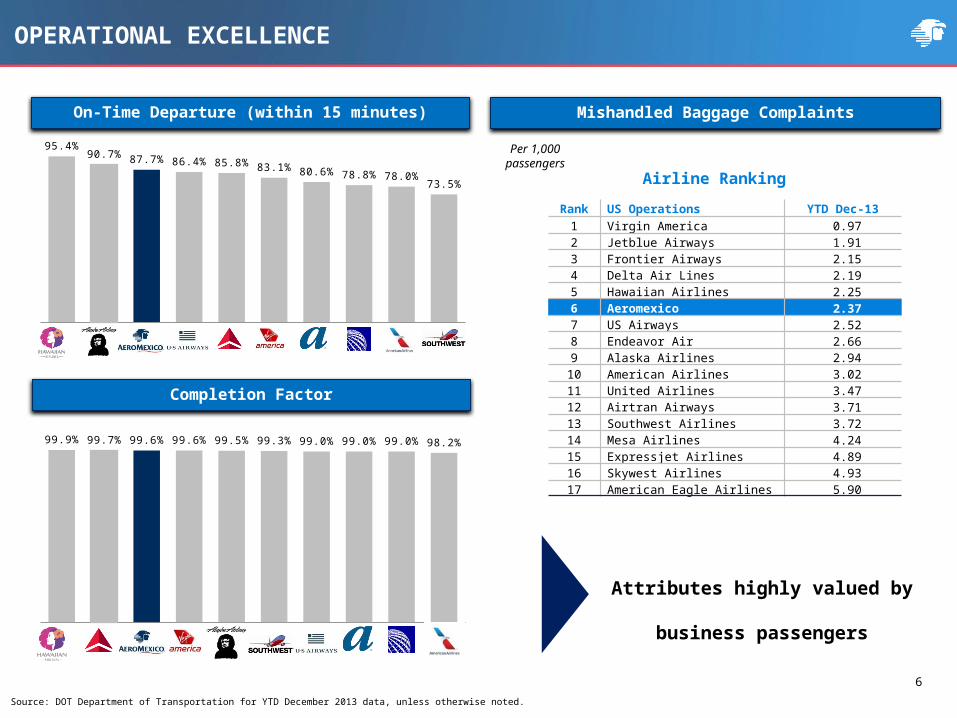

99.9% 99.7% 99.6% 99.6% 99.5% 99.3% 99.0% 99.0% 99.0% 98.2%

OPERATIONAL EXCELLENCE

On-Time Departure (within 15 minutes)

Source: DOT Department of Transportation for YTD December 2013 data, unless otherwise noted.

Airline Ranking

Mishandled Baggage Complaints

Completion Factor

95.4%90.7% 87.7% 86.4% 85.8% 83.1% 80.6% 78.8% 78.0%

73.5%

Per 1,000 passengers

Rank US Operations YTD Dec-131 Virgin America 0.972 Jetblue Airways 1.913 Frontier Airways 2.154 Delta Air Lines 2.195 Hawaiian Airlines 2.256 Aeromexico 2.377 US Airways 2.528 Endeavor Air 2.669 Alaska Airlines 2.94

10 American Airlines 3.0211 United Airlines 3.4712 Airtran Airways 3.7113 Southwest Airlines 3.7214 Mesa Airlines 4.2415 Expressjet Airlines 4.8916 Skywest Airlines 4.9317 American Eagle Airlines 5.90

Attributes highly valued by business passengers

6

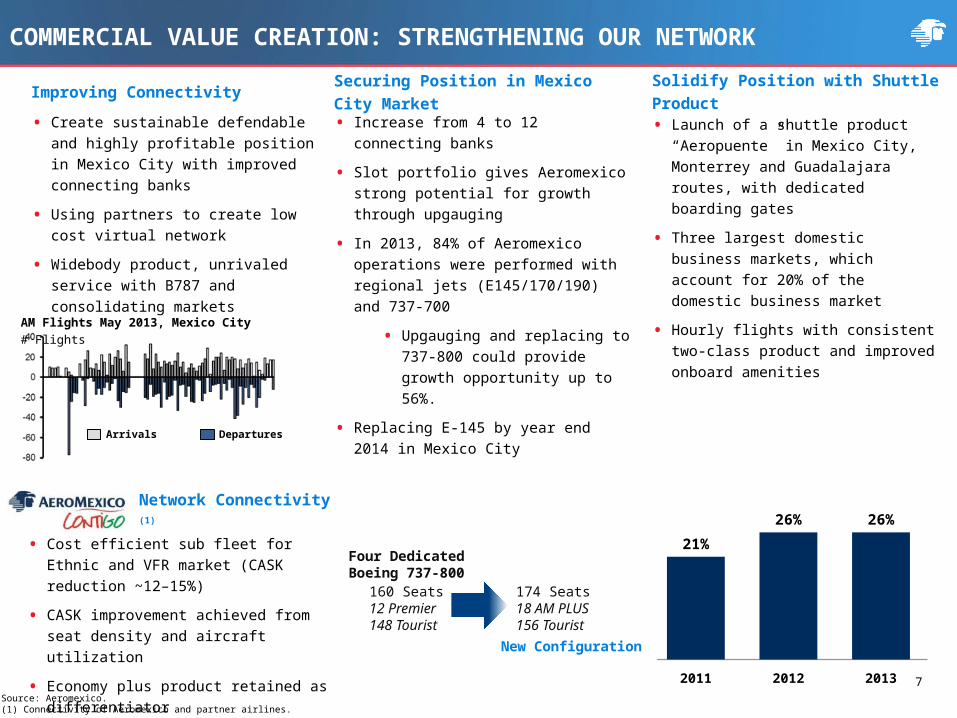

Source: Aeromexico.(1) Connectivity of Aeromexico and partner airlines.

