© 2007 thomson south-western. microeconomics macroeconomics

Post on 20-Dec-2015

236 views

TRANSCRIPT

© 2007 Thomson South-Western

© 2007 T

homson S

outh-Western

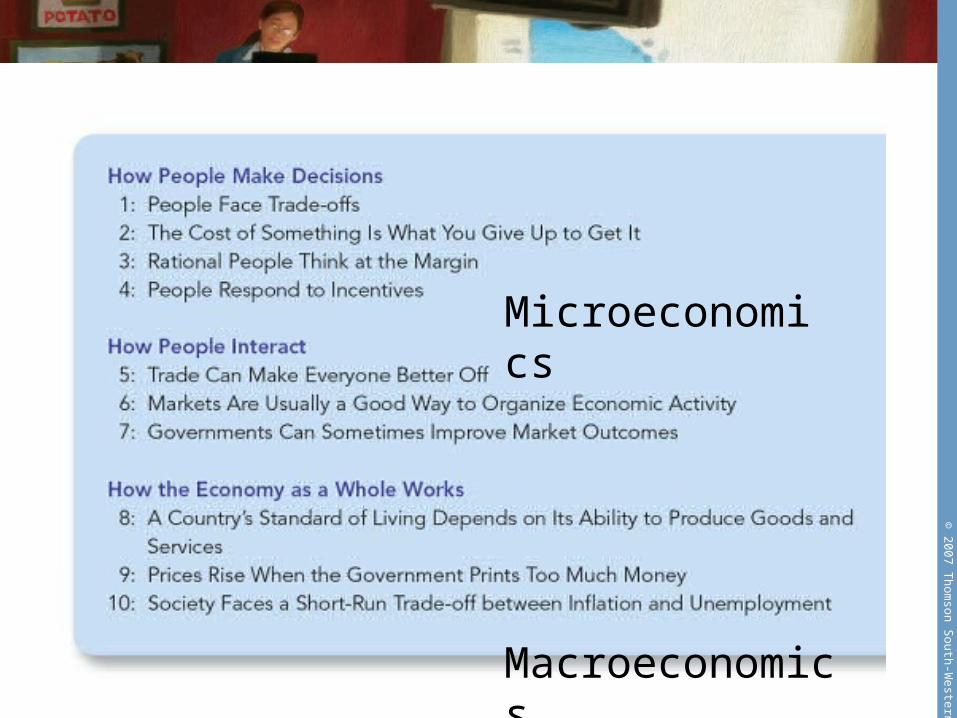

Microeconomics

Macroeconomics

© 2007 T

homson S

outh-Western

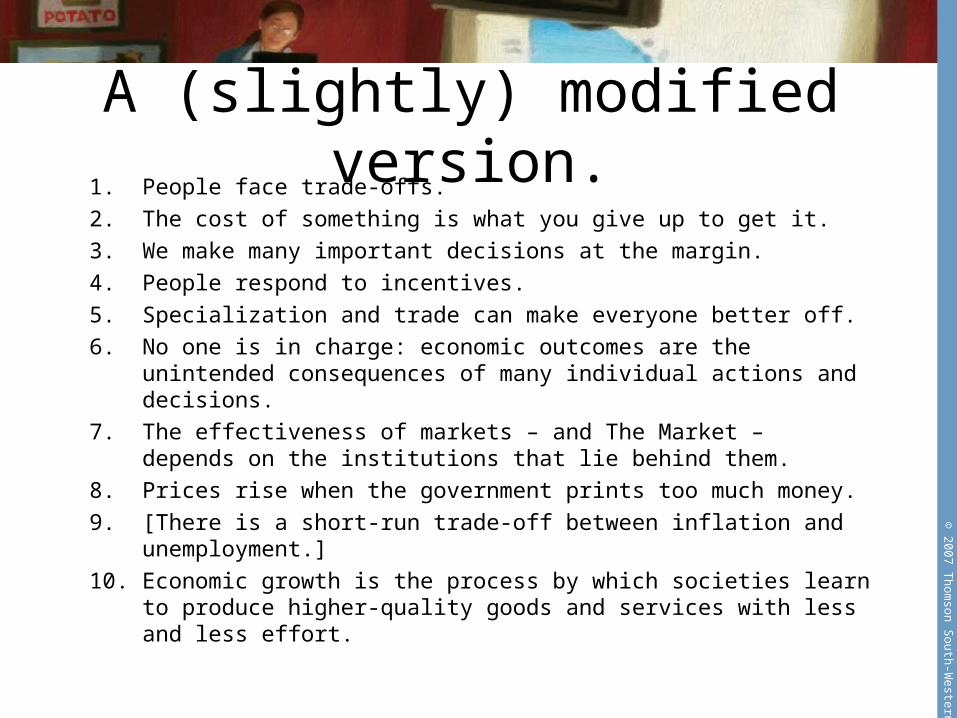

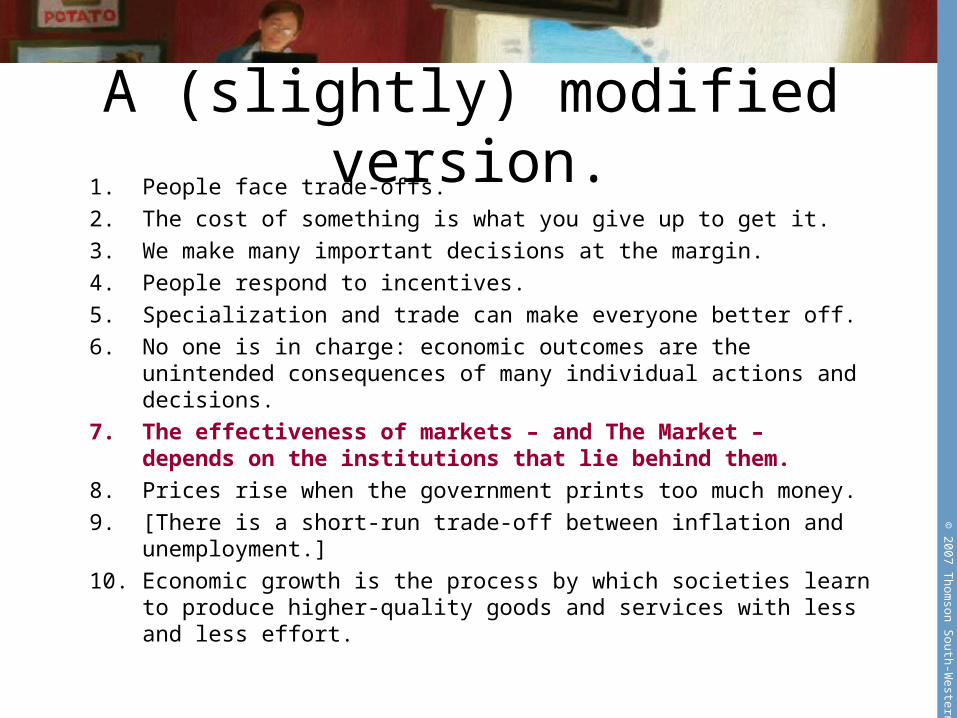

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the

unintended consequences of many individual actions and decisions.

7. The effectiveness of markets – and The Market – depends on the institutions that lie behind them.

8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn

to produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

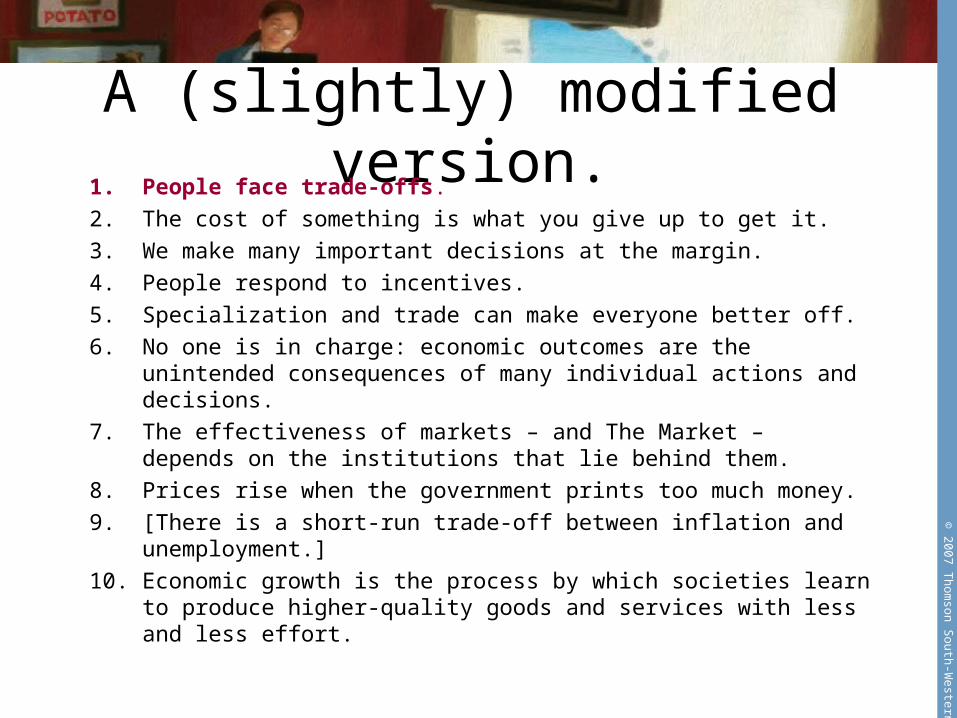

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the

unintended consequences of many individual actions and decisions.

7. The effectiveness of markets – and The Market – depends on the institutions that lie behind them.

8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn

to produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

People face trade-offs.All decisions involve tradeoffs. Examples:• Going to a party the night before your midterm

leaves less time for studying.• Having more money to buy stuff requires

working longer hours, which leaves less time for leisure.

• Protecting the environment requires resources that might otherwise be used to produce consumer goods.

There’s no such thing as a free lunch.

© 2007 T

homson S

outh-Western

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the

unintended consequences of many individual actions and decisions.