2010 2011 2012 2013

21% 21%

26% 26%

• Create sustainable defendable and highly profitable position in Mexico City with improved connecting banks

• Using partners to create low cost virtual network

• Widebody product, unrivaled service with B787 and consolidating markets

COMMERCIAL VALUE CREATION: STRENGTHENING OUR NETWORK

Network Connectivity (1)

Improving Connectivity Securing Position in Mexico City Market Solidify Position with Shuttle Product

• Increase from 4 to 12 connecting banks

• Slot portfolio gives Aeromexico strong potential for growth through upgauging

• In 2013, 84% of Aeromexico operations were performed with regional jets (E145/170/190) and 737-700

• Upgauging and replacing to 737-800 could provide growth opportunity up to 56%.

• Replacing E-145 by year end 2014 in Mexico City

• Launch of a shuttle product “Aeropuente” in Mexico City, Monterrey and Guadalajara routes, with dedicated boarding gates

• Three largest domestic business markets, which account for 20% of the domestic business market

• Hourly flights with consistent two-class product and improved onboard amenities

7

• Cost efficient sub fleet for Ethnic and VFR market (CASK reduction ~12–15%)

• CASK improvement achieved from seat density and aircraft utilization

• Economy plus product retained as differentiator

160 Seats12 Premier148 Tourist

Four DedicatedBoeing 737-800

174 Seats18 AM PLUS156 Tourist

New Configuration

Arrivals Departures

AM Flights May 2013, Mexico City# Flights

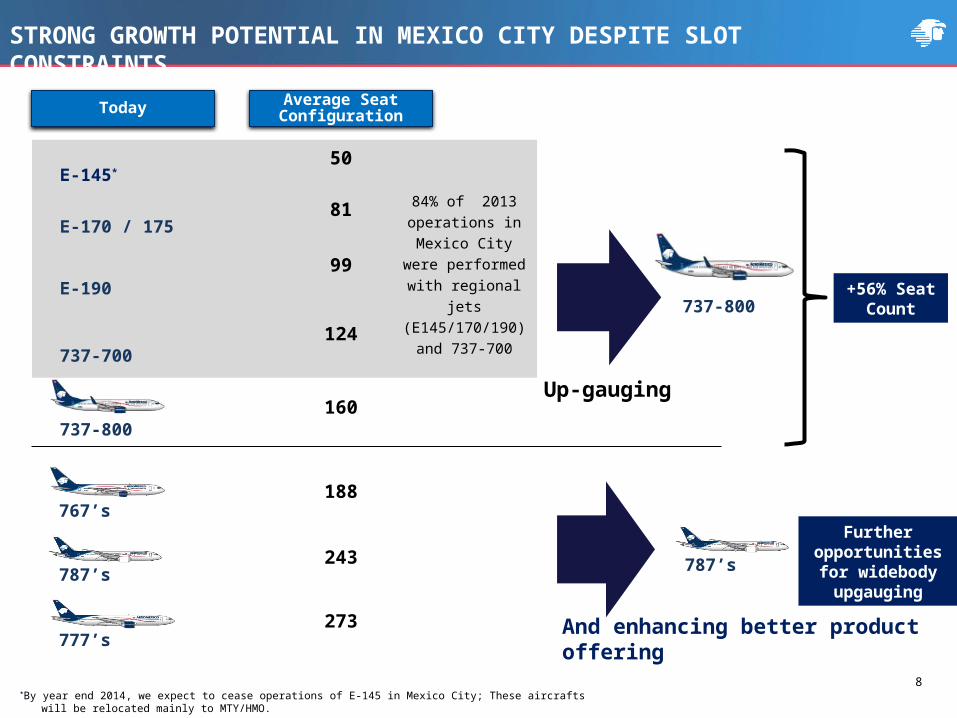

STRONG GROWTH POTENTIAL IN MEXICO CITY DESPITE SLOT CONSTRAINTS

Today Average Seat Configuration

767’s

777’s

787’s

E-145*

E-170 / 175

737-700

737-800

E-190

50

81

99

124

160

188

243

273

737-800+56% Seat

Count

Up-gauging

Further opportunities for

widebody upgauging

787’s

8

*By year end 2014, we expect to cease operations of E-145 in Mexico City; These aircrafts will be relocated mainly to MTY/HMO.

And enhancing better product offering

84% of 2013 operations in Mexico City were performed

with regional jets (E145/170/190) and

737-700

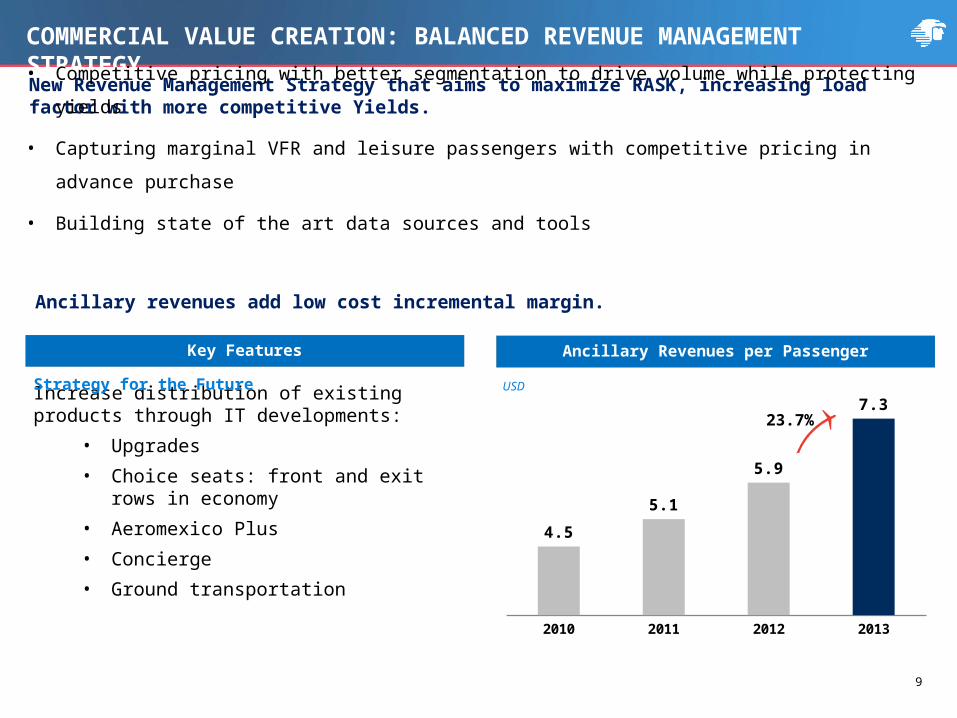

2010 2011 2012 2013

4.5

5.1

5.9

7.3

Ancillary revenues add low cost incremental margin.

USD

Key Features Ancillary Revenues per Passenger

Increase distribution of existing products through IT developments:

• Upgrades

• Choice seats: front and exit rows in economy

• Aeromexico Plus

• Concierge

• Ground transportation

Strategy for the Future

9

COMMERCIAL VALUE CREATION: BALANCED REVENUE MANAGEMENT STRATEGY

New Revenue Management Strategy that aims to maximize RASK, increasing load factor with more competitive Yields.

• Competitive pricing with better segmentation to drive volume while protecting yields

• Capturing marginal VFR and leisure passengers with competitive pricing in advance purchase

• Building state of the art data sources and tools

23.7%

Passenger TrafficMonthly Var % YoY

Load Factor (%)

10

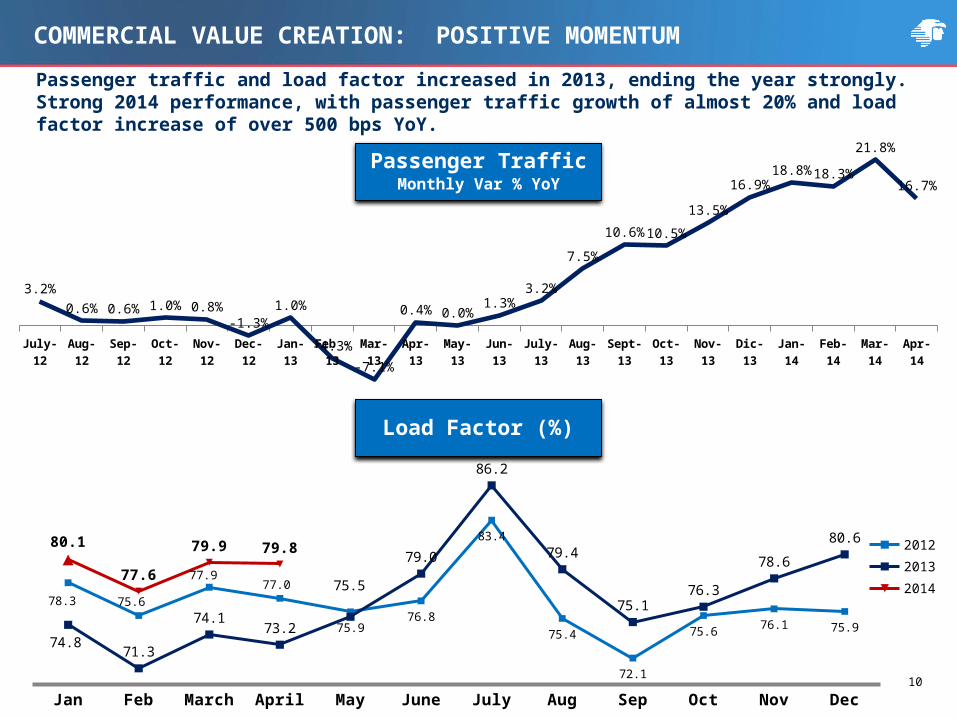

COMMERCIAL VALUE CREATION: POSITIVE MOMENTUM

Passenger traffic and load factor increased in 2013, ending the year strongly. Strong 2014 performance, with passenger traffic growth of almost 20% and load factor increase of over 500 bps YoY.