7. The effectiveness of markets – and The Market – depends on the institutions that lie behind them.

8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn

to produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

Opportunity cost.• Making decisions requires comparing

the costs and benefits of alternative choices.

• The opportunity cost of any item is whatever must be given up to obtain it.

• For example: The opportunity cost of going to college for a year is not just the tuition, books, and fees, but also the foregone wages.

© 2007 T

homson S

outh-Western

Opportunity cost.

So how come these guys

aren’t still in

college?

© 2007 T

homson S

outh-Western

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the

unintended consequences of many individual actions and decisions.

7. The effectiveness of markets – and The Market – depends on the institutions that lie behind them.

8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn

to produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

Thinking at the margin.• A person is rational if she does

the best she can to achieve her objectives given what she has to work with.

• Many decisions are not “all or nothing,” but involve marginal changes – incremental adjustments to an existing plan.

• Evaluating the costs and benefits of marginal changes is an important part of decision making.

© 2007 T

homson S

outh-Western

Thinking at the margin.Examples:

• A student considers whether to go to college for an additional year, comparing the fees & foregone wages to the extra income he could earn with an extra year of education.

• A firm considers whether to increase output, comparing the cost of the needed labor and materials to the extra revenue.– The sunk cost fallacy.

© 2007 T

homson S

outh-Western

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the

unintended consequences of many individual actions and decisions.

7. The effectiveness of markets – and The Market – depends on the institutions that lie behind them.

8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn

to produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

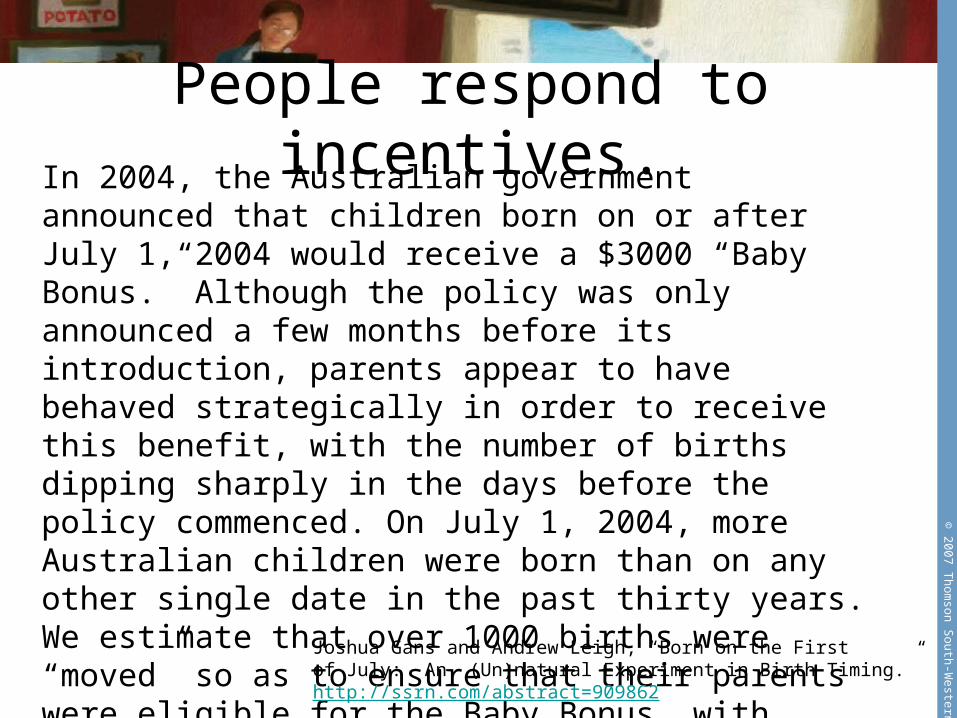

People respond to incentives.In 2004, the Australian government announced

that children born on or after July 1, 2004 would receive a $3000 “Baby Bonus.” Although the policy was only announced a few months before its introduction, parents appear to have behaved strategically in order to receive this benefit, with the number of births dipping sharply in the days before the policy commenced. On July 1, 2004, more Australian children were born than on any other single date in the past thirty years. We estimate that over 1000 births were “moved” so as to ensure that their parents were eligible for the Baby Bonus, with about one quarter being moved by more than two weeks. Most of the effect was due to changes in the timing of inducement and cesarean section procedures.

Joshua Gans and Andrew Leigh, “Born on the First of July: An (Un)natural Experiment in Birth Timing.” http://ssrn.com/abstract=909862

© 2007 T

homson S

outh-Western

People respond to incentives.