July-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb -13 Mar-13 Apr-13 May-13 Jun-13 July-13 Aug-13 Sept-13 Oct-13 Nov-13 Dic-13 Jan-14 Feb-14 Mar-14 Apr-14

3.2%0.6% 0.6% 1.0% 0.8%

-1.3%1.0%

-4.3%

-7.1%

0.4% 0.0%1.3%

3.2%

7.5%

10.6% 10.5%

13.5%

16.9%18.8% 18.3%

21.8%

16.7%

Jan Feb March April May June July Aug Sep Oct Nov Dec

78.3 75.6

77.977.0

75.976.8

83.4

75.4

72.1

75.6 76.1 75.974.8

71.3

74.173.2

75.5

79.0

86.2

79.4

75.176.3

78.6

80.680.1

77.6

79.9 79.8 201220132014

11

Aeroméxico Volaris

7.58

4.88

55%

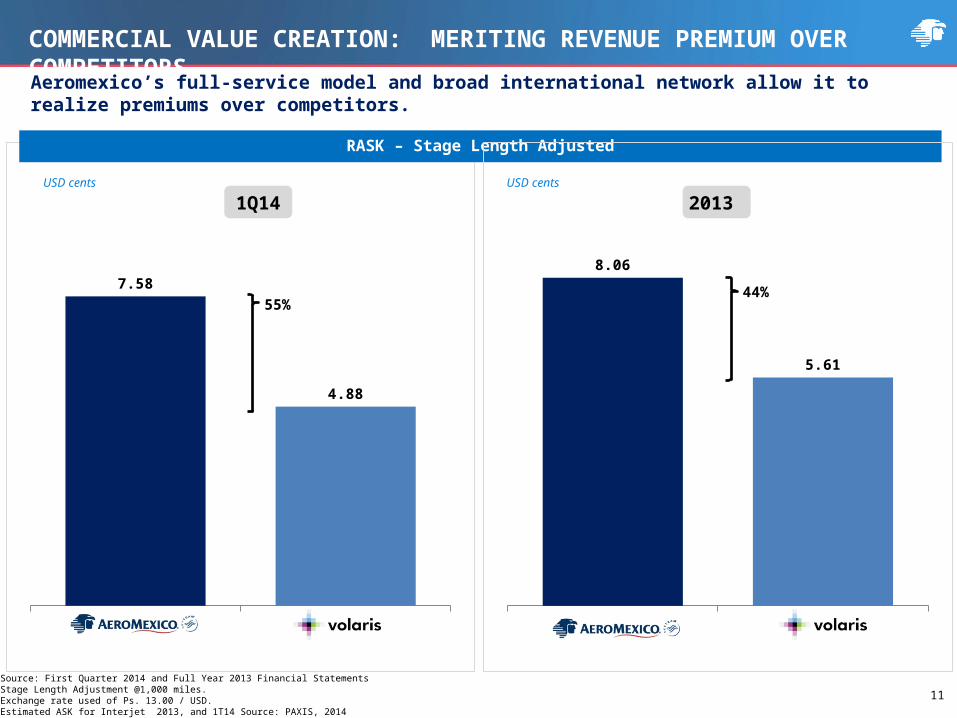

COMMERCIAL VALUE CREATION: MERITING REVENUE PREMIUM OVER COMPETITORS

RASK – Stage Length Adjusted

USD cents

Aeromexico’s full-service model and broad international network allow it to realize premiums over competitors.

1Q14USD cents

Aeroméxico Volaris

8.06

5.61

44%

2013

Source: First Quarter 2014 and Full Year 2013 Financial StatementsStage Length Adjustment @1,000 miles. Exchange rate used of Ps. 13.00 / USD.Estimated ASK for Interjet 2013, and 1T14 Source: PAXIS, 2014