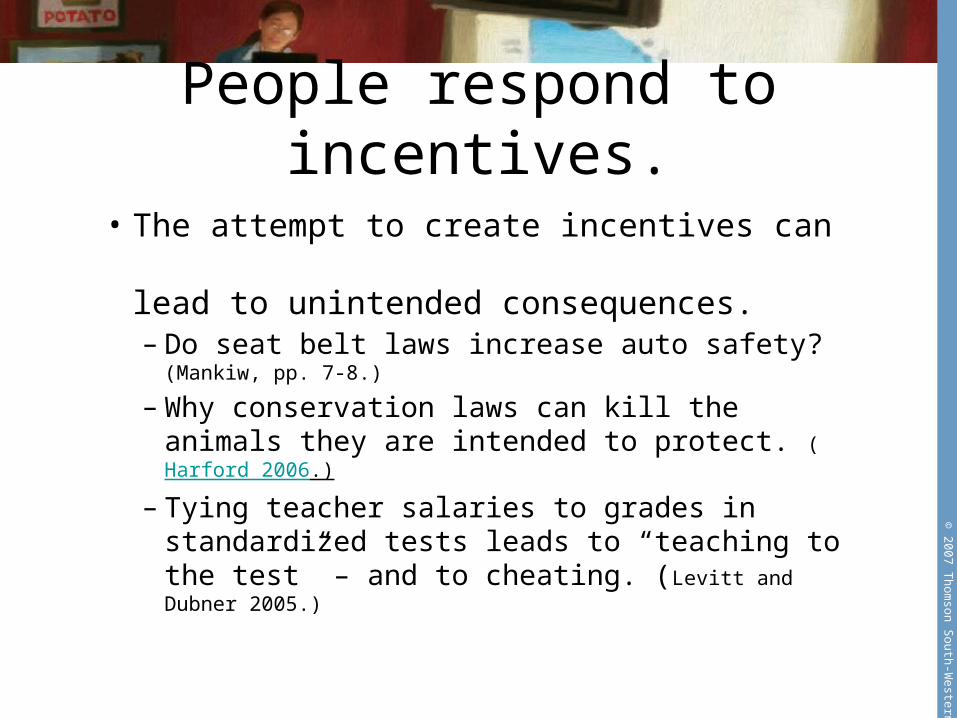

• The attempt to create incentives can lead to unintended consequences.– Do seat belt laws increase auto safety?

(Mankiw, pp. 7-8.)

– Why conservation laws can kill the animals they are intended to protect. (Harford 2006.)

– Tying teacher salaries to grades in standardized tests leads to “teaching to the test” – and to cheating. (Levitt and Dubner 2005.)

© 2007 T

homson S

outh-Western

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better

off.6. No one is in charge: economic outcomes are the unintended

consequences of many individual actions and decisions.7. The effectiveness of markets – and The Market –

depends on the institutions that lie behind them.8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn to

produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

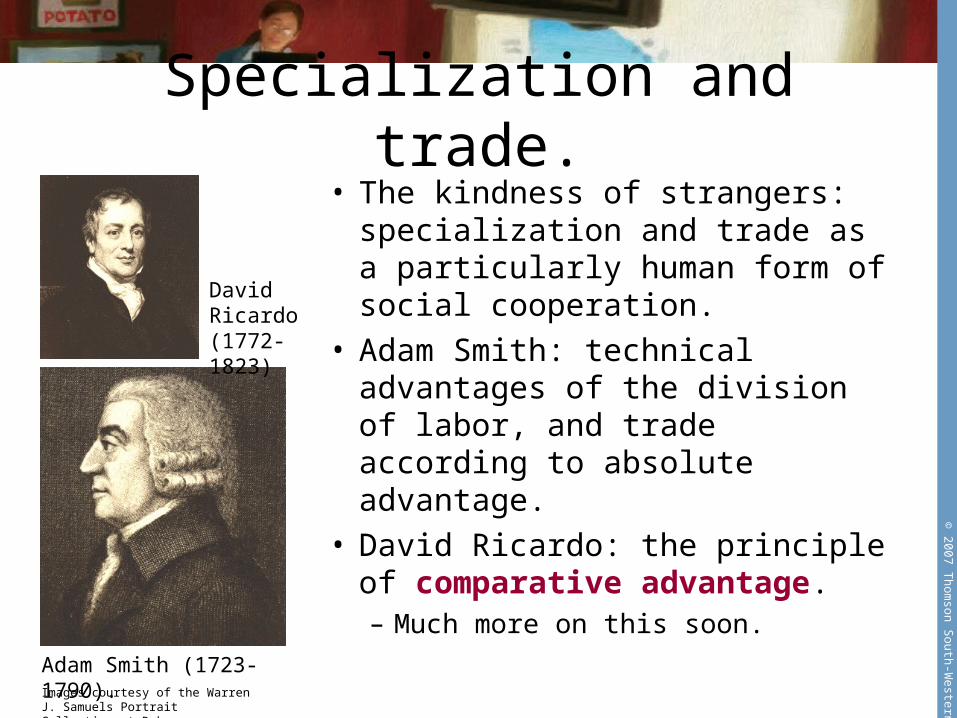

Specialization and trade.

Adam Smith (1723-1790).

David Ricardo (1772-1823)

Images courtesy of the Warren J. Samuels Portrait Collection at Duke University.

• The kindness of strangers: specialization and trade as a particularly human form of social cooperation.

• Adam Smith: technical advantages of the division of labor, and trade according to absolute advantage.

• David Ricardo: the principle of comparative advantage.– Much more on this soon.

© 2007 T

homson S

outh-Western

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the

unplanned consequences of many individual actions and decisions.

7. The effectiveness of markets – and The Market – depends on the institutions that lie behind them.

8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn to

produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

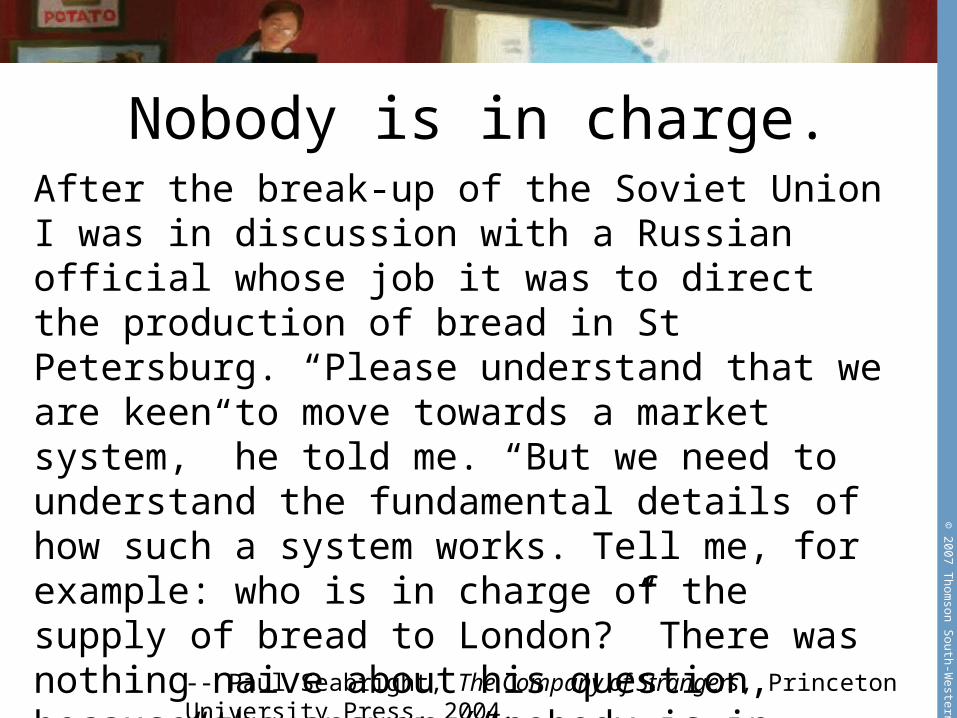

Nobody is in charge.After the break-up of the Soviet Union I was in discussion with a Russian official whose job it was to direct the production of bread in St Petersburg. “Please understand that we are keen to move towards a market system,” he told me. “But we need to understand the fundamental details of how such a system works. Tell me, for example: who is in charge of the supply of bread to London?” There was nothing naive about his question, because the answer (“nobody is in charge”), when one thinks carefully about it, is astonishingly hard to believe. Only in the industrialised West have we forgotten just how strange it is.

-- Paul Seabright, The Company of Strangers, Princeton University Press, 2004.

© 2007 T

homson S

outh-Western

The Invisible Hand.

Adam Smith (1723-1790). Image courtesy of the Warren J. Samuels Portrait Collection at Duke University.

• Under the right institutional arrangements, the pursuit of individual goals can lead to orderly and socially beneficial outcomes.

• Individuals are led as if by an invisible hand to promote outcomes they never intended.

• Taking advantage of dispersed local knowledge and specialized skills.

© 2007 T

homson S

outh-Western

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the

unintended consequences of many individual actions and decisions.

7. The effectiveness of markets – and The Market – depends on the institutions that lie behind them.

8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn

to produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

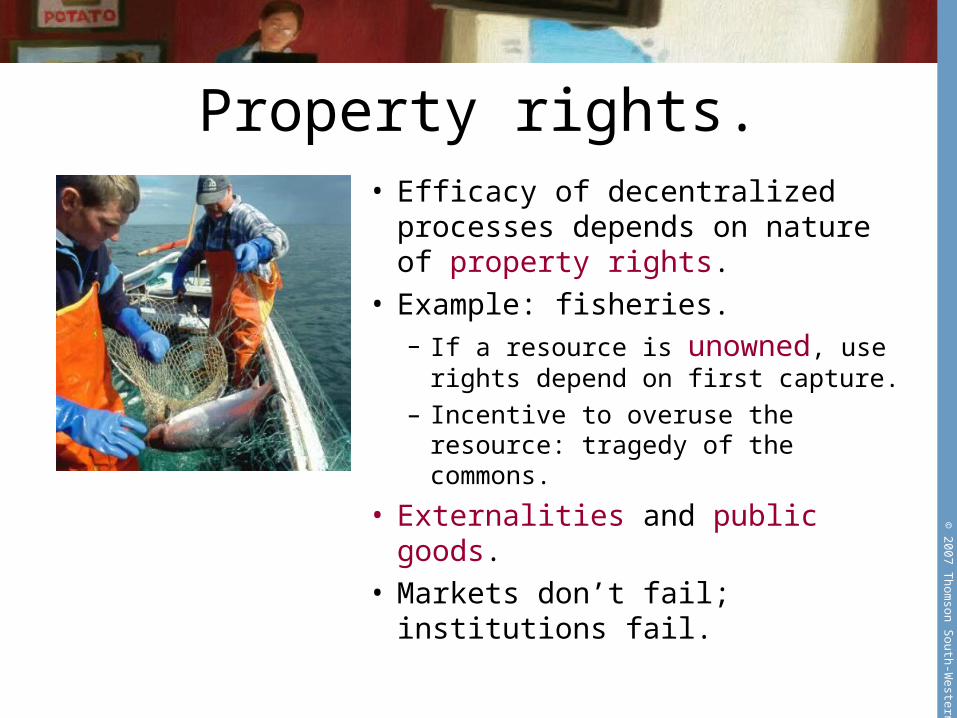

Property rights.• Efficacy of decentralized

processes depends on nature of property rights.