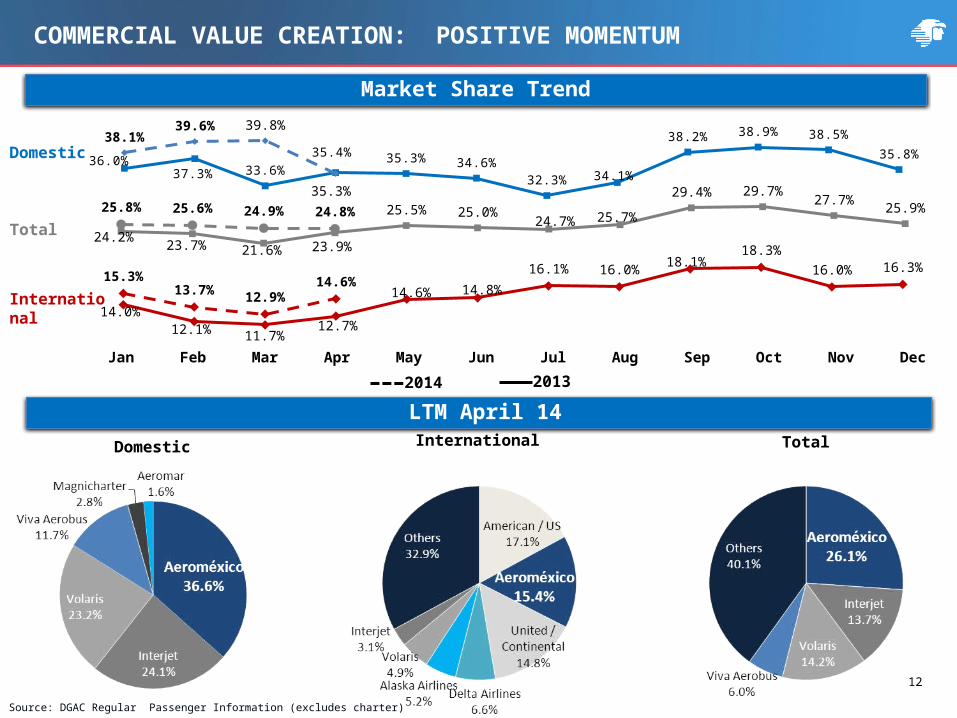

24.2%23.7% 21.6% 23.9%

25.5% 25.0% 24.7% 25.7%

29.4% 29.7%27.7% 25.9%25.8% 25.6% 24.9% 24.8%

36.0%37.3% 33.6%

35.4%35.3% 34.6%

32.3% 34.1%

38.2% 38.9% 38.5%

35.8%38.1%

39.6% 39.8%

35.3%

14.0%12.1% 11.7%

12.7%

14.6% 14.8%16.1% 16.0%

18.1%18.3%

16.0% 16.3%15.3%

13.7% 12.9%14.6%

International

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

12

Market Share Trend

Domestic Total

LTM April 14

Source: DGAC Regular Passenger Information (excludes charter)

COMMERCIAL VALUE CREATION: POSITIVE MOMENTUM

Total

International

Domestic

2014 2013

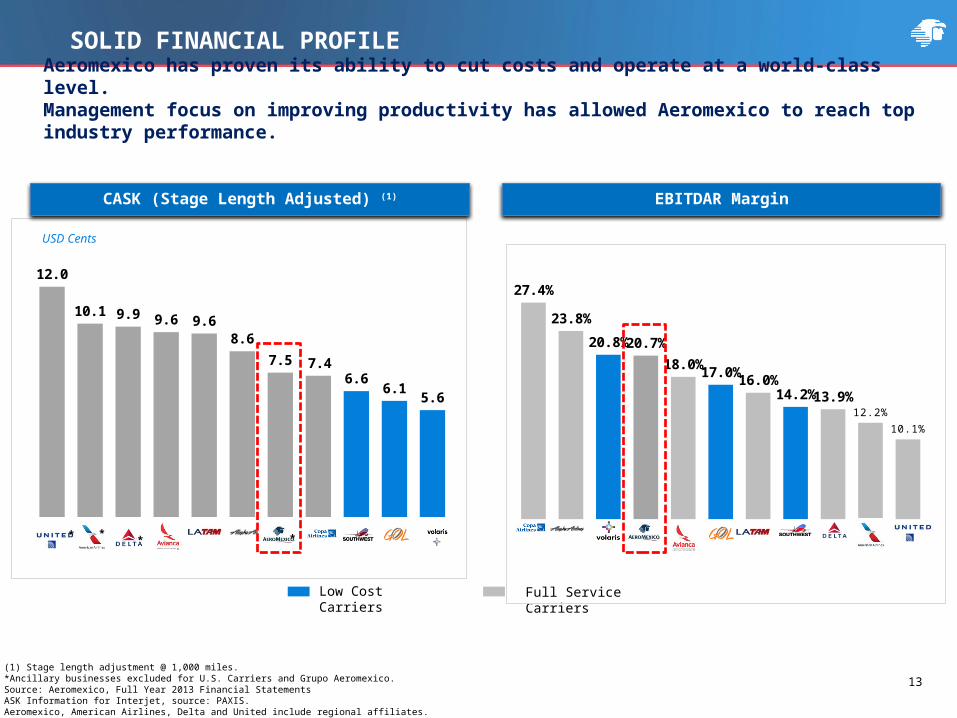

Aeromexico has proven its ability to cut costs and operate at a world-class level. Management focus on improving productivity has allowed Aeromexico to reach top industry performance.

12.0

10.1 9.9 9.6 9.68.6

7.5 7.46.6

6.15.6

SOLID FINANCIAL PROFILE

CASK (Stage Length Adjusted) (1)

USD Cents

Low Cost Carriers Full Service Carriers

EBITDAR Margin

27.4%

23.8%

20.8% 20.7%

18.0% 17.0% 16.0%14.2% 13.9%

12.2%

10.1%

13

** **

(1) Stage length adjustment @ 1,000 miles.*Ancillary businesses excluded for U.S. Carriers and Grupo Aeromexico.Source: Aeromexico, Full Year 2013 Financial StatementsASK Information for Interjet, source: PAXIS.Aeromexico, American Airlines, Delta and United include regional affiliates.

•New contracts with pilots, flight attendants and ground staff

•Restructuring and Integration of AM/AM Connect

•Maintenance Process Reengineering

•Increase fleet utilization

•ERP and Shared Services Centre

•Improving Distribution Costs

•Co-location in Airports

•Fleet Renewal

•Balance between Owned and Leased Aircrafts

•Unique Fleet Plan Flexibility

14

Strong pipeline of cost reduction initiatives.

Operational , Administrative & Sales Efficiencies Fleet StrategyLabor Costs

PRODUCTIVITY AND COST CONTROL INITIATIVES

Owned:(25%)USD 682mm

Leased:(75%)USD

$2.0bnSource: Aeromexico, Avitas Bluebook 2nd Half 2013.Aeromexico estimates as of 2013.(1) B767-2 and B787 data for: Mex-Mad. B737-7 and B737-8 / ERJ145,

ERJ190 and ERJ170 data for Mex-Mty.(2) Fleet proportion of leased vs. owned depends on fleet value.(3) On July 2013, Aeromexico announced the pricing of an offering of USD$117.4 million of 2.537% secured

notes guaranteed by the Export-Import Bank of the United States.