• Example: fisheries.– If a resource is unowned, use

rights depend on first capture.– Incentive to overuse the

resource: tragedy of the commons.

• Externalities and public goods.• Markets don’t fail; institutions

fail.

© 2007 T

homson S

outh-Western

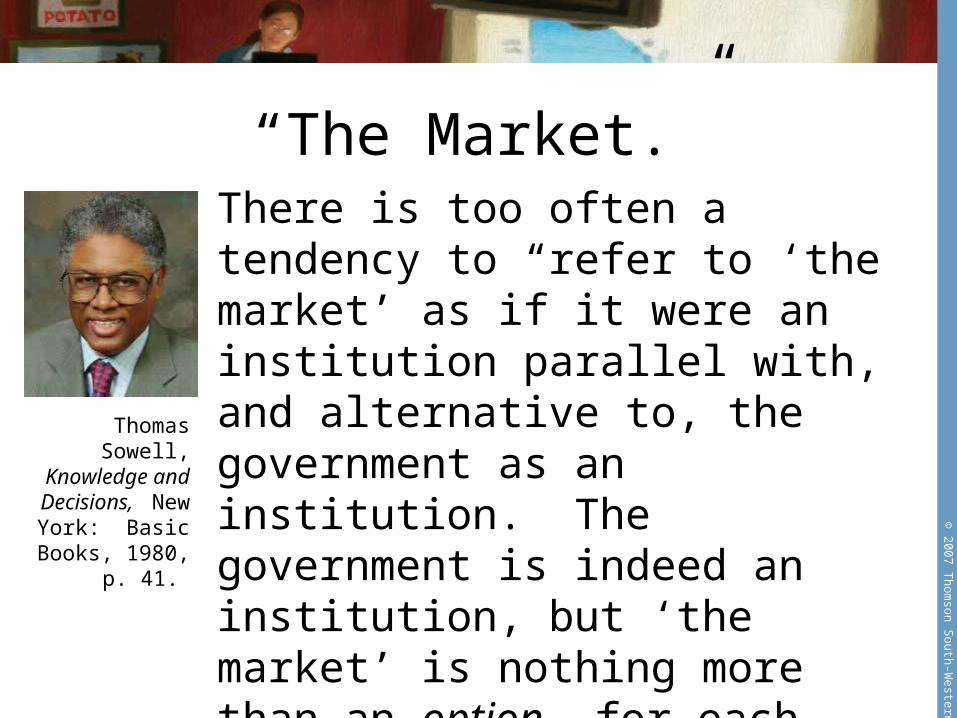

“The Market.”There is too often a tendency to “refer to ‘the market’ as if it were an institution parallel with, and alternative to, the government as an institution. The government is indeed an institution, but ‘the market’ is nothing more than an option for each individual to choose among numerous existing institutions, or to fashion new arrangements suited to his own situation and taste.”

Thomas Sowell,

Knowledge and Decisions,

New York: Basic Books, 1980, p. 41.

© 2007 T

homson S

outh-Western

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the unintended

consequences of many individual actions and decisions.7. The effectiveness of markets – and The Market –

depends on the institutions that lie behind them.8. Prices rise when the government prints too much

money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies learn to

produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

Inflation.

• Inflation is an increase in the general price level.– Not to be confused with a change in relative prices.

• Higher prices don’t cause inflation; they are inflation.

• In the long run, inflation is almost always caused by excessive growth in the quantity of money, which causes the value of money to fall.

© 2007 T

homson S

outh-Western

A (slightly) modified version.

1. People face trade-offs.2. The cost of something is what you give up to get it.3. We make many important decisions at the margin.4. People respond to incentives.5. Specialization and trade can make everyone better off.6. No one is in charge: economic outcomes are the

unintended consequences of many individual actions and decisions.

7. The effectiveness of markets – and The Market – depends on the institutions that lie behind them.

8. Prices rise when the government prints too much money.9. [There is a short-run trade-off between inflation and

unemployment.]10. Economic growth is the process by which societies

learn to produce higher-quality goods and services with less and less effort.

© 2007 T

homson S

outh-Western

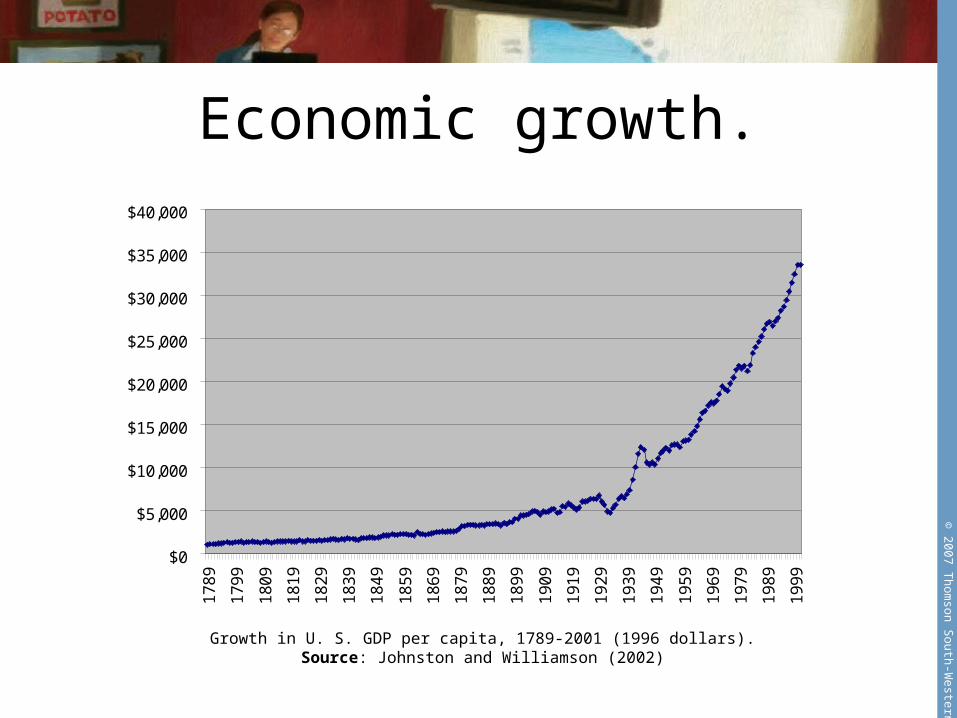

Economic growth.

Growth in U. S. GDP per capita, 1789-2001 (1996 dollars).Source: Johnston and Williamson (2002)

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,0001789

1799

1809

1819

1829

1839

1849

1859

1869

1879

1889

1899

1909

1919

1929

1939

1949

1959

1969

1979

1989

1999

© 2007 T

homson S

outh-Western

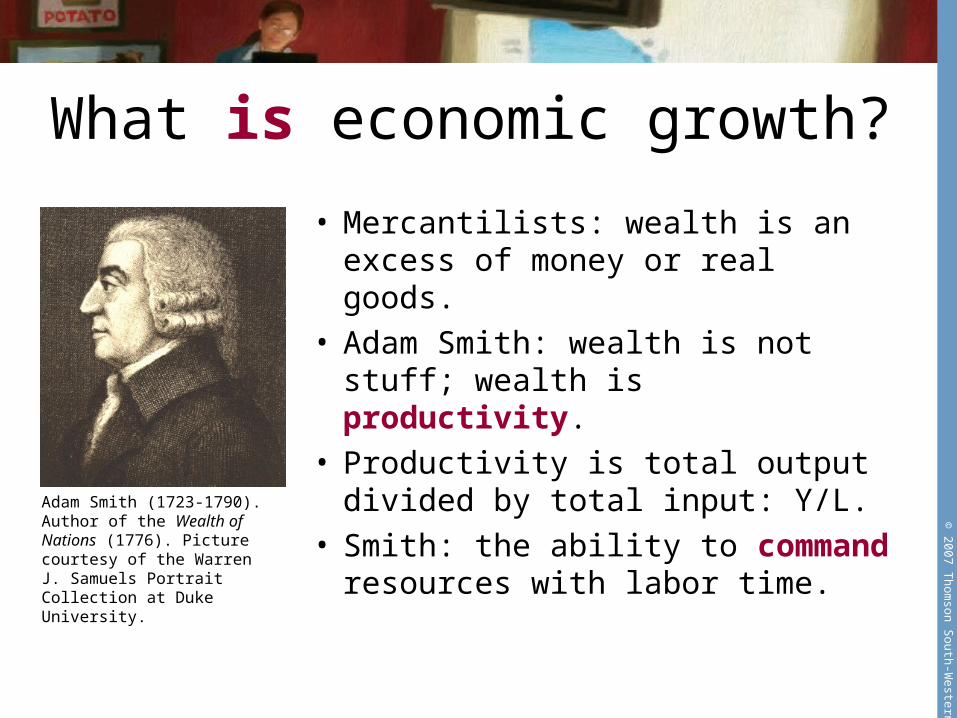

What is economic growth?

• Mercantilists: wealth is an excess of money or real goods.

• Adam Smith: wealth is not stuff; wealth is productivity.

• Productivity is total output divided by total input: Y/L.

• Smith: the ability to command resources with labor time.

Adam Smith (1723-1790). Author of the Wealth of Nations (1776). Picture courtesy of the Warren J. Samuels Portrait Collection at Duke University.