EJ170 & E190ERJ145 B737-8B737-7 B787B767

E145 E170 E190 B737-7 B737-8 B767 B787

100

84

77

100

86

100

81

(16%) (19%)

(9%)

(14%)

Estimated CASK Reduction (1)

Today 2018

E-145

E-170/175/190

737 – 700’s/800’sNG

767’s

787’s

777’s

E-170/190

737 – 800’sNG/MAX

787’s

Fleet Plan

Leased vs. Owned

Fleet Plan renewal provides CASK efficiencies, maintaining flexibility and reducing ownership cost.

PRODUCTIVITY AND COST CONTROL INITIATIVES: FLEET STRATEGY

Leased Owned

Annual Cost of Financing

4% to 6% (2)

10%-12%

USD $108M– USD $162Mcost savings due to ownership

Fleet Value: USD 2.7 billion(3)

Fleet Value

15

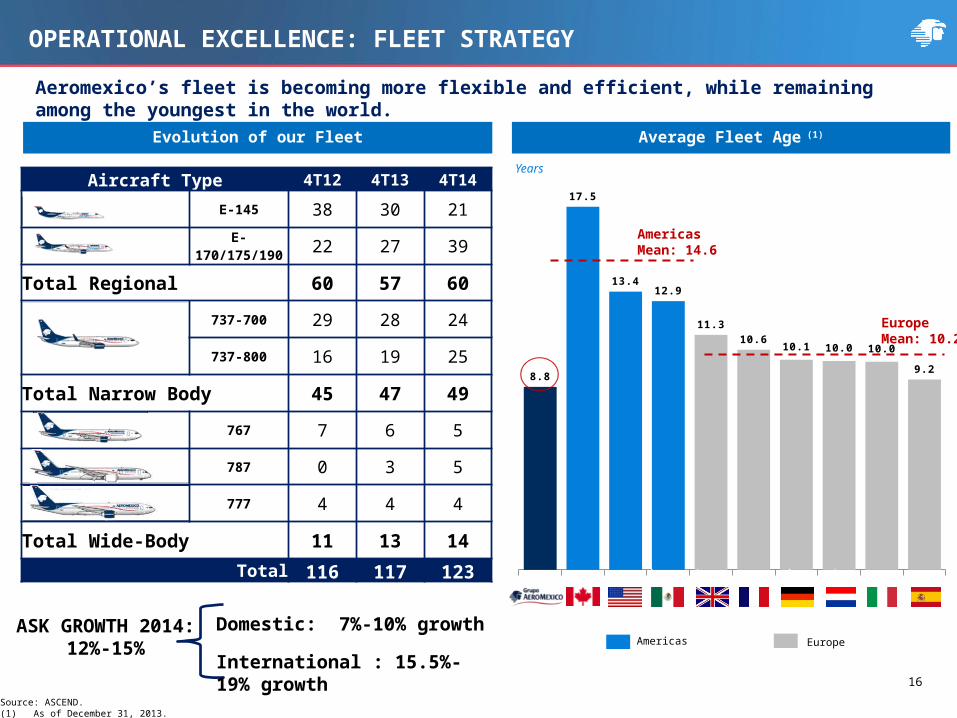

16

ASK GROWTH 2014:12%-15%

Domestic: 7%-10% growth

International : 15.5%-19% growth

Aircraft Type 4T12 4T13 4T14

E-145 38 30 21

E-170/175/190 22 27 39

Total Regional 60 57 60

737-700 29 28 24

737-800 16 19 25

Total Narrow Body 45 47 49

767 7 6 5

787 0 3 5

777 4 4 4

Total Wide-Body 11 13 14

Total 116 117 123

Average Fleet Age (1)

8.8

17.5

13.412.9

11.3

10.610.1 10.0 10.0

9.2

AmericasMean: 14.6

Europe Mean: 10.2

Years

Americas Europe

Aeromexico’s fleet is becoming more flexible and efficient, while remaining among the youngest in the world.

Source: ASCEND.(1) As of December 31, 2013.