© 2007 T

homson S

outh-Western

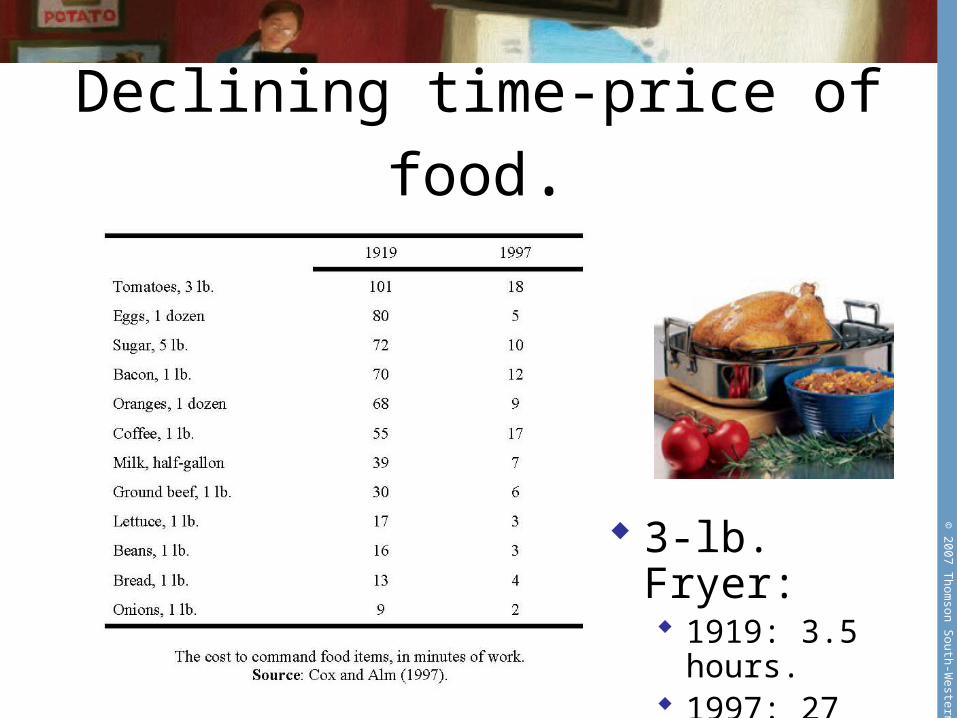

Declining time-price of food.

3-lb. Fryer: 1919: 3.5 hours. 1997: 27 minutes.

© 2007 T

homson S

outh-Western

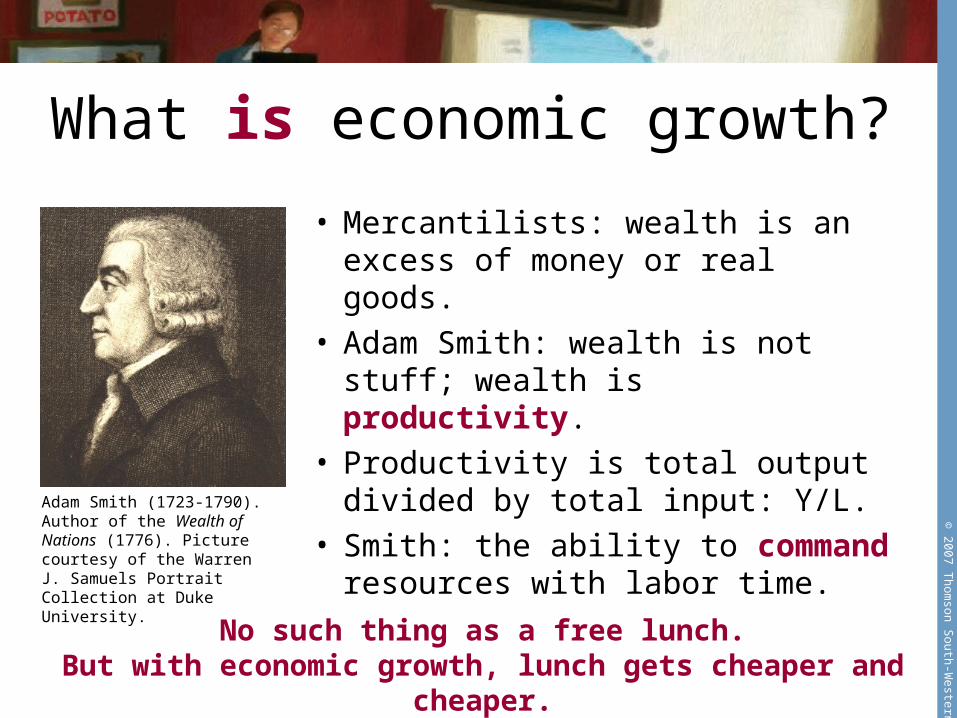

What is economic growth?

• Mercantilists: wealth is an excess of money or real goods.

• Adam Smith: wealth is not stuff; wealth is productivity.

• Productivity is total output divided by total input: Y/L.

• Smith: the ability to command resources with labor time.

Adam Smith (1723-1790). Author of the Wealth of Nations (1776). Picture courtesy of the Warren J. Samuels Portrait Collection at Duke University.

No such thing as a free lunch.But with economic growth, lunch gets cheaper and

cheaper.