Evolution of our Fleet

OPERATIONAL EXCELLENCE: FLEET STRATEGY

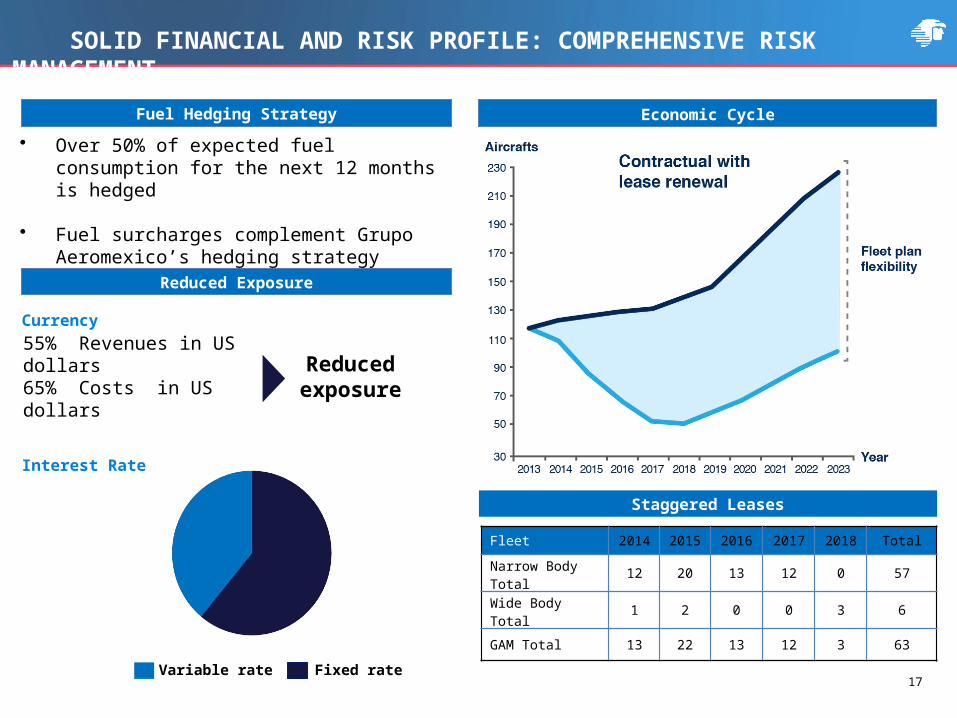

• Over 50% of expected fuel consumption for the next 12 months is hedged

• Fuel surcharges complement Grupo Aeromexico’s hedging strategy

Reduced Exposure

61% @ Fixed Rate

39%

55% Revenues in US dollars65% Costs in US dollars

Reduced exposure

61%

39%

Fuel Hedging Strategy

61% @ Fixed Rate

Fixed rate

58%

42%

Variable rate

Total

17

SOLID FINANCIAL AND RISK PROFILE: COMPREHENSIVE RISK MANAGEMENT

Economic Cycle

Staggered Leases

Fleet 2014 2015 2016 2017 2018 Total

Narrow Body Total 12 20 13 12 0 57

Wide Body Total 1 2 0 0 3 6

GAM Total 13 22 13 12 3 63

Currency

Interest Rate

18

2014 2015 2016 2017 2018+

36 36 37 35

228

43 26 41 63

129

SOLID FINANCIAL DEBT PROFILE

Debt Maturity Profile (1)

(1) Information as of March 2014(2) Last 12 months EBITDAR AS OF March 2014. Source: First Quarter 2014 Financial Statements, except GOL and Avianca (with latest available information of Full Year

2013)* Considers Adjusted EBITDAR

USD millions

11.7% 9.3% 11.5% 14.6% 52.9%

Benchmark Financial Net Debt / Adjusted EBITDAR (2)

Adjusted EBITDAR 2013: USD 622 M

Volaris GOL LATAM Avianca AeroMexico United American Delta Copa

6.5x5.8x 5.2x

4.2x 4.07x 3.6x 3.2x2.3x

0.9x

Low Cost Carriers Full Service Carriers

*

*

19Source: First Quarter 2014 and Full Year 2013 Financial Statements and Company Filings

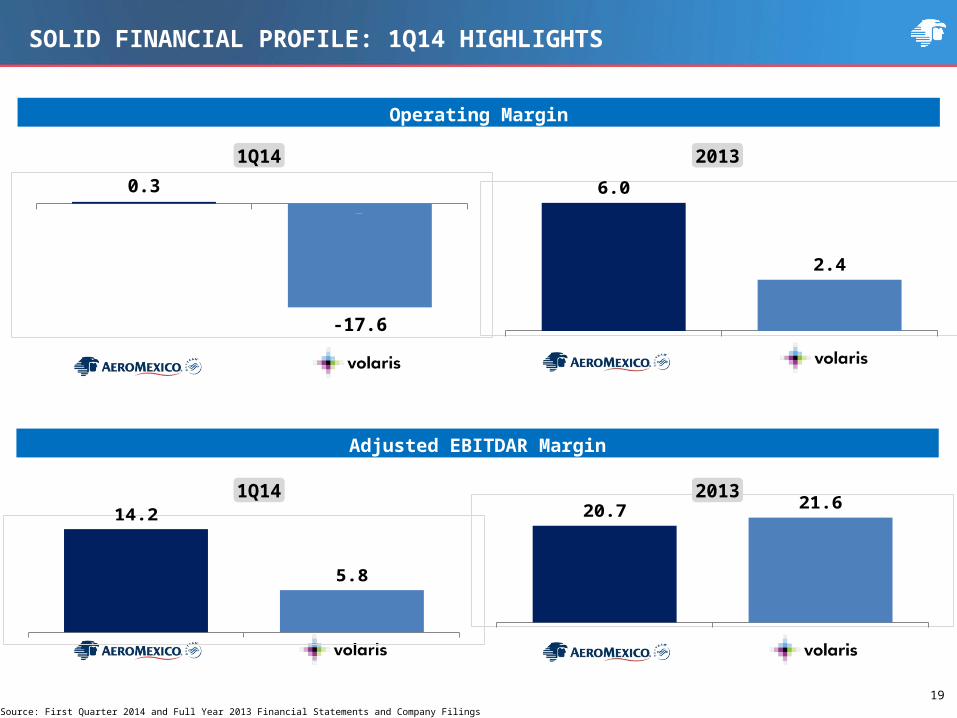

Operating Margin

1Q14 2013

A ero méxico V o laris

0.3

-17.6A ero méxico V o laris

6.0

2.4

Adjusted EBITDAR Margin

A ero méxico V o laris

14.2

5.8

A ero méxico V o laris

20.7 21.61Q14 2013

SOLID FINANCIAL PROFILE: 1Q14 HIGHLIGHTS

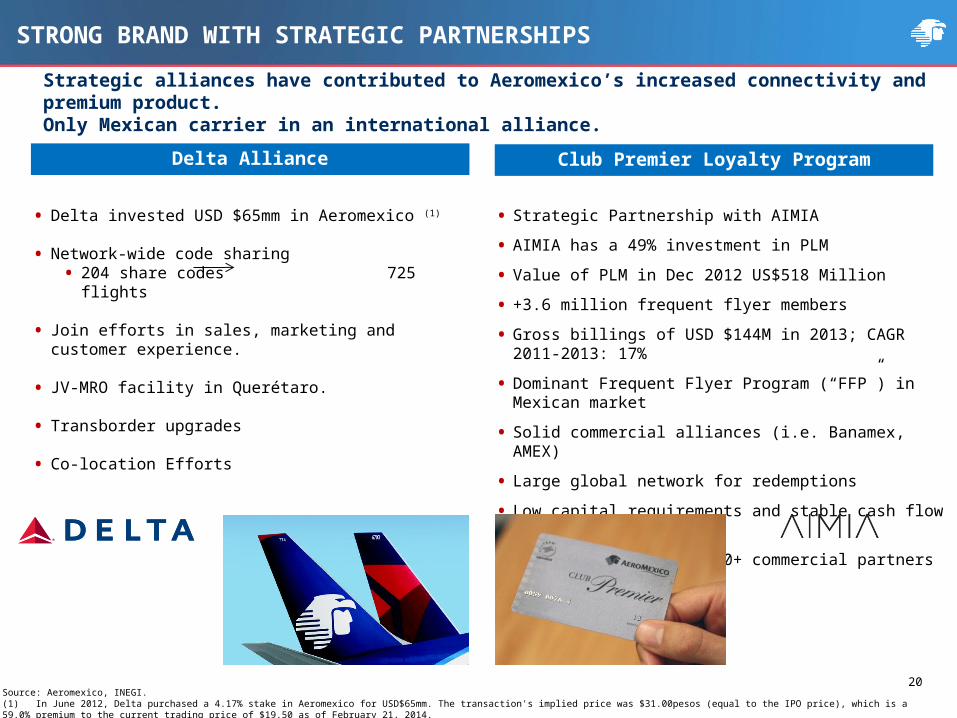

• Strategic Partnership with AIMIA

• AIMIA has a 49% investment in PLM

• Value of PLM in Dec 2012 US$518 Million

• +3.6 million frequent flyer members

• Gross billings of USD $144M in 2013; CAGR 2011-2013: 17%

• Dominant Frequent Flyer Program (“FFP”) in Mexican market

• Solid commercial alliances (i.e. Banamex, AMEX)

• Large global network for redemptions

• Low capital requirements and stable cash flow generation

• Earn kilometers with 90+ commercial partners

Source: Aeromexico, INEGI.(1) In June 2012, Delta purchased a 4.17% stake in Aeromexico for USD$65mm. The transaction's implied price was $31.00pesos (equal to the IPO price), which is a 59.0% premium to the current trading price of $19.50 as of February 21, 2014.

• Delta invested USD $65mm in Aeromexico (1)

• Network-wide code sharing• 204 share codes 725 flights

• Join efforts in sales, marketing and customer experience.

• JV-MRO facility in Querétaro.

• Transborder upgrades

• Co-location Efforts

Delta Alliance Club Premier Loyalty Program

STRONG BRAND WITH STRATEGIC PARTNERSHIPS

Strategic alliances have contributed to Aeromexico’s increased connectivity and premium product. Only Mexican carrier in an international alliance.

20

DISCLAIMER

This presentation is neither an offer for sale nor a request to buy any securities. Such offer or request may only be made through an offering memorandum containing the description of the terms and conditions of such offer and shall include detailed information of the company and its management, as well as the financial statements of Grupo Aeromexico, S.A. de C.V. (“Grupo Aeromexico”), in terms of the Securities Market Law (Ley del Mercado de Valores) (“LMV”) and the General provisions applicable to securities issuers and other securities market participants (Disposiciones de carácter general aplicables a las emisoras de valores y a otros participantes del mercado de valores) (the “Provisions”).

The information contained herein is confidential and shall not be reproduced in whole or in part or shared with third parties without the previous consent of Grupo Aeromexico.

This presentation contains information obtained from diverse sources and, despite it contains truthful information, no representation is hereby made by Grupo Aeromexico as to the accuracy, integrity and sufficiency of such information. Additionally, Grupo Aeromexico makes no representation in respect of the sufficiency or truthfulness of the assumptions, estimations, projections, hypothetical behavior analysis or in respect of other financial information included in the results of the financial models contained or used herein.

The results contained herein may substantially vary. Nothing herein shall be understood or construed as a representation or warranty as to future performance of the securities referred to herein.

The information included in this presentation has not been audited and it does not provide information on the company’s future performance. Aeromexico’s future performance depends on many factors and it cannot be inferred that any period’s performance or its comparison year-over-year will be an indicator of a similar performance in the future.

Thank You

Investor Relations Contact Information [email protected] (+52) 55 9132 4257

Daniel [email protected